Answered step by step

Verified Expert Solution

Question

1 Approved Answer

CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities,

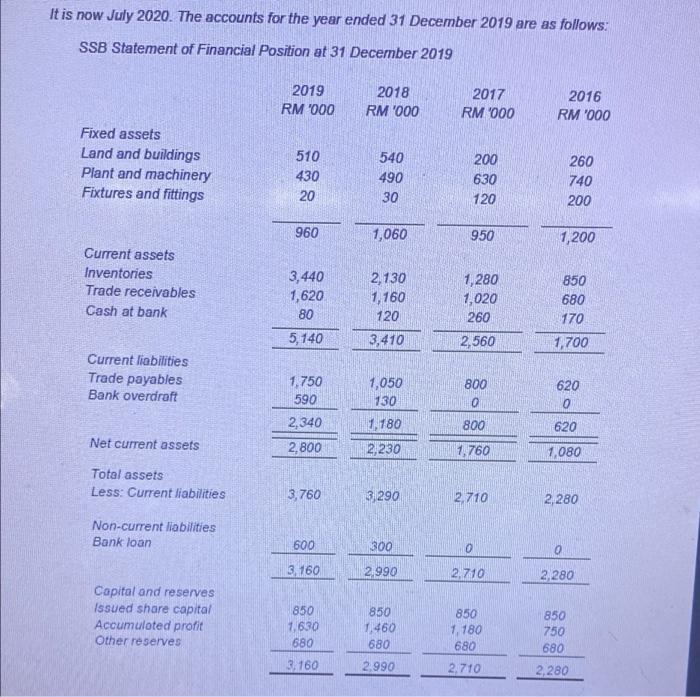

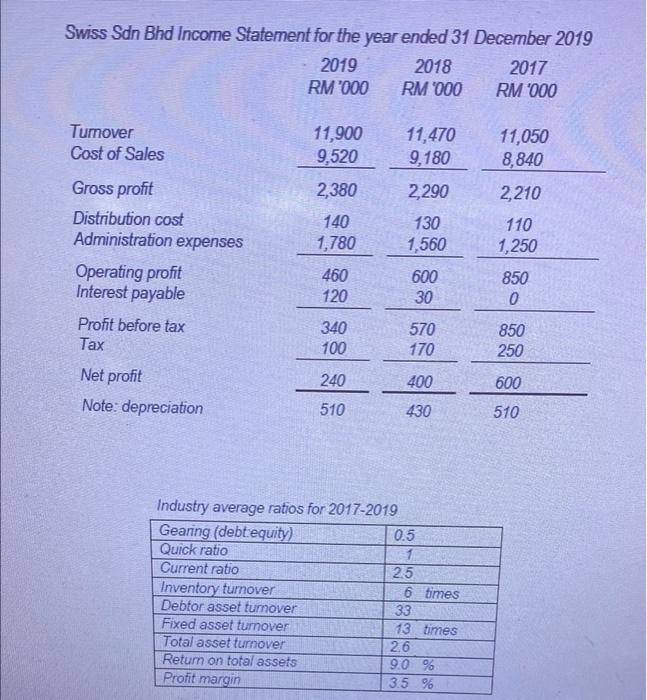

CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks)

Step by Step Solution

★★★★★

3.26 Rating (144 Votes )

There are 3 Steps involved in it

Step: 1

Solution As per managing director by giving entre loan the company able to maintai...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

635e0f09e4775_181094.pdf

180 KBs PDF File

635e0f09e4775_181094.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Employment Law for Human Resource Practice

Authors: David J. Walsh

4th edition

1111972192, 978-1133710820, 1133710824, 978-1111972196