Answered step by step

Verified Expert Solution

Question

1 Approved Answer

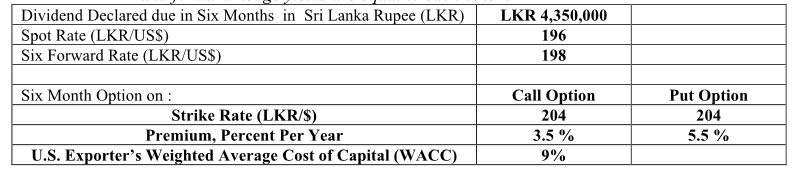

A U.S. investor will receive dividend from a Sri Lankan coconut exporting company but worries about the depreciation of the Sri Lankan Rupee in six

A U.S. investor will receive dividend from a Sri Lankan coconut exporting company but worries about the depreciation of the Sri Lankan Rupee in six months due to the expectation in the interest rate rises by the Fed.

Keeping option premium fixed, what is the strike rate at which both options hedge and forward hedge yields are equal to each other? (according to table)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started