Answered step by step

Verified Expert Solution

Question

1 Approved Answer

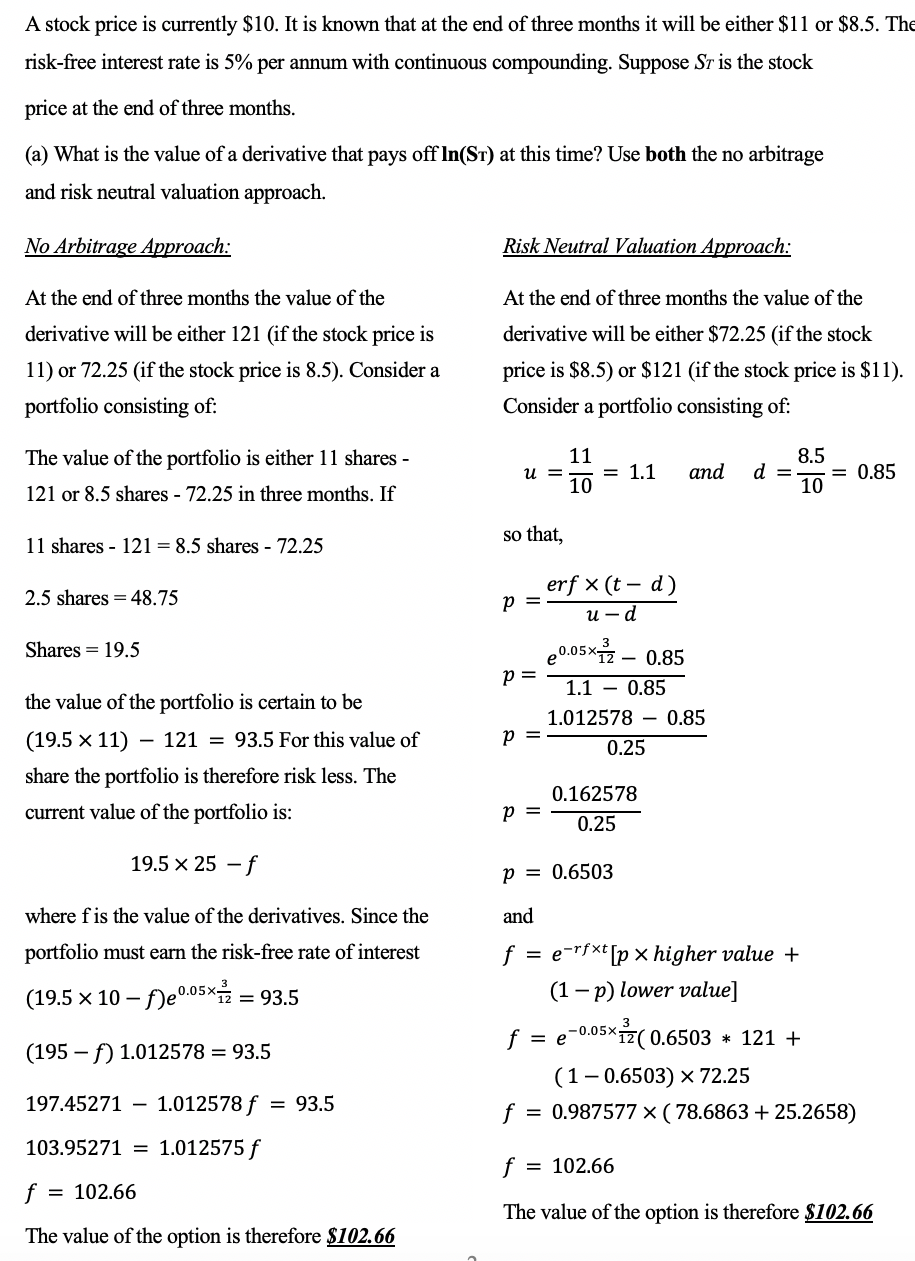

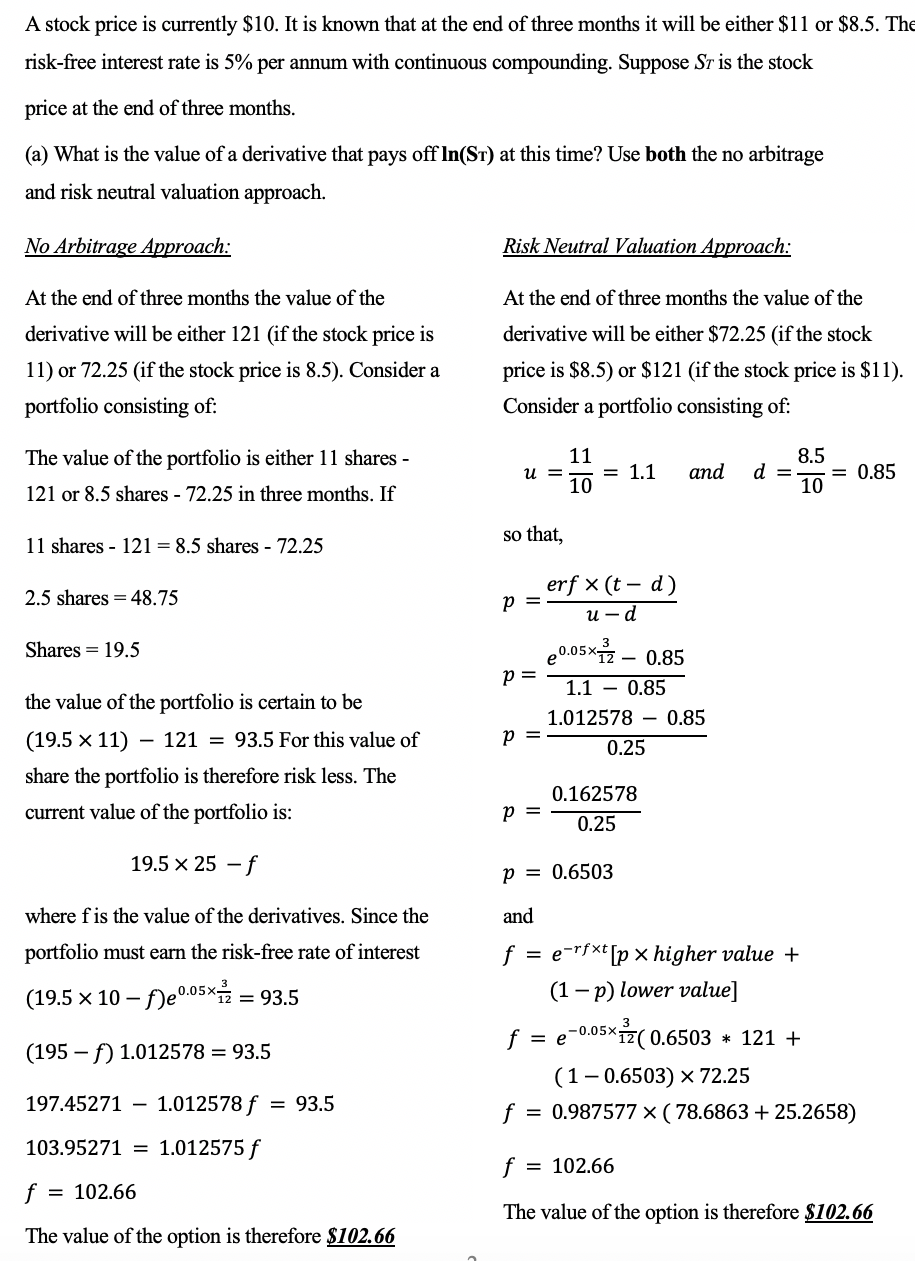

A stock price is currently $10. It is known that at the end of three months it will be either $11 or $8.5. Th risk-free

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Case Studies in Finance Managing for Corporate Value Creation

Authors: Robert F. Bruner, Kenneth Eades, Michael Schill

7th edition

007786171X, 77861711, 978-0077861711