Question

A UK based client holds a welldiversified equity portfolio which has finally regained all the value it lost during the recent COVID19 related crash. The

A UK based client holds a welldiversified equity portfolio which has finally regained all the value it lost during the recent COVID19 related crash. The portfolio is currently worth 75 million and has a market beta of 1.5. Moreover, the expected dividend yield on the equity portfolio is 3.3% per annum with simple compounding. The client is concerned about a further downturn in the market as she thinks the recent bull market rally does not truly reflect the underlying economic reality. She has therefore requested your advice on how best to protect the value of her portfolio going forward, while still benefitting if the bull market continues. The FTSE100 index is currently at 5,969 and the dividend yield of the FTSE100 index is 2.1% per annum with simple compounding. The riskfree interest rate is 0.3% per annum with continuous compounding for all maturities. Available index options are quoted in increments of 25 index points and the multiplier (per point) for each option contract is equal to 10.

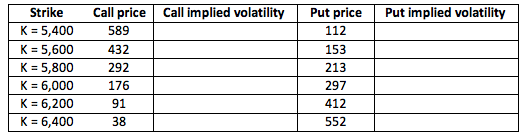

(c) Use Excel's GoalSeek (or otherwise) to estimate the implied volatility of the index, based on market prices of threemonth European call and put options on the index. Specifically, complete the following table with the estimated implied volatilities (to 3 significant figures). Note you will need information stated earlier in the question to do this: 111.png You should also answer the following questions: i. Plot the implied volatility as a function of the strike price. ii. Are the option prices consistent with the assumptions underlying the BlackScholes model? Does the implied volatility depend on the moneyness of the option? Explain. iii. Is the implied volatility of one option class higher than the other? If so, explain why. Call implied volatility Put implied volatility Strike K = 5,400 K = 5,600 K = 5,800 K = 6,000 K = 6,200 K = 6,400 Call price

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started