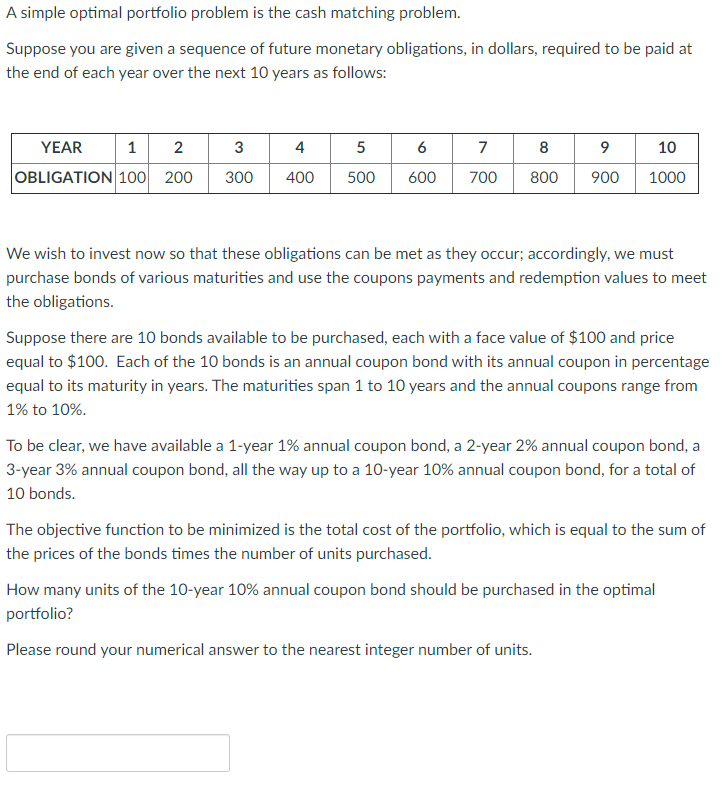

A simple optimal portfolio problem is the cash matching problem. Suppose you are given a sequence of future monetary obligations, in dollars, required to be paid at the end of each year over the next 10 years as follows: 3 4 5 6 7 8 9 10 YEAR 1 2 OBLIGATION 100 200 300 400 500 600 700 800 900 1000 We wish to invest now so that these obligations can be met as they occur, accordingly, we must purchase bonds of various maturities and use the coupons payments and redemption values to meet the obligations. Suppose there are 10 bonds available to be purchased, each with a face value of $100 and price equal to $100. Each of the 10 bonds is an annual coupon bond with its annual coupon in percentage equal to its maturity in years. The maturities span 1 to 10 years and the annual coupons range from 1% to 10%. To be clear, we have available a 1-year 1% annual coupon bond, a 2-year 2% annual coupon bond, a 3-year 3% annual coupon bond, all the way up to a 10-year 10% annual coupon bond, for a total of 10 bonds. The objective function to be minimized is the total cost of the portfolio, which is equal to the sum of the prices of the bonds times the number of units purchased. How many units of the 10-year 10% annual coupon bond should be purchased in the optimal portfolio? Please round your numerical answer to the nearest integer number of units. A simple optimal portfolio problem is the cash matching problem. Suppose you are given a sequence of future monetary obligations, in dollars, required to be paid at the end of each year over the next 10 years as follows: 3 4 5 6 7 8 9 10 YEAR 1 2 OBLIGATION 100 200 300 400 500 600 700 800 900 1000 We wish to invest now so that these obligations can be met as they occur, accordingly, we must purchase bonds of various maturities and use the coupons payments and redemption values to meet the obligations. Suppose there are 10 bonds available to be purchased, each with a face value of $100 and price equal to $100. Each of the 10 bonds is an annual coupon bond with its annual coupon in percentage equal to its maturity in years. The maturities span 1 to 10 years and the annual coupons range from 1% to 10%. To be clear, we have available a 1-year 1% annual coupon bond, a 2-year 2% annual coupon bond, a 3-year 3% annual coupon bond, all the way up to a 10-year 10% annual coupon bond, for a total of 10 bonds. The objective function to be minimized is the total cost of the portfolio, which is equal to the sum of the prices of the bonds times the number of units purchased. How many units of the 10-year 10% annual coupon bond should be purchased in the optimal portfolio? Please round your numerical answer to the nearest integer number of units