Question

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long term government and corporate bond

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5.5%. The stock fund and bond fund have expected returns 15% and 9%, and SD 32% and 23% The correlation between them is 0.15

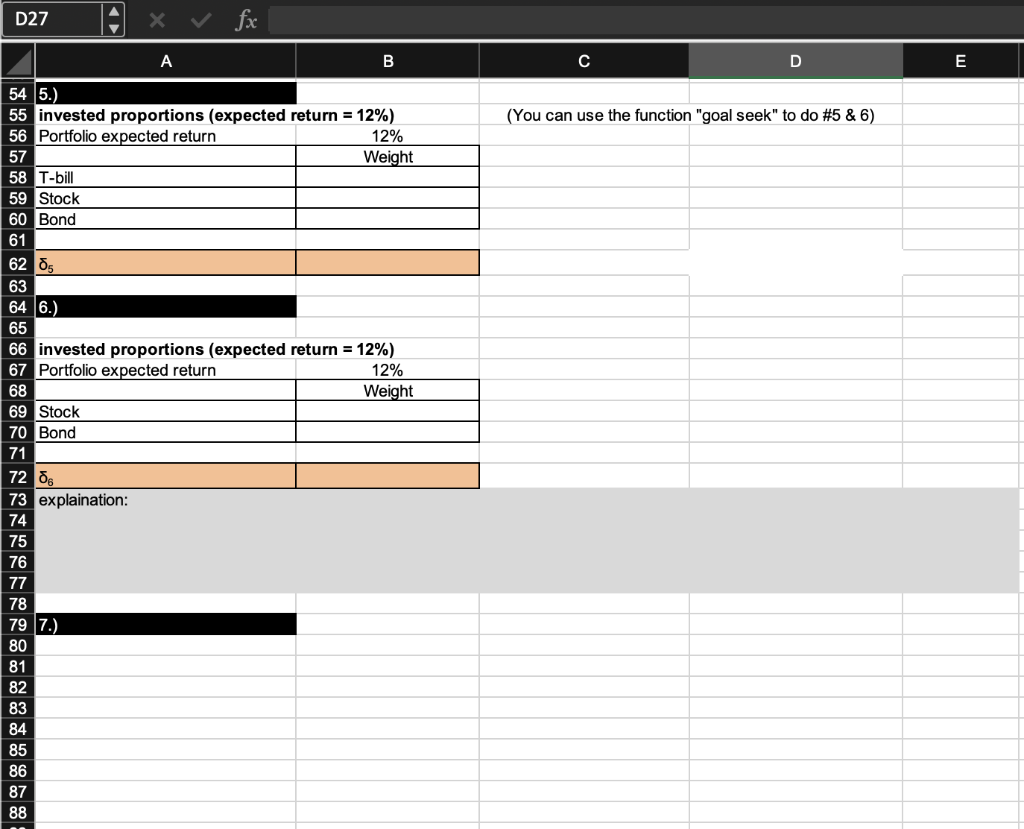

5.) You require that your portfolio yield an expected return of 12%. What is the proportion invested in the T-bill fund and each of the two risky fund?

6.) If you were to use only the two risky funds, and still require an expected return of 12%, what would be the investment proportions of your portfolio? Compare standard deviation of 5 and 6.

7.) Draw the graph.

Questions:

