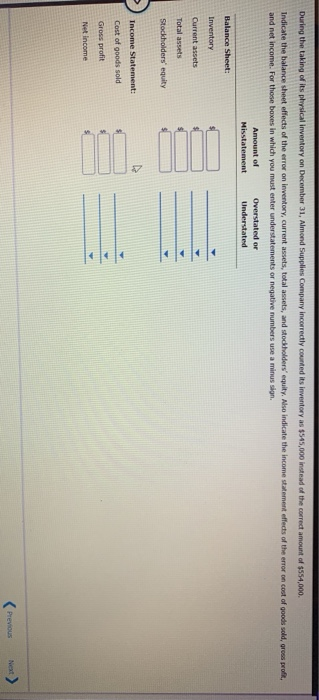

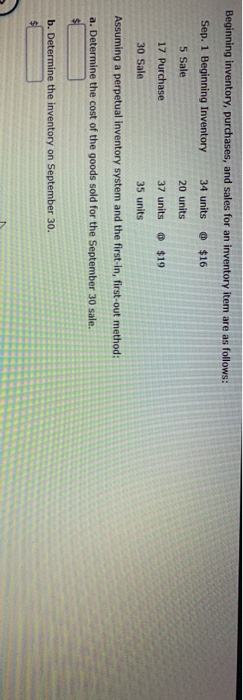

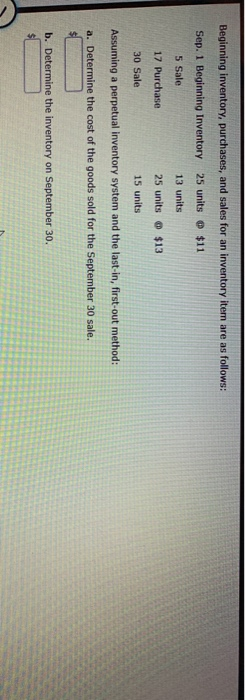

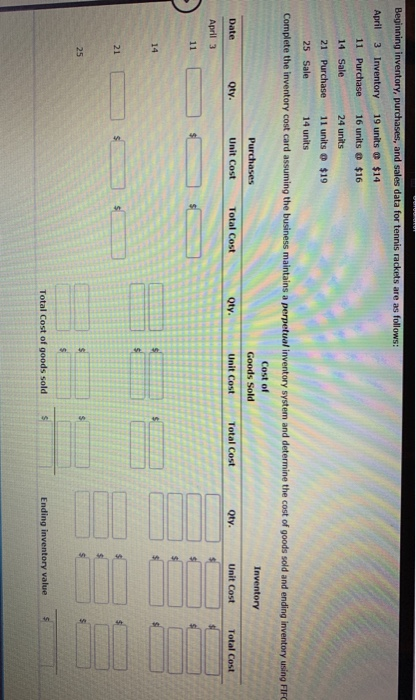

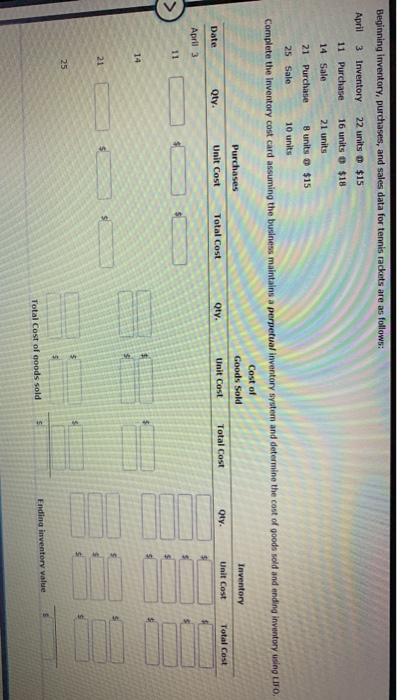

a. Sampson Co. sold merchandise to Batson Co. on account, $25,500, terms 2/15, net 45. b. The cost of the goods sold is $19,125. c. The Batson Co. paid the invoice within the discount period. Assume both Sampson and Batson use a perpetual inventory system. If no entry is required, select "No entry required" and leave the amount boxes blank. Prepare the entries that Sampson Company would record for the information above. If an amount box does not require an entry, leave it blank. Prepare the entries that Batson Company would record for the information above. If an amount box does not require an entry, leave it blank. VLJU Prepare the entries that Batson Company woul or the information above. If an amount box does not require an entry, leave it blank. During the taking of its physical Inventory on December 31, Almond Supplies Company incorrectly courted its inventory as $545,000 instead of the correct amount of $554,000. Indicate the balance sheet effects of the error on Inventory, current assets, total assets, and stockholders' equity. Also indicate the income statement effects of the error on cost of goods sold, gross profit, and net income. For those boxes in which you must enter understatements or negative numbers use a minus sign. Amount of Misstatement Overstated or Understated Balance Sheet: Current assets Total assets Stockholders' equity Income Statement: Cost of ooods sold Gross profit Net Income (Previous Next Beginning inventory, purchases, and sales for an inventory item are as follows: Sep. 1 Beginning Inventory 34 units @ $16 5 Sale 20 units 17 Purchase 37 units @ $19 30 Sale 35 units Assuming a perpetual inventory system and the first in, first-out method: a. Determine the cost of the goods sold for the September 30 sale. b. Determine the inventory on September 30. Beginning inventory, purchases, and sales for an inventory item are as follows: Sep. 1 Beginning Inventory 25 units @ $11 5 Sale 13 units 17 Purchase 25 units @ $13 30 Sale 15 units Assuming a perpetual inventory system and the last-in, first-out method: a. Determine the cost of the goods sold for the September 30 sale. b. Determine the inventory on September 30. Beginning inventory, purchases, and sales data for tennis rackets are as follows: 14 Sale April 3 Inventory 19 units $14 11 Purchase 16 units $16 24 units 21 Purchase 11 units $19 25 Sale 14 units Complete the inventory cost card assuming the business maintains a perpetual inventory system and determine the cost of goods sold and ending Inventory using FIF Cost of Purchases Inventory Goods Sold Date Qty. Unit Cost Total Cost Unit Cost Total Cost Qty. Unit Cost Total Cost April 3 11 $ $ 14 Total Cost of goods sold Ending inventory value Beginning inventory, purchases, and sales data for tennis rackets are as follows: April 3 Inventory 22 units $15 11 Purchase 16 units $18 14 Sale 21 units 21 Purchase 8 units $15 25 Sale 10 units Complete the inventory cost card assuming the business maintains a perpetual inventory system and determine the cost of goods sold and ending inventory using UFO. Cost of Inventory Purchases Unit Cost Goods Sold Unit Cost Qty. Unit Cost Qty. Total Cost Total Cost Total Cost Qty. Date April 3 Ending inventory value Total Cost of goods sold