Question

A stock index is currently valued at $50, and its return has a volatility of 30% per year. The continuously compounded risk-free interest rate is

A stock index is currently valued at $50, and its return has a volatility of 30% per year. The continuously compounded risk-free interest rate is 2.5% per year.

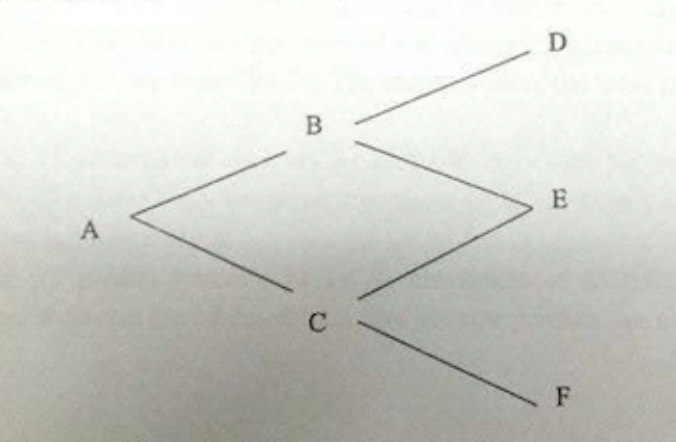

a) Use a binomial model with two steps to describe the evolution of stock prices for the next two months. Specify the stock price at each node in the binomial three above. b) Determine the price of a European call option with two months maturity and a strike price of $55.

c) What is the delta at node B for this call option? d) Determine the price of an American put option with the same strike price and time to maturity. And whats the put options delta at node A?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Performance Measurement In Finance

Authors: John Knight, Stephen Satchell, Nathalie Farah

1st Edition

0750650265, 978-0750650267