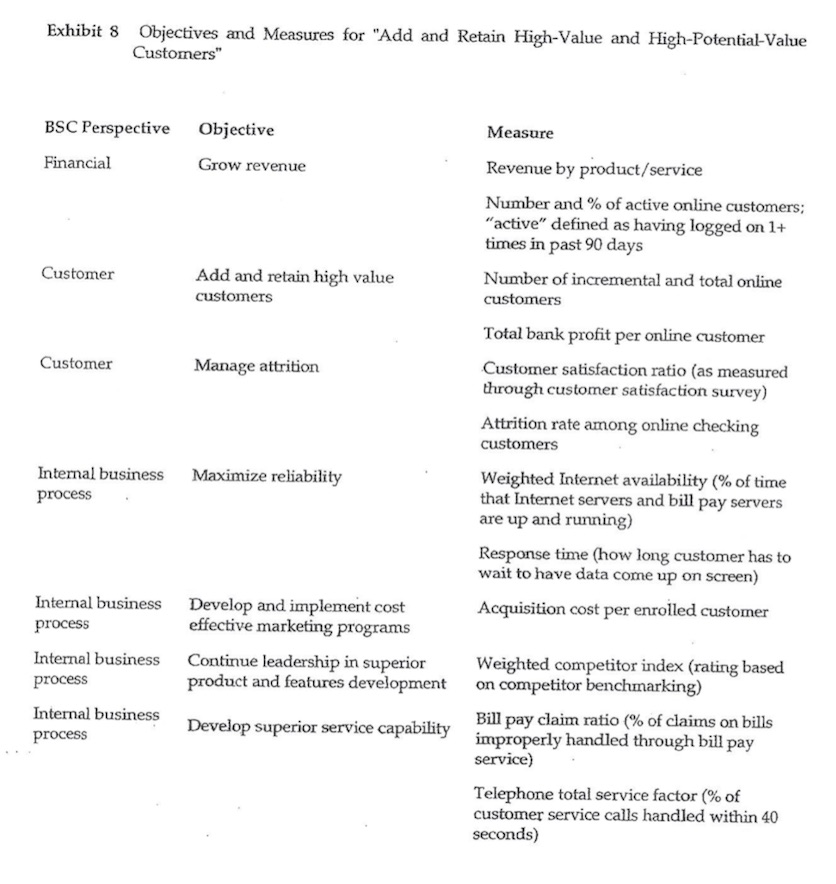

a) increasing revenues per customer and b) reducing costs per customer using the example format provided in Exhibit 8 of the case. Please develop 4 to 5 objectives/measures

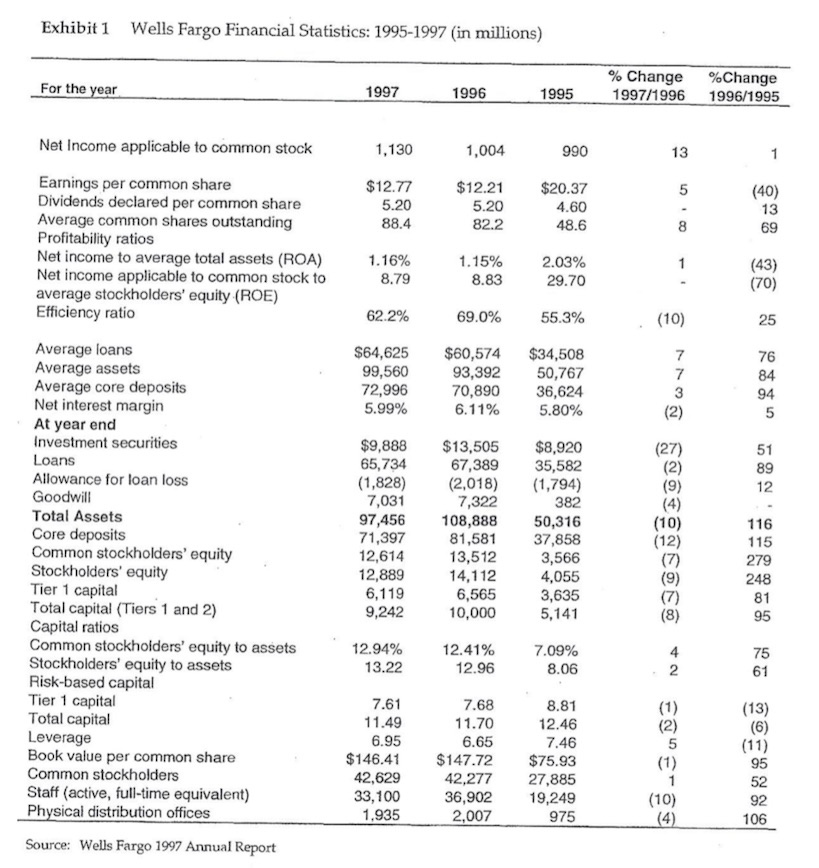

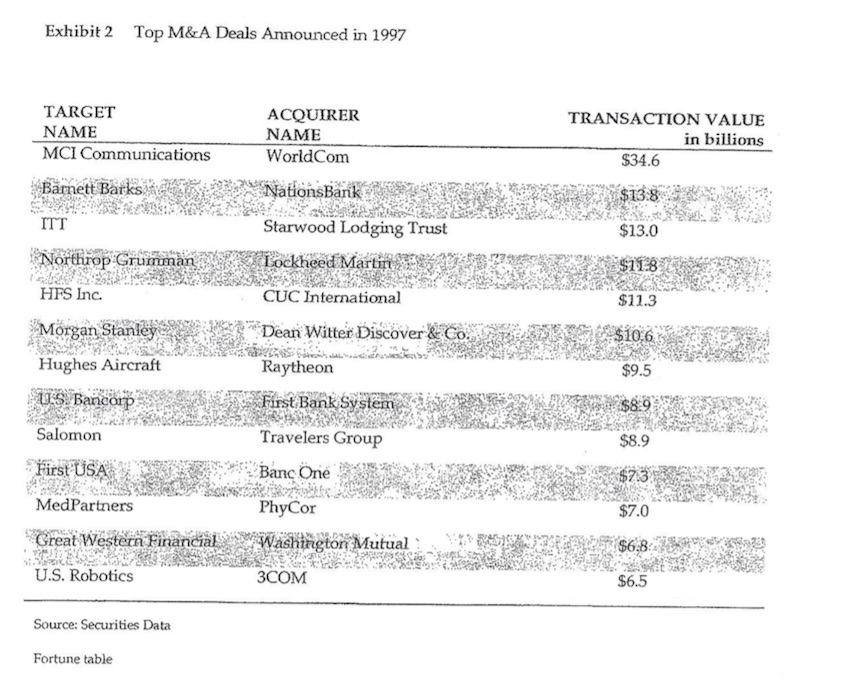

Wells Fargo was wel known in the banking industry for its focus on nnovation and cost management. In most cases the two were interrelated: innovations often enabled the bank to reduce operating costs. On the innovation front, Wells Fargo was one of the first banks in the country to offer extended weekday and Saturday hours, and it was a pioneer in pursuing nontraditional delivery channels, such as installing ATM machines in grocery stores. Such installations required less capital to build and cost less to operate than a standard freestanding branch. The bank was also a leader in testing new retail formats such as its one-stop-shopping banking center which included a full service branch, a Starbucks coffee outlet, a dry cleaner and a photocopying service all under one roof. Wells Fargo's focus on cost management was championed by Carl Reichardt, chairman from 1983 through 1994, who built an ambitious management culture with slogans such as, "Run it like you own it." The aggressive focus on costs caused the bank to exit businesses where the margins did not meet its targets; for example, the bank sold its home mortgage portfolio business in 1994 due to intense pressure on rates from regional savings and loans. Wells Fargo's acquisition of First Interstate was also an effort to gain efficiencies by enabling the bank to consolidate overhead and close over 300 redundant branches. The Commercial Banking Industry During the late 1980s, the commercial banking industry entered into a period of widespread olidation as Congress, the Federal Reserve, and other government agencies lowered the barriers that had previously separated different parts of the financial services universe, blurring the lines etween banks, brokerage firms, insurers, finance companies, and credit card issuers. Some of the most significant changes occurred when Congress passed legislation that allowed full-scale interstate banking in 1994 and when the Federal Reserve Board raised the limit on the amount of underwriting business a bank affiliate was permitted from 10% to 25% of revenues in 1996, By the mid-1990s commercial banks could sell stocks and mutual funds, investment banks could offer lines of credit, and credit card issuers could sell insurance. Competition intensified even further due to a series of industry mergers and acquisitions initiated to increase profits through greater economies of scale. Some of the best known, long-standing names in the commercial banking industry merged or were acquired in the 1990s. These included Chemical Bank's $2.3 billion merger with Manufacturer's over in 1991, BankAmerica's $4 billion acquisition of Security Pacific in 1992, Chase Manhattan's $10 billion merger with Chemical Bank in 1995, and Wells Fargo's $11.6 billion acquisition of First Interstate in 1996. In fact, of the 13 largest merger and acquisition (M&A) deals announced in 1997, 6 involved combinations of financial institutions, of which 3 were combinations of commercial banks including NationsBank's $13.8 billion acquisition of Barnett Banks and Banc One's $7.3 billion acquisition of First USA (see Exhibit 2 for the top 13 M&A deals announced in 1997). To succeed in an increasingly competitive environment, commercial banks were pursuing innovative ways to attract customers and reduce costs, many of which required significant investments in technology Electronic Banking The