Answered step by step

Verified Expert Solution

Question

1 Approved Answer

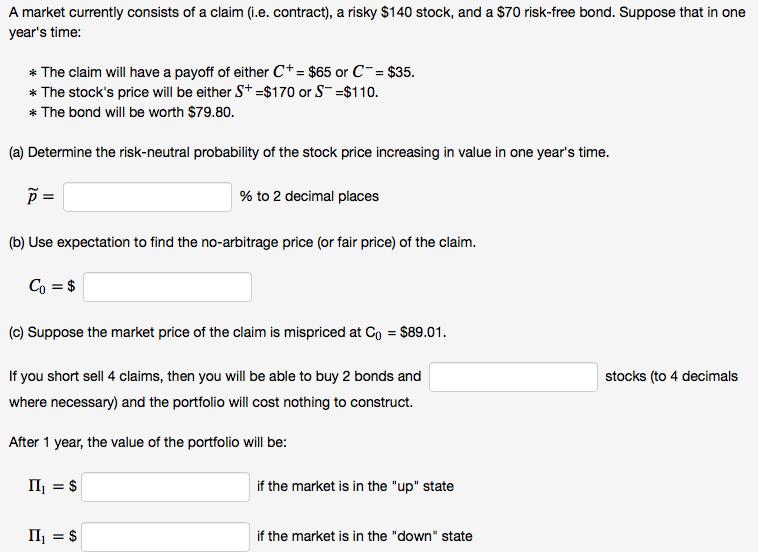

A market currently consists of a claim (i.e. contract), a risky $140 stock, and a $70 risk-free bond. Suppose that in one year's time:

A market currently consists of a claim (i.e. contract), a risky $140 stock, and a $70 risk-free bond. Suppose that in one year's time: * The claim will have a payoff of either C+ = $65 or C = $35. * The stock's price will be either S+ =$170 or S=$110. * The bond will be worth $79.80. (a) Determine the risk-neutral probability of the stock price increasing in value in one year's time. % to 2 decimal places (b) Use expectation to find the no-arbitrage price (or fair price) of the claim. Co = $ (c) Suppose the market price of the claim is mispriced at C = $89.01. If you short sell 4 claims, then you will be able to buy 2 bonds and where necessary) and the portfolio will cost nothing to construct. After 1 year, the value of the portfolio will be: II = $ II = $ if the market is in the "up" state if the market is in the "down" state stocks (to 4 decimals

Step by Step Solution

★★★★★

3.47 Rating (157 Votes )

There are 3 Steps involved in it

Step: 1

SOLUTION a To determine the riskneutral probability of the stock price increasing in value in one ye...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516