Answered step by step

Verified Expert Solution

Question

1 Approved Answer

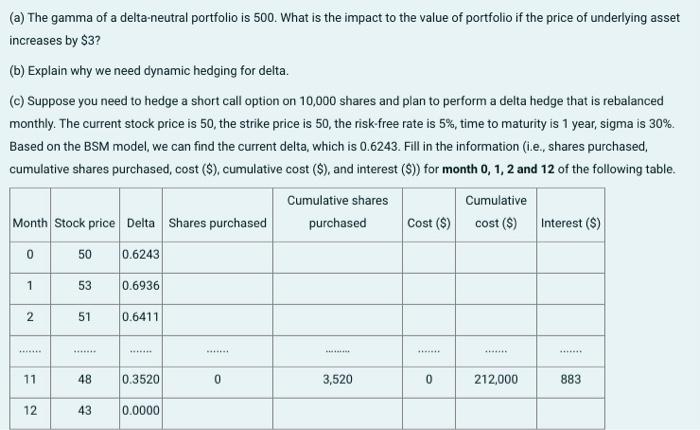

(a) The gamma of a delta-neutral portfolio is 500. What is the impact to the value of portfolio if the price of underlying asset increases

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Money Management And Financial Budgeting 2 Books In 1 A Beginners Guide On Managing Bad Credit Debt Savings And Personal Finance

Authors: Robert Anderson

1st Edition

1386959006, 978-1386959007