Answered step by step

Verified Expert Solution

Question

1 Approved Answer

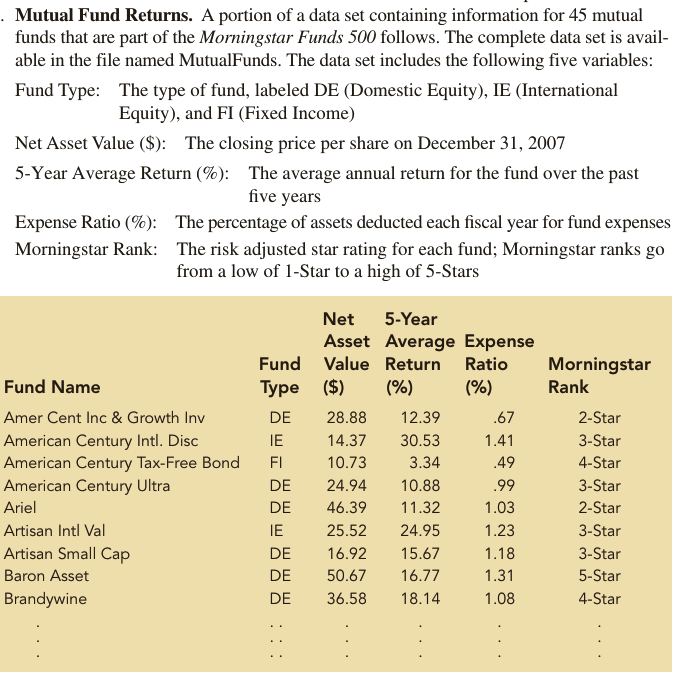

A portion of a data set containing information for 4 5 mutual funds that are part of the Morningstar Funds 5 0 0 follows. The

A portion of a data set containing information for mutual funds that are part of the Morningstar Funds follows. The complete data set is available in the file named MutualFunds. The data set includes the following five variables:

Fund Type: The type of fund, labeled DE Domestic Equity IE International

Equity and FI Fixed Income Net Asset Value $: The closing price per share on December

Year Average Return : The average annual return for the fund over the past five years

Expense Ratio : The percentage of assets deducted each fiscal year for fund expenses

Morningstar Rank: The risk adjusted star rating for each fund; Morningstar ranks go

from a low of Star to a high of Stars

a Develop an estimated regression equation that can be used to predict the yearaverage return given the type of fund. At the level of significance, test for a significant relationship.

b Did the estimated regression equation developed in part a provide a good fit to the data? Explain.

c Develop the estimated regression equation that can be used to predict the year average return given the type of fund, the net asset value, and the expense ratio. At the level of significance, test for a significant relationship. Do you think any variables should be deleted from the estimated regression equation? Explain.

d Morningstar Rank is a categorical variable. Because the data set contains only

funds with four ranks Star through Star use the following dummy variables:

StarRank for a Star fund, otherwise; StarRank for a Star fund,

otherwise; and StarRank for a Star fund, otherwise. Develop an estimated regression equation that can be used to predict the year average return given the type of fund, the expense ratio, and the Morningstar Rank. Using remove any independent variables that are not significant.

e Use the estimated regression equation developed in part d to predict the year average return for a domestic equity fund with an expense ratio of and a

Star Morningstar Rank.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Finance Transactions Policy And Regulation

Authors: Hal Scott, Anna Gelpern

20th Edition

1609303164, 978-1609303167