Question

A recently graduated M.B.A., Mark Thomas, had been hired three months ago as assistant direc- tor of the Abbington Youth Center. Prior to earning his

A recently graduated M.B.A., Mark Thomas, had been hired three months ago as assistant direc-

tor of the Abbington Youth Center. Prior to earning his M.B.A., he had worked in several manufac-

turing firms, but he had never worked in a nonprofit organization. He knew little about Abbington's

programs or the educational and social theories in use by the professional staff, but had decided to

take the job since he had been impressed with the Center's attempts to provide high-quality pro-

grams for the children in his community.

Despite his lack of experience in organizations like Abbington, Mr. Thomas had brought some

much-needed management skills to the centers operations. In his short tenure he not only had in-

troduced some new management techniques, but had regularly made attempts to educate the profes-

sional staff in the use of those techniques.

This afternoon's staff meeting was no exception. In attendance would be the center's director,

Helen Fineberg, and the coordinators of the center's three programs: Fiona Mosteller (Infants and

Toddlers Program), Joanne Olivo (Preschool Program), and Don Harris (After-School Program).

As the names suggested, each program was aimed toward a different age-group: the first accepted

children up to the age of three; the second from three to five years of age; and the third from five to

seven years.

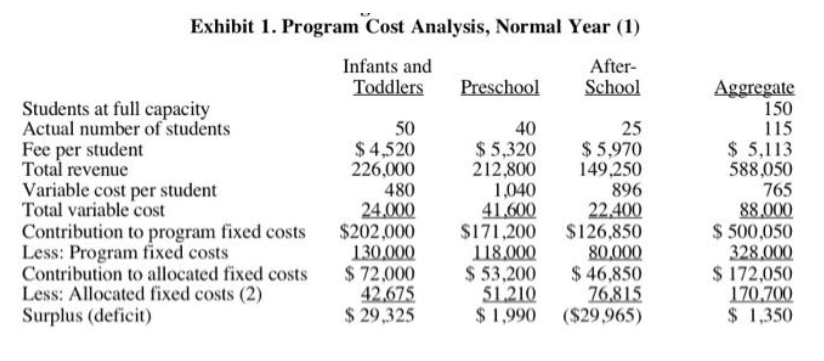

Mr. Thomas planned to instruct the program directors in the concept of breakeven analysis; in

order to do so, he had gathered some data on the revenues and costs of the three programs (see Ex-

hibit 1). Using this information, he determined that each student contributed $4,348 to fixed costs

after covering his or her variable costs. Given the fixed costs of $498,700 ($328,000 in the pro-

grams and $170,700 for the center overall), he had calculated that 115 students were needed to

break even.

He had prepared the breakeven chart, shown in Exhibit 2, which he planned to distribute to eve-

ryone at the meeting prior to giving a short lecture on the concept of breakeven analysis. His intent

was to make clear to everyone that enrollment was exactly at breakeven, which did not allow any

margin of safety, and to encourage the program directors to expand the size of their programs by a

few students each so as to provide a more comfortable margin and, if all went well, a substantial

surplus for the center.

The Meeting

At the meeting, several issues arose that Mr. Thomas had not anticipated, and a rather hostile at-

mosphere developed. Ms. Mosteller pointed out that 50 students was the maximum her program

could accommodate, given current classroom space, and wondered exactly how Mr. Thomas ex-

pected her to increase the program's size. Ms. Olivo said she would be happy to expand her pro-

gram by another 10 students, but in order to do so, she would need to hire another teacher, at a cost

of $22,000. She wondered how Mr. Thomas might include this fact in his analysis, and, under the

circumstances, whether the teacher should be considered a fixed or a variable cost. Mr. Harris told

Mr. Thomas that he had been planning all along to add another 15 students to his program, and

wondered why Mr. Thomas had not checked with him about this prior to preparing the figures and

the chart. He too would need to hire another teacher, however, at a cost of $25,000, and also won-

dered whether this was a fixed or variable cost.

Ms. Fineberg seemed quite perplexed by the discussion, and began her comments by asking

Mr. Thomas why he was using averages when the Center had three separate programs. She also in-

dicated that $1,350 was far too low a surplus, since she was hoping to have some extra money

available during the year for painting and some minor renovations, which would cost about

$10,000. She asked Mr. Thomas how he might incorporate this need into his analysis. She also expressed some concern about Mr. Thomas's per-student fees, stating that in talking with people in

other centers she had learned that Abbington's fees were about 10 percent below what others were

charging. She thought an across-the-board increase to make up the difference was called for.

Finally, all three program directors queried Mr. Thomas about his variable-cost-per-student fig-

ure. They asked him how he had derived these figures and whether they included some recent price

increases of about 5 percent in educational supplies. Mr. Thomas stated that they included both

supplies and food, divided about 75 percent/25 percent between the two, but he confessed that he

had not included any price increase in his calculations.

Next Steps

The meeting ended on a less-than-happy note. Mr. Thomas had not had an opportunity to give

his lecture, the program managers felt frustrated that their concerns and plans had not been included

in his analysis, and Ms. Fineberg was quite upset because it appeared as though the center would

not have the funds necessary to pay for the much-needed painting and renovations.

Mr. Thomas returned to his office and wondered whether his decision to work at the center had

been a wise one. Perhaps, he thought, life would be simpler in a manufacturing firm.

Assignment

Requirements:

- Mr. Thomas is new to Abbington and has made several assumptions when building his current analysis. Discuss what assumptions he has made any concerns you have regarding his assumptions.

2. The case states that Mr. Thomas is concerned that the company is currently operating at breakeven. Explain why it is important to Mr. Thomas for Abbington to operate with a margin of safety.

3. Using Mr. Thomas information given in Exhibit 1, calculate a breakeven point for each of the three programs. Using Mr. Thomas aggregate data in Exhibit 1, calculate Abbingtons breakeven in total; prove that they are operating at breakeven based on Mr. Thomas current figures.

***Note. The aggregate information Mr. Thomas has in his exhibit is using a weighted average approach rather than a simple average; this is appropriate because each program has a different number of students and thus carries a different weight. For example, the aggregate fee per student in Mr. Thomas exhibit is $5,113, calculated as shown below:

(($4,520 * 50) + ($5,320 * 40) + ($4,970 * 25))/ 115 = $5,113

4. Rework Mr. Thomas exhibit with the changes in revenue and costs discussed at the meeting. We dont have enough information on the allocated fixed costs of $170,700 to change their allocations (meaning they will be the same in your reworked Exhibit 1 as they were when Mr. Thomas first presented this chart). Do you think it is realistic for these allocatedfixed costs to remain the same, or do you think if we had more information that they would may change as well? Does the unknown regarding these allocated fixed costs cause any concerns about this new analysis?

5. Based on your new numbers (from Requirement 4) what are the new breakeven points for each program and Abbington as a whole? With this updated information would Abbington be operating at or above breakeven? How does this impact the ending surplus or deficit that Ms. Fineberg mentioned?

6. When Mr. Thomas was given updated numbers during the meeting, we used this information to create the updated exhibit and recast the break evens in Requirements 4 and 5. Do you believe all the estimate and updates given in the meeting are reliable? Do you have any concerns with the assumptions used in these updated calculations, what could happen if these assumptions were incorrect?

Can you help me with question 6?

Exhibit 1. Program Cost Analysis, Normal Year (1)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysing The Value Proposition Of The Audit Process In Africa The Case Of Malawi

Authors: Daniel Dunga

1st Edition

3659166286, 978-3659166280