Question

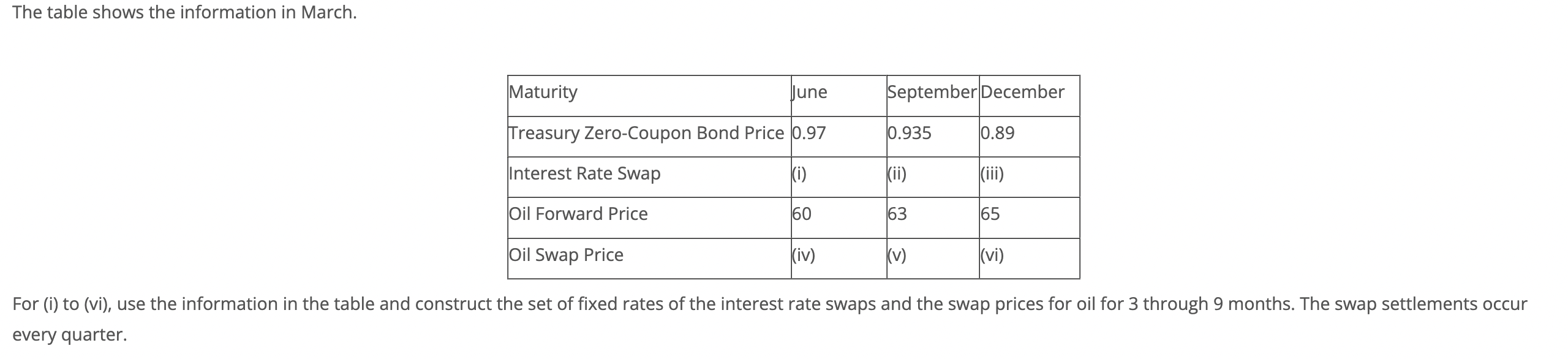

(a) Find item (i) to (vi) (b) Consider the 9-month oil swap. 3 months later, the oil price is $61/barrel. If cash settlement occurs, what

(a) Find item (i) to (vi)

(b) Consider the 9-month oil swap. 3 months later, the oil price is $61/barrel. If cash settlement occurs, what is the payoff of the floating price payer at t=3 months on a 1,000-barrel swap agreement?

(c) After the settlement above, what is the value of the swap? Given that the 3-month and 6-month interest rate at that time is 2% and 4.5% effectively. Assume the dividend yield (lease rate) of oil is negligible.

Thank you!

The table shows the information in March. For (i) to (vi), use the information in the table and construct the set of fixed rates of the interest rate swaps and the swap prices for oil for 3 through 9 months. The swap settlements occur every quarterStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Art Of M And A A Merger Acquisition Buyout Guide

Authors: Stanley Foster Reed, Alexandria Lajoux , H. Peter Nesvold

4th Edition

0071714952, 9780071714952