Answered step by step

Verified Expert Solution

Question

1 Approved Answer

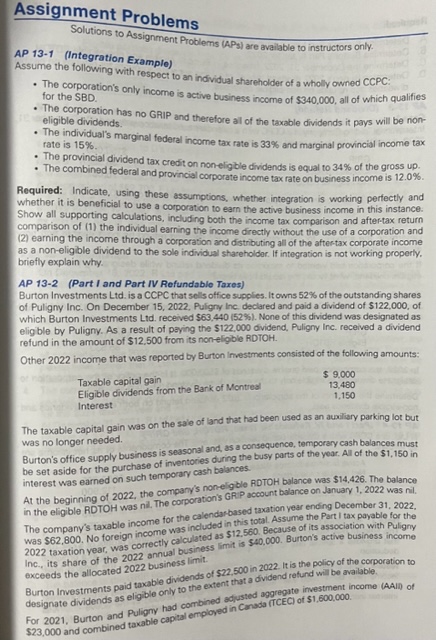

A1.2abc Wilems (APs) are avalable to instructors only. AP 13-1 (Integration Example) Assume the following with respect to an individual shareholder of a wholly owned

A1.2abc

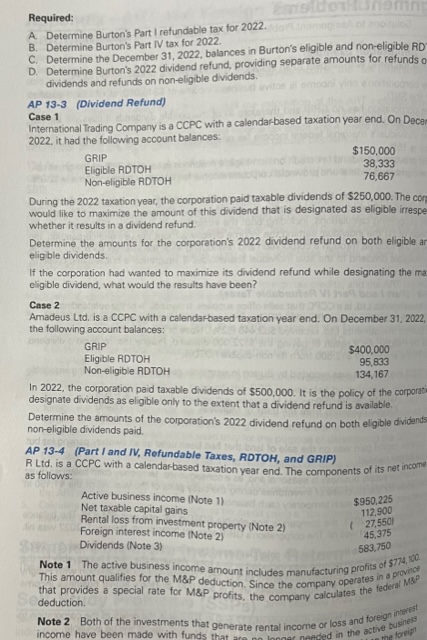

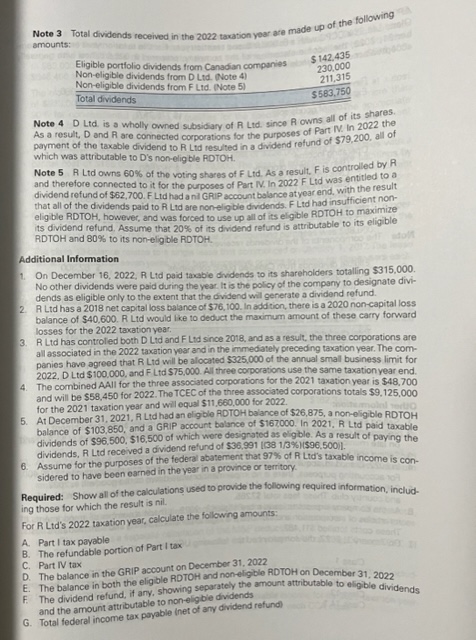

Wilems (APs) are avalable to instructors only. AP 13-1 (Integration Example) Assume the following with respect to an individual shareholder of a wholly owned CCPC: - The corporation's only income is active business income of $340,000, all of which qualifies for the SBD. - The corporation has no GRIP and therefore al of the taxable dividends it pays will be noneligible dividends. - The individual's marginal federal income tax rate is 33% and marginal provincial income tax rate is 15%. - The provincial dividend tax credit on non-ligble dividends is equal to 34% of the gross up. - The combined federal and provincial corporate income tax rate on business income is 12.0%. Required: Indicate, using these assumptions, whether integration is working perfectly and whether it is beneficial to use a corporation to earn the active business income in this instance. Show all supporting calculations, including both the income tax comparison and aftertax return comparison of (1) the individual earning the income directly without the use of a corporation and (2) earning the income through a corporation and distributing all of the aftertax corporate income as a non-eligible dividend to the sole individual shareholdar. If integration is not working properly. briefly explain why. AP 13-2 (Part I and Part IV Refundable Taxes) Burton Investments Ltd. is a CCPC that sells office supplies. It owns 52% of the outstanding shares of Puligny Inc. On December 15, 2022, Puligny Inc declared and paid a dividend of $122,000, of which Burton Investments Lid. received $63,440(52%). None of this dividend was designated as eligble by Puligny. As a result of paying the $122,000 dividend, Puligny Inc. received a dividend refund in the amount of $12,500 from its noneligble RDTOH. Other 2022 income that was reported by Burton Investments consistod of the following amounts: The taxable capital gain was on the sale of land that had been used as an awailiary parking lot but was no longer needed. Burton's office supply business is seasonal and, as a consequence, temporary cash balances must be set aside for the purchase of inventories during the busy parts of the year. All of the $1,150 in interest was earned on such temporary cash balances. At the beginning of 2022, the company's noneligble RDTOH balance was $14,426. The balance in the eligible RDTOH was nil. The corporation's GR.P account balance on January 1,2022 was nil. The company's taxable income for the calendarbased taxation year ending December 31, 2022, The company's taxable income for the caiendartased taxation year the Part I tax payable for the 2022 taxation year, was correctly calculated as $12.560. Because of its association with Puligny Inc., its share of the 2022 annual business limit is 5:0,000. Burton's active business income exceeds the allocated 