Answered step by step

Verified Expert Solution

Question

1 Approved Answer

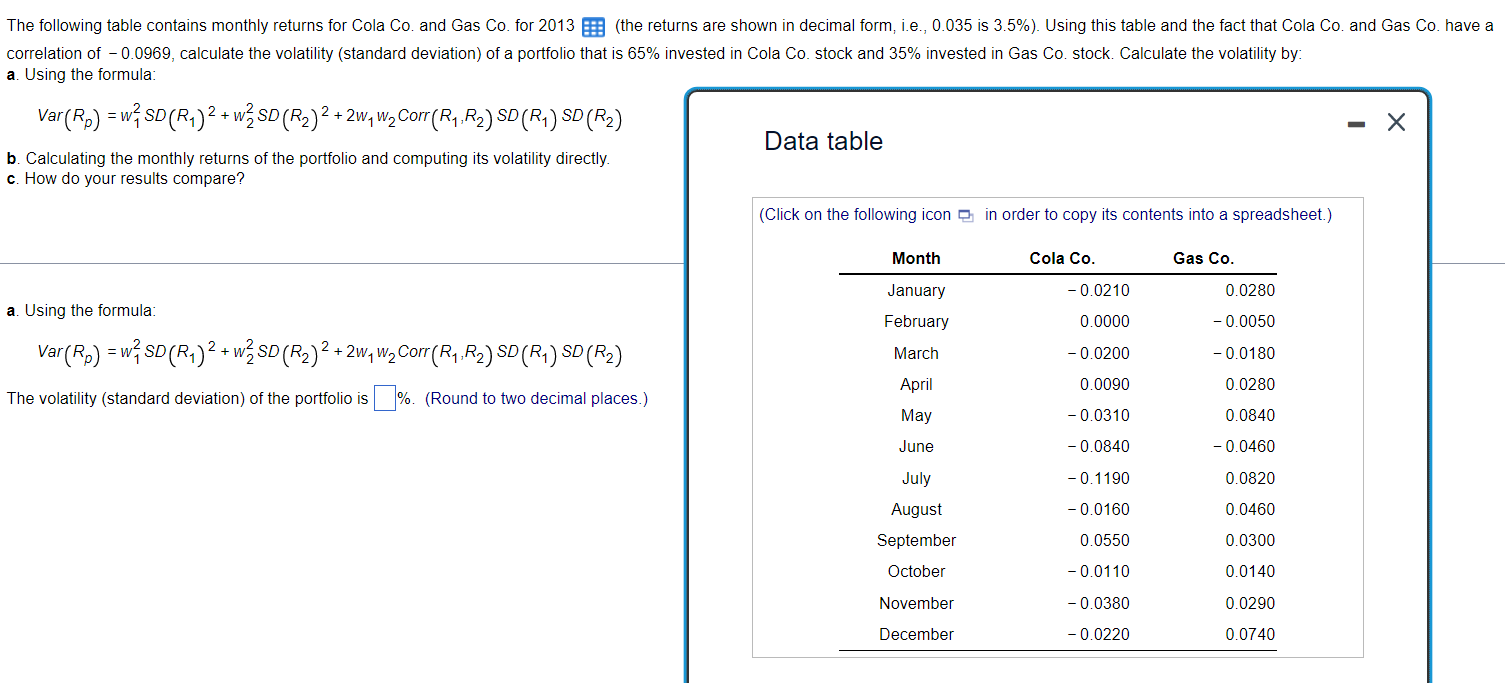

a. Using the formula: Var(Rp)=w12SD(R1)2+w22SD(R2)2+2w1w2Corr(R1,R2)SD(R1)SD(R2) b. Calculating the monthly returns of the portfolio and computing its volatility directly. c. How do your results compare? Data

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Optimization Methods In Finance

Authors: Gerard Cornuejols, Reha Tütüncü

1st Edition

0521861705, 978-0521861700