Answered step by step

Verified Expert Solution

Question

1 Approved Answer

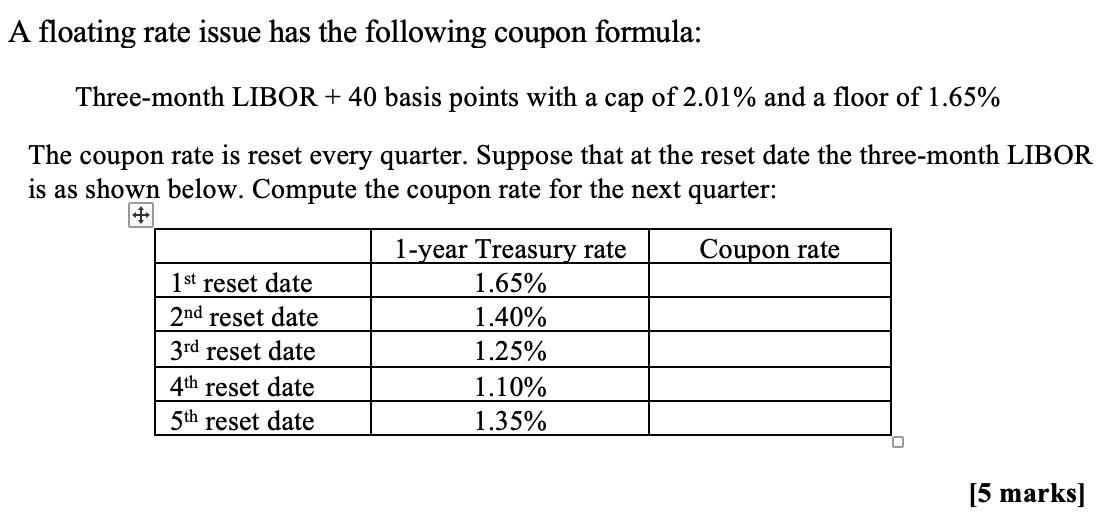

A floating rate issue has the following coupon formula: Three-month LIBOR + 40 basis points with a cap of 2.01% and a floor of

A floating rate issue has the following coupon formula: Three-month LIBOR + 40 basis points with a cap of 2.01% and a floor of 1.65% The coupon rate is reset every quarter. Suppose that at the reset date the three-month LIBOR is as shown below. Compute the coupon rate for the next quarter: Coupon rate + 1st reset date 2nd reset date 3rd reset date 4th reset date 5th reset date 1-year Treasury rate 1.65% 1.40% 1.25% 1.10% 1.35% [5 marks]

Step by Step Solution

★★★★★

3.40 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the coupon rate for the next quarter we need to compare the current threemonth LIBOR ra...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bond Markets Analysis and Strategies

Authors: Frank J.Fabozzi

9th edition

133796779, 978-0133796773