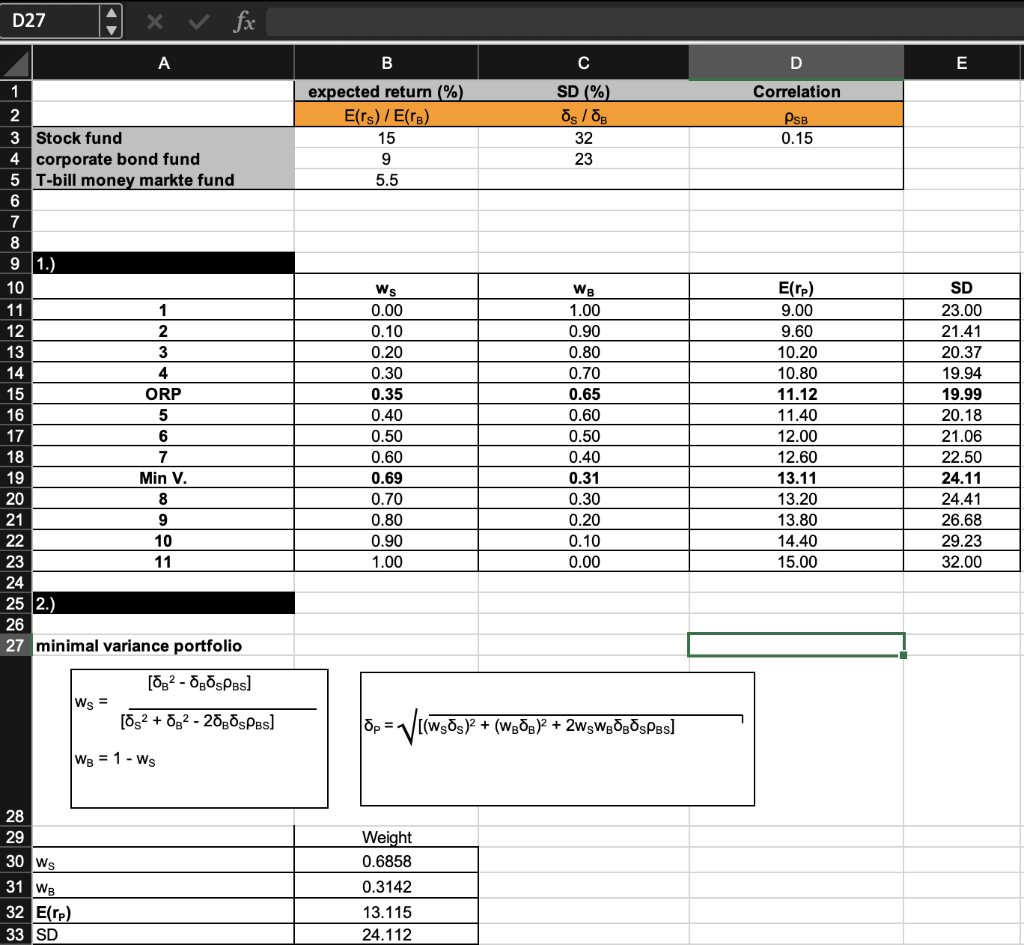

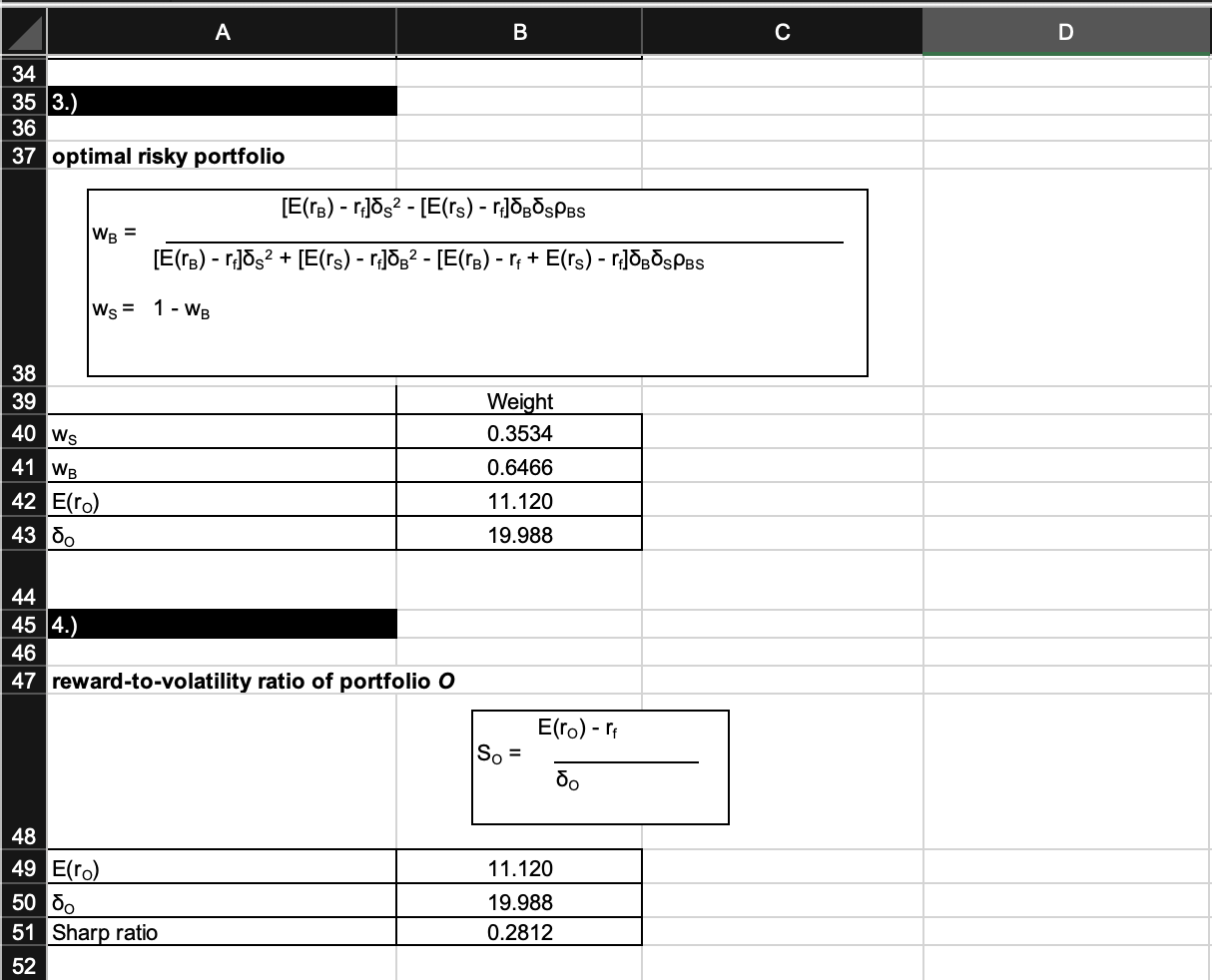

1.) 2.) minimal variance portfolio P=[(wSS)2+(wBB)2+2wSwBBSBS] 28 \begin{tabular}{|l|l|l|} \hline 29 & & Weight \\ \hline 30 & wS & 0.6858 \\ \hline 31 & wB & 0.3142 \\ \hline 32 & E(rP) & 13.115 \\ \hline 33 & SD & 24.112 \\ \hline \end{tabular} A B C D 37 optimal risky portfolio wB=[E(rB)rf]s2+[E(rs)rf]B2[E(rB)rf+E(rs)rf]BSBS[E(rB)rf]s2[E(rs)rf]BsBSwS=1wB \begin{tabular}{|l|l|l|} \hline 38 & & \\ \hline 39 & & Weight \\ \hline 40 & wS & 0.3534 \\ \hline 41 & wB & 0.6466 \\ \hline 42 & E(rO) & 11.120 \\ \hline 43 & O & 19.988 \\ \hline \end{tabular} 4.) reward-to-volatility ratio of portfolio O S0=0E(r0)rf 48 \begin{tabular}{|l|l|l|} \hline 49 & E(ro) & 11.120 \\ \hline 50 & o & 19.988 \\ \hline 51 & Sharp ratio & 0.2812 \\ \hline \end{tabular} 1.) 