term electronic banking described two services that allowed consumers to access their ban bank's proprietary software or a personal finance software package such as Money or Quicken t browser software, such as Netscape Navigator or Microsoft Internet Explorer. accounts and conduct transactions using their computers. PC banking referred to customers using a access their bank's network via a modem. Internet banking allowed customers to access their bank account information through the Internet by connecting to their bank's Web site directly, using Web While only an estimated 250,000 U.S. households used electronic banking for account access or bill payment in 1994, the number had climbed to 4.5 million by 1997, representing 45% of all US the year 2000, industry experts projected that more than 17 million U.S. households would be using electronic banking (see Exhibit 3 for projected usage of electronic banking) Growth in electronic banking had been fueled by the growth in the installed base of personal comput homes and in the workplace; between 1994 and 1996, the number of installed PCs in the U.S. had increased from 78 million to almost 95 million, a 10% compound annual growth rat personal finance was one of the leading uses for home computers, ahead of spreadsheets and work brought home from the office ers in e. Moreover, internet usage in the United States had also grown rapidly between 1996 and 1997-increasing from an estimated 34 million adult users over the age of 16 end of 1997, 2700 banks and credit unions had established Web sites on the Internet. However, the majority of these Web sites offered only standard, packaged marketing information; 1 ffered customers direct account access. to over 50 million by early 1997. By the ess than 6% Wells Fargo Online Financial Services In 1989 Wells Fargo introduced its first electronic banking product which allowed consumers to access their accounts through Prodigy's online service. Shortly thereafter, Wells Fargo introduced its own proprietary DOS-based system. However, by late 1994 only 20,000 customers were using the two services combined, prompting the bank to look for ways to improve its online banking offerings g services as "online"). The OFS group consisted of 75 people at the time, all of whom had come from other departments within the bank. In December 1994 Wells Fargo's corporate marketing group launched a Web site on the World Wide Web as part of its brand-building effort on behalf of the bank as a whole. The Web site initially provided onl dard marketing information. Soon, however, customers were asking for direct account access Karen Derr Gilbert, vice president of marketing for OPS, recalled We took the customer feedback and asked our technology group, "can we do this?" By we had balances and account histories available to customers through our Web sit It was phenomenal since it was an entirely customer-driven process. Wells Fargo was the first major U.S. bank to offer Intemet access (see Exhibit 4 for the laundlh dates of competitors' Internet offerings), and customer response was overv Wells Fargo customers accessed their accounts through the Inte helming over 10 ,000 rnet service in the first two months of operation. Dudley Nigg, executive vice president of OFS at Wells Fargo, reflected on the decision to launch the Internet service: In recent years, banks have become far more consumer focused. The trend started about 15 years ago when banks began to offer longer hours and expanded services in consumer demand for greater convenience and greater access responseto . We realized then that customers considered banking a chore, which led us to find ways to make it easier for them