Answered step by step

Verified Expert Solution

Question

1 Approved Answer

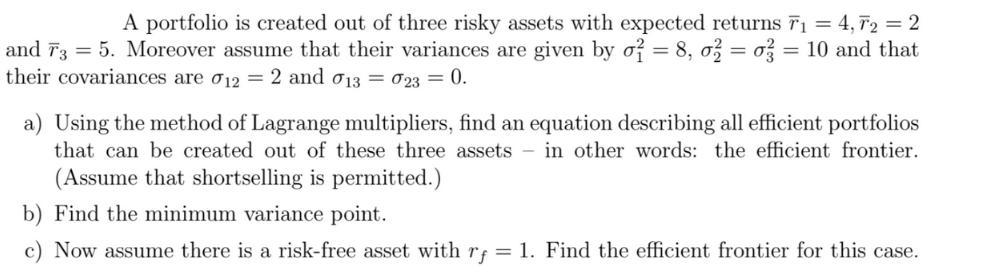

A portfolio is created out of three risky assets with expected returns 7 = 4,7 = 2 and 73 = 5. Moreover assume that

A portfolio is created out of three risky assets with expected returns 7 = 4,7 = 2 and 73 = 5. Moreover assume that their variances are given by o2 = 8, o2 = 0 = 10 and that their covariances are 12 = 2 and 13 = 023 = 0. a) Using the method of Lagrange multipliers, find an equation describing all efficient portfolios that can be created out of these three assets in other words: the efficient frontier. (Assume that shortselling is permitted.) b) Find the minimum variance point. c) Now assume there is a risk-free asset with rf = 1. Find the efficient frontier for this case.

Step by Step Solution

★★★★★

3.41 Rating (157 Votes )

There are 3 Steps involved in it

Step: 1

a Let w1 w2 and w3 be the weights of the three assets in the portfolio respectively The expected return of the portfolio is then given by rp w1 overli...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516