Answered step by step

Verified Expert Solution

Question

1 Approved Answer

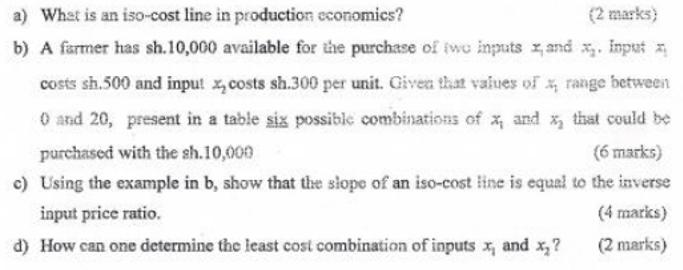

a) What is an iso-cost line in production economics? (2 marks) b) A farmer has sh.10,000 available for the purchase of two inputs x

a) What is an iso-cost line in production economics? (2 marks) b) A farmer has sh.10,000 available for the purchase of two inputs x and x. Input x costs sh.500 and input costs sh.300 per unit. Given that values of x, range between 0 and 20, present in a table six possible combinations of x and that could be purchased with the sh.10,000 (6 marks) c) Using the example in b, show that the slope of an iso-cost line is equal to the inverse input price ratio. (4 marks) d) How can one determine the least cost combination of inputs x and x2? (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a In production economics an isocost line represents all the combinations of inputs that can be purc...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Engineering Economics

Authors: Chan S. Park

5th edition

136118488, 978-8120342095, 8120342097, 978-0136118480