2.) minimal variance portfolio P=[(wSS)2+(wBB)2+2wSwBBSBS] 28 \begin{tabular}{|l|l|l|} \hline 29 & & Weight \\ \hline 30 & wS & 0.6858 \\ \hline 31 & wB & 0.3142 \\ \hline 32 & E(rP) & 13.115 \\ \hline 33 & SD & 24.112 \\ \hline \end{tabular} A B C D 37 optimal risky portfolio wB=[E(rB)rf]s2+[E(rs)rf]B2[E(rB)rf+E(rs)rf]BSBS[E(rB)rf]s2[E(rs)rf]BsBSwS=1wB \begin{tabular}{|l|l|l|} \hline 38 & & \\ \hline 39 & & Weight \\ \hline 40 & wS & 0.3534 \\ \hline 41 & wB & 0.6466 \\ \hline 42 & E(rO) & 11.120 \\ \hline 43 & O & 19.988 \\ \hline \end{tabular} 4.) reward-to-volatility ratio of portfolio O S0=0E(r0)rf 48 \begin{tabular}{|l|l|l|} \hline 49 & E(ro) & 11.120 \\ \hline 50 & o & 19.988 \\ \hline 51 & Sharp ratio & 0.2812 \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Have More Money Now A Commonsense Approach To Financial Management

Authors: John Layfield

1st Edition

0743466330,1416595775