Answered step by step

Verified Expert Solution

Question

1 Approved Answer

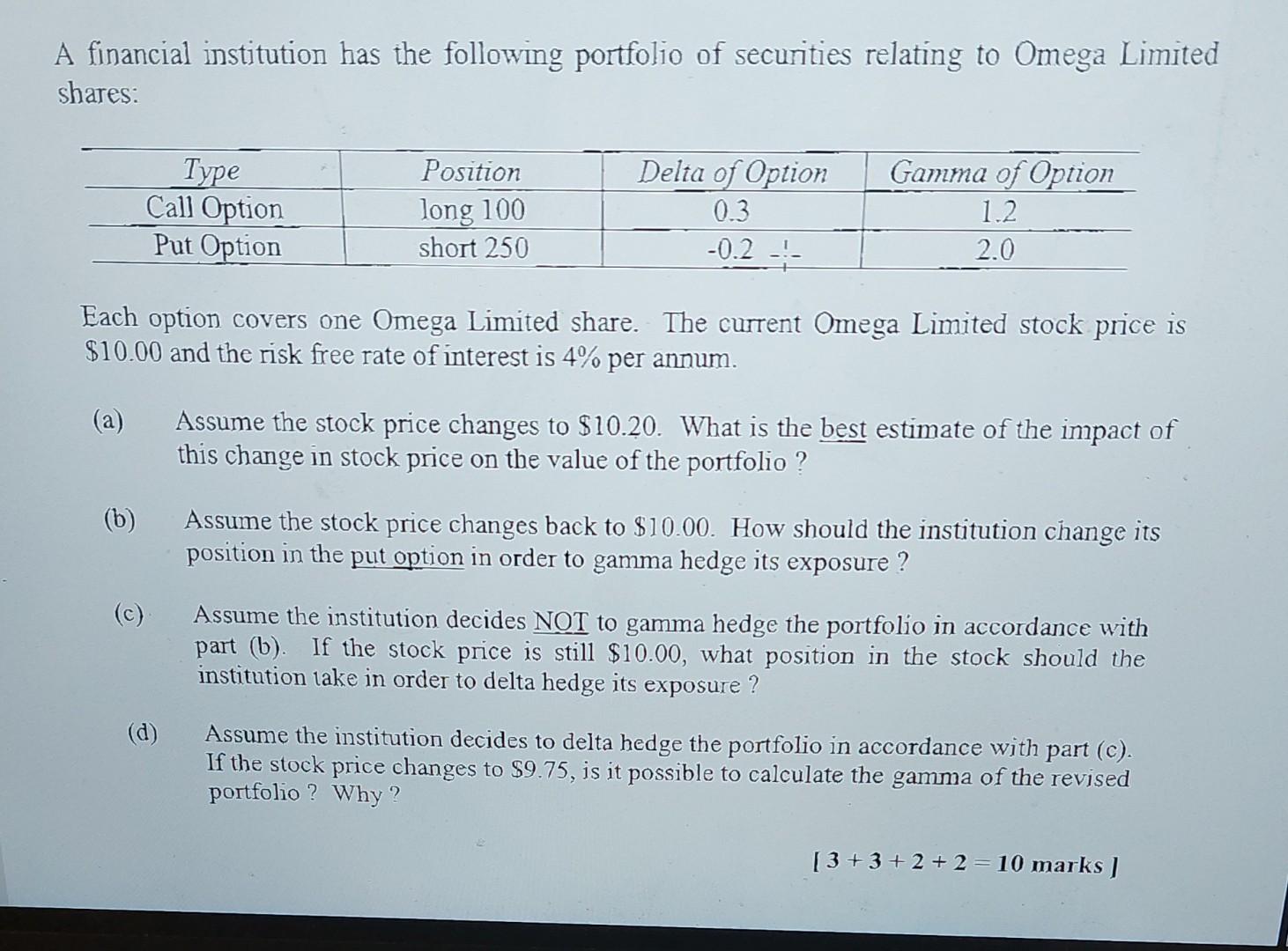

A financial institution has the following portfolio of securities relating to Omega Limited shares: Each option covers one Omega Limited share. The current Omega Limited

A financial institution has the following portfolio of securities relating to Omega Limited shares: Each option covers one Omega Limited share. The current Omega Limited stock price is $10.00 and the risk free rate of interest is 4% per annum. (a) Assume the stock price changes to $10.20. What is the best estimate of the impact of this change in stock price on the value of the portfolio? (b) Assume the stock price changes back to $10.00. How should the institution change its position in the put option in order to gamma hedge its exposure? (c) Assume the institution decides NOT to gamma hedge the portfolio in accordance with part (b). If the stock price is still $10.00, what position in the stock should the institution lake in order to delta hedge its exposure? (d) Assume the institution decides to delta hedge the portfolio in accordance with part (c). If the stock price changes to $9.75, is it possible to calculate the gamma of the revised portfolio? Why? [3+3+2+2=10 marks ] A financial institution has the following portfolio of securities relating to Omega Limited shares: Each option covers one Omega Limited share. The current Omega Limited stock price is $10.00 and the risk free rate of interest is 4% per annum. (a) Assume the stock price changes to $10.20. What is the best estimate of the impact of this change in stock price on the value of the portfolio? (b) Assume the stock price changes back to $10.00. How should the institution change its position in the put option in order to gamma hedge its exposure? (c) Assume the institution decides NOT to gamma hedge the portfolio in accordance with part (b). If the stock price is still $10.00, what position in the stock should the institution lake in order to delta hedge its exposure? (d) Assume the institution decides to delta hedge the portfolio in accordance with part (c). If the stock price changes to $9.75, is it possible to calculate the gamma of the revised portfolio? Why? [3+3+2+2=10 marks ]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advances In Entrepreneurial Finance

Authors: Rassoul Yazdipour

2011th Edition

148998190X, 978-1489981905