Answered step by step

Verified Expert Solution

Question

1 Approved Answer

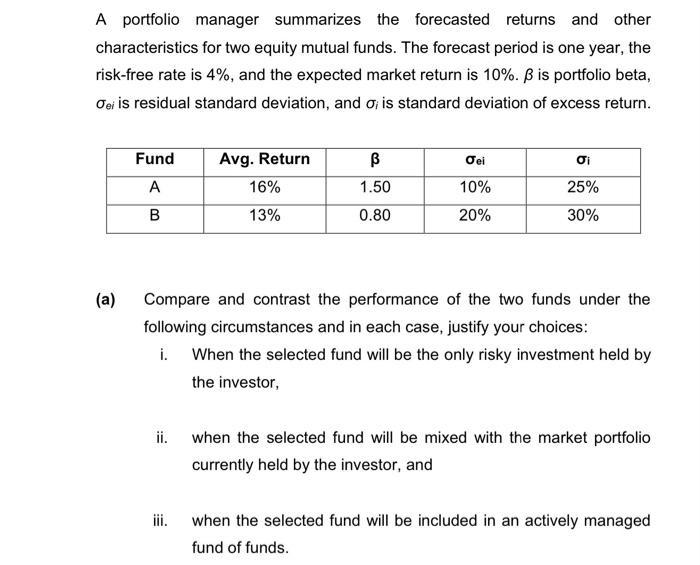

A portfolio manager summarizes the forecasted returns and other characteristics for two equity mutual funds. The forecast period is one year, the risk-free rate

A portfolio manager summarizes the forecasted returns and other characteristics for two equity mutual funds. The forecast period is one year, the risk-free rate is 4%, and the expected market return is 10%. is portfolio beta, Jei is residual standard deviation, and o; is standard deviation of excess return. (a) Fund A B Avg. Return 16% 13% ii. 1.50 0.80 Jei 10% 20% i 25% 30% Compare and contrast the performance of the two funds under the following circumstances and in each case, justify your choices: i. When the selected fund will be the only risky investment held by the investor, when the selected fund will be mixed with the market portfolio currently held by the investor, and when the selected fund will be included in an actively managed fund of funds.

Step by Step Solution

★★★★★

3.36 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

i When the selected fund will be the only risky investment held by the investor To compare the performance of the two funds we need to calculate their ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

9th Edition

73530700, 978-0073530703