We began to study which channels offered consumers the convenience they want ed. We egan to look at convenience along a continuum, which included branch banking, telephone banking, and ATMs. Then we extended the continuum into the remote increasing number of customers saw the came to the conclusion that Wells Fargo should begin to aggressively offer banking space. In 1994 an as a very attractive medium, and we as an online channel option through that medium. Since then a couple of things have really allowed our Internet banking service to take off: first, the proliferation of PCs has given many more people access to fact, we're playing catch-up-a lot more of our customers have PCs Internet access than are currently banking online, so we are following behind a phenomenon that we don't have to lead; and second, the Internet has grown in importance far faster than any of us thought it would, especially out here on the West Coast. By 1998, the Wells Fargo Internet service, accessed through the www.wellsfargo.com Web address (see Exhibit 5 for Wells Fargo's home page), allowed customers to handle many of their banking needs online; for example customers could review their checking account and credit card balances pay bills, transfer funds, conduct stock and bond trades, order checks, information. Wells Fargo's Web site had generated significant praise from industry reviewers: Smart Money magazine named Wells Fargo "Best Online Bank" in 1996, the Online Banking Association named Wells Fargo's site "Best Overall Site by a U.S. Financial Institution" in 1996, and Financial Net News named Wells Fargo's site "Best of Banks" in 1997.2 By early 1998 over 450,000 Wells Fargo customers used one of Wells Fargo's online banking services, and the company believed this number would grow to 1 million customers within two years. Wells Fargo's Internet service accounted for 350,000 of its online banking customers by early 1998 and it was projected to account for the majority of the growth going forward; the bank was enrolling close to 1,000 customers per day, and over 80% were Internet-based and request product Given its first-mover advantage, by 1997 Wells Fargo had captured a significant share of all electronic banking users in the United States. Maintaining or challenge as other banks, credit unions, brokerage firms, insurance firms and even nonfinancial institutions entered the electronic banking market. Wells Fargo's near-term strategy was similar to that of a "land rush": sign up as many customers as quickly as possible. Based on this strategy, early on Wells Fargo focused on designing its service to meet the needs of users of WebTV, Nokia Internet cell phones, and other Internet access devices, in an effort to meet customers wherever doing their banking growing that share would be a were The Wells Fargo Online Banking Customer The Wells Fargo online banking service appealed to an attractive customer segment. The average user was 38 years old, had a median household income of $75,000 to $100,000, was in a wealth ulation mode, and was a moderate to heavy borrower (through personal loans, credit card:s, and auto loans). Their behavior as bank customers provided the foundation for three of the four elements driving the business rationale for OFS. First, the online customer stayed with the bank average-the attrition rate for online banking customers was 50% below the bank's nd, the cross-selling opportunity was higher for online banking customers since they held, on average, one more product than the typical Wells Fargo customer. Third, online customers were more profitable to the bank since they carried higher balances on both deposits and loans. The