Question

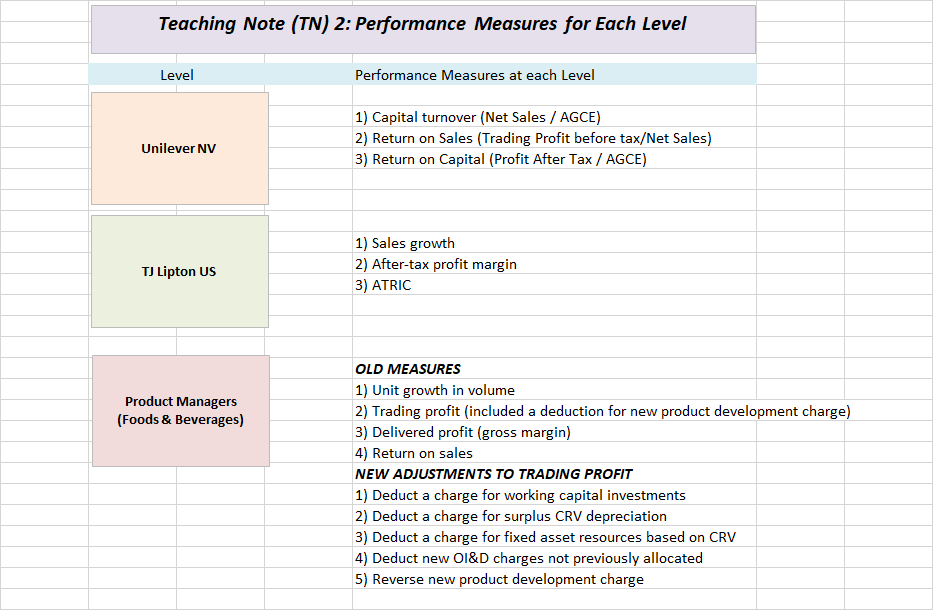

a) How are managers currently evaluated? (see TN2 - OLD Measures) b) Do you believe the current system is fair (if not, recommend changes; Hint

a) How are managers currently evaluated? (see TN2 - OLD Measures)

b) Do you believe the current system is fair (if not, recommend changes; Hint reconsider any expenses that are included that are not controllable by product-line managers as an argument can be made that one shouldn't be responsible for costs they cannot control AND consider expenses that are under their control but not included in the calculation)?

c) Are the current measures congruent with Lipton's corporate level objectives? How about Unilever's? Are these differences at the heart of the changes that are being proposed by Don Logan (be brief; yes or no)? How do the product-line managers feel about the recommended changes? Why are they upset? Be brief.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing A Practical Approach With Data Analytics

Authors: Raymond N. Johnson, Laura Davis Wiley, Robyn Moroney, Fiona Campbell, Jane Hamilton

2nd Edition

1119786045, 978-1119785996