Answered step by step

Verified Expert Solution

Question

1 Approved Answer

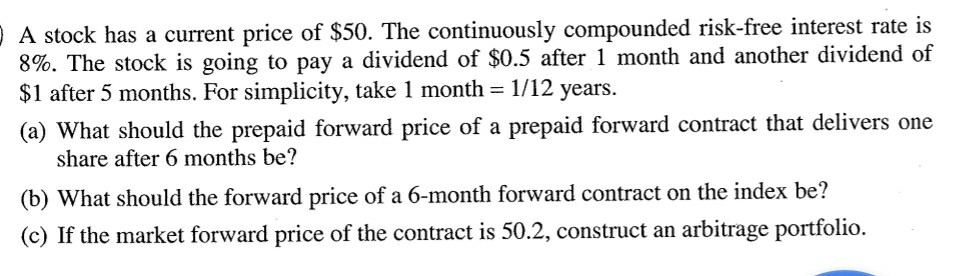

A stock has a current price of $50. The continuously compounded risk-free interest rate is 8%. The stock is going to pay a dividend of

A stock has a current price of $50. The continuously compounded risk-free interest rate is 8%. The stock is going to pay a dividend of $0.5 after 1 month and another dividend of $1 after 5 months. For simplicity, take 1 month 1/12 years. (a) What should the prepaid forward price of a prepaid forward contract that delivers one share after 6 months be? (b) What should the forwand price of a 6-month forward contract on the index be? (c) If the market forward price of the contract is 50.2, construct an arbitrage portfolio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Times Guide To Finance For Non Financial Managers

Authors: Jo Haigh

1st Edition

0273756206, 978-0273756200