fourth element of the OFS business case was not related to customer attractiveness, but rather to migrating Wells Fargo customers to a lower-cost service channel than branch banking, phone banking, and ATM operations. The American Banker's Association estimated that an online banking transaction cost $.01, whereas an ATM transaction cost $.27, a telephone transaction $.54, and a longer than average. Seco branch transaction $1.07.3 Exhibit1 Wells Fargo Financial Statistics: 1995-1997 (in millions) %Change %Change 1997/1996 1996/1995 For the year 1997 1996 1995 Net Income applicable to common stock 1,004 Earnings per common share Dividends declared per common share Average common shares outstanding Profitability ratios Net income to average total assets (ROA) Net income applicable to common stock to average stockholders' equity (ROE) Efficiency ratio $12.77 5.20 88.4 $12.21 5.20 $20.37 4.60 1.16% 8.79 1.15% 8.83 2.03% 29.70 62.2% 69.0% 55.3% 25 Average loans Average assets Average core deposits Net interest margin At year end Investment securities Loans Allowance for loan loss Goodwill Total Assets Core deposits Common stockholders' equity Stockholders' equity Tier 1 capital Total capital (Tiers 1 and 2) Capital ratios Common stockhoiders' equity to assets Stockholders' equity to assets Risk-based capital Tier 1 capital Total capital Leverage Book value per common share Common stockholders Staff (active, full-time equivalent) Physical distribution offices $64,625 $60,574 $34,508 99,560 93,392 50,767 72,996 70,890 36,624 6.11% 94 5 5.99% 5.80% $9,888 $13,505 $8,920 (27 65,734 67,389 35,582 (1,828)(2,018) (1,794) 7,031 382 97,456 108,888 50,316 81,581 13,512 14,112 6,565 10,000 116 71,397 12,614 12,889 37,858 3,566 4,055 3,635 5,141 9,242 12.94% 13.22 12.41% 12.96 7.09% 4 2 11.49 6.95 11.70 12.46 $146.4 $147.72 $75.93 42,629 42,277 27,885 36,902 19,249 975 95 33,100 1,935 2,007 Source: Wells Fargo 1997 Annual Report Exhibit 2 Top M&A Deals Announced in 1997 TARGET NAME MCI Communications ACQUIRER NAME WorldCom TRANSACTION VALUE in billions $34.6 ITT Starwood Lodging Trust $13.0 ummna HFS Inc. CUC International Dean WitterDis ov reo Raytheon First Bank Syst Travelers Group $11.3 1 a $9.5 Morgan Stany Hughes Aircraft Salomorn $8.9 MedPartners o a wes er Financi l ).wa ning oi Mutual U.S. Robotics PhyCor $7.0 se $6.5 s : 3COM Source: Securities Data Fortune table Exhibit 8 Objectives and Measures for "Add and Retain High-Value and High-Potential-Value Customers BSC Perspive Objective Measure Financial Grow revenue Revenue by product/service Number and % of active online customers "active" defined as having logged on 1+ times in past 90 days Customer Add and retain high value customers Number of incremental and total online customers Total bank profit per online customer Customer Manage attrition Customer satisfaction ratio (as measured through customer satisfaction survey) Attrition rate among online checking customers Internal business Miize reliability process Weighted Internet availability (% of time that Internet servers and bill pay servers are up and running) Response time (how long customer has to wait to have data come up on screen) Internal business process Internal business process Internal business process Develop and implement cost effective marketing programs Acquisition cost per enrolled customer Continue leadership in superior product and features development Weighted competitor index (rating based on competitor benchmarking) Bill pay claim ratio (% of claims on bills improperly handled through bill pay Develop superior service capability Telephone total service factor (% of customer service calls handled within 40 seconds)