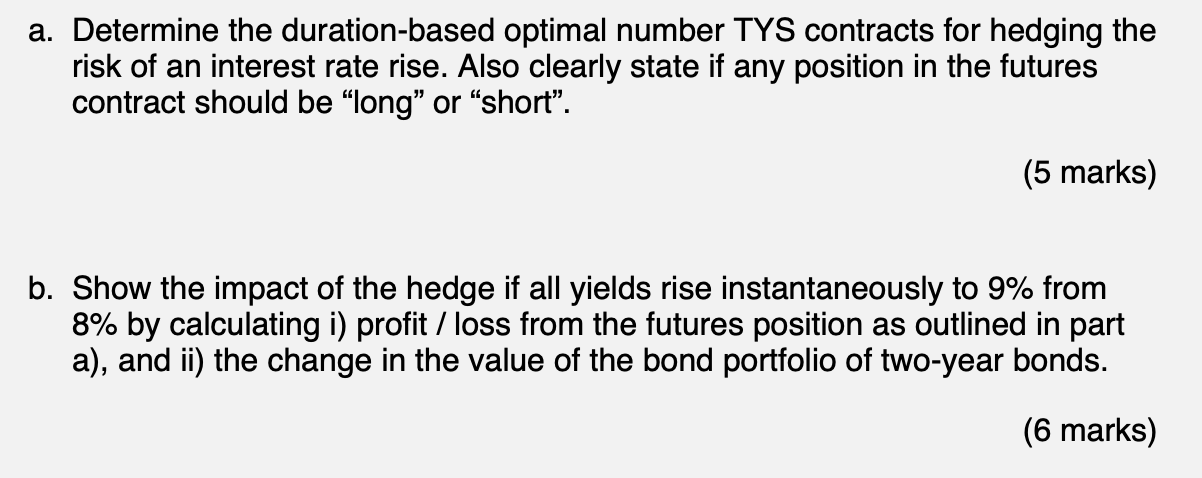

A fund manager has a portfolio of two-year bonds with a total face value of $30 million. These bonds carry a 5% p.a. coupon paid semi-annually. Concerned that a rise in interest rates will reduce the market value of her bond portfolio, the fund manager would like to take a position in the three-year New Zealand Government Stock futures contract (TYS) at a price of 92.00 (or 9200 implying an 8% p.a. yield-to-maturity). The asset underlying this TYS contract is three-year government stock with $100,000 face value, 8% p.a. coupon, paid semi-annually. Assume that the yield curve is flat at 8% p.a. (semi-annual compounding) - that is, yields for all maturities are 8% p.a. - and that the duration of TYS contract is 2.726 years when yields are 8% p.a. Hint: All rates quoted above are simple annualized rates with semi-annual compounding. a. Determine the duration-based optimal number TYS contracts for hedging the risk of an interest rate rise. Also clearly state if any position in the futures contract should be "long or short". (5 marks) b. Show the impact of the hedge if all yields rise instantaneously to 9% from 8% by calculating i) profit / loss from the futures position as outlined in part a), and ii) the change in the value of the bond portfolio of two-year bonds. (6 marks) A fund manager has a portfolio of two-year bonds with a total face value of $30 million. These bonds carry a 5% p.a. coupon paid semi-annually. Concerned that a rise in interest rates will reduce the market value of her bond portfolio, the fund manager would like to take a position in the three-year New Zealand Government Stock futures contract (TYS) at a price of 92.00 (or 9200 implying an 8% p.a. yield-to-maturity). The asset underlying this TYS contract is three-year government stock with $100,000 face value, 8% p.a. coupon, paid semi-annually. Assume that the yield curve is flat at 8% p.a. (semi-annual compounding) - that is, yields for all maturities are 8% p.a. - and that the duration of TYS contract is 2.726 years when yields are 8% p.a. Hint: All rates quoted above are simple annualized rates with semi-annual compounding. a. Determine the duration-based optimal number TYS contracts for hedging the risk of an interest rate rise. Also clearly state if any position in the futures contract should be "long or short". (5 marks) b. Show the impact of the hedge if all yields rise instantaneously to 9% from 8% by calculating i) profit / loss from the futures position as outlined in part a), and ii) the change in the value of the bond portfolio of two-year bonds. (6 marks)