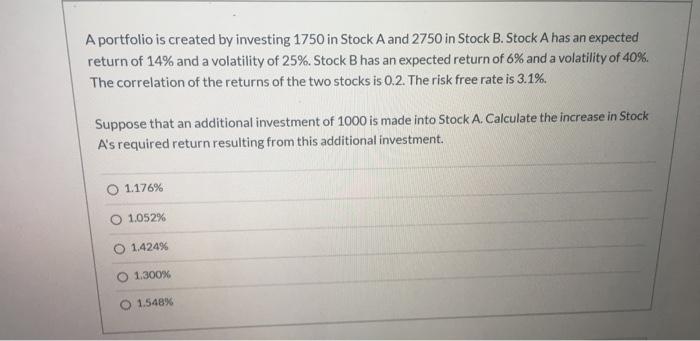

A portfolio is created by investing 1750 in Stock A and 2750 in Stock B. Stock A has an expected return of 14% and

A portfolio is created by investing 1750 in Stock A and 2750 in Stock B. Stock A has an expected return of 14% and a volatility of 25%. Stock B has an expected return of 6% and a volatility of 40%. The correlation of the returns of the two stocks is 0.2. The risk free rate is 3.1%. Suppose that an additional investment of 1000 is made into Stock A. Calculate the increase in Stock A's required return resulting from this additional investment. O 1.176% 1.052% 1.424% O 1.300% O 1.548%

Step by Step Solution

3.40 Rating (159 Votes )

There are 3 Steps involved in it

Step: 1

Answer A 1176 Answer basically everything that the other person said but the first ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Stephen Ross, Randolph Westerfield, Bradford Jordan

9th edition

978-0077459451, 77459458, 978-1259027628, 1259027627, 978-0073382395