2022 business limit. Burton Investments paid taxable dividends of $22,500 in 2022 . It is the policy of the corporation to designate dividends as eligible only to the extent that a dividend refund will be available. For 2021, Burton and Puligny had combined adjusted aggregate investment income (AAII) of $23,000 and combined taxable capial employed in Conada (TCEC) of $1,600,000. Required: A. Determine Burton's Part I refundable tax for 2022. B. Determine Burton's Part IV tax for 2022. C. Determine the December 31,2022, balances in Burton's eligible and non-eligible RD D. Determine Burton's 2022 dividend refund, providing separate amounts for refunds 0 dividends and refunds on noneligible dividends. AP 13-3 (Dividend Refund) Case 1 International Trading Company is a CCPC with a calendarbased taxation year end. On Dece 2022, it hat the finllmwinn anmunt balances: During the 2022 taxation year, the corporation paid taxable dividends of $250,000. The con would like to maximize the amount of this dividend that is designated as eligible irrespe whether it results in a dividend refund. Determine the amounts for the corporation's 2022 dividend refund on both eligible ar eligble dividends. If the corporation had wanted to maximize its dividend refund while designating the ma eligble dividend, what would the results have been? Case 2 Amadeus Ltd. is a CCPC with a calendarbased taxation year end. On December 31, 2022, the following account balances: In 2022, the corporation paid taxable dividends of $500,000. It is the policy of the corporat designate dividends as eligible only to the extent that a dividend refund is available. Determine the amounts of the corporation's 2022 dividend refund on both eligible dvidands non-eligible dividends paid. AP 13-4 (Part I and IV, Refundable Taxes, RDTOH, and GRIP) R Ltd. is a CCPC with a calendarbased taxation year end. The components of its net income as follows: Note 1 The active business income amount includes manufacturing profits of 5774 This amount qualifies for the M\&P deduction. Since the company operates in a provinge that provides a special rate for M\&P profits, the company calculates the federal MSP deduction. Note 2 Both of the investments that generate rental income or loss and foreign incerest Note 3 Total dividends received in the 2022 taxation year are made up of the following amounts: Note 4 D Ltd is a wholly owned subsidiary of A Ltd. since R owns all of its shares. As a result, D and A are connected corporations for the purposes of Part N. in 2022 the payment of the taxable cividend to R Ltd resulted in a dividend refund of $79,200, all of which was attributable to D's non-eligble ROTOH. Note 5 . R Ltd owns 60% of the voting shares of F Ltd. As a result, F is controlled by R and therefore connected to it for the purposes of Part IN. In 2022 F Lid was entitled to a dividend refund of $62,700. F Ltd had a nil GRIP account bolance atyear end, with the result. that all of the dividends paid to R Ltd are noneligble dividends. F Ltd had insutficient noneligible RDTOH, however, and was forced to use up all of its eligible RDTOH to maximize its dividend refund. Assume that 20% of its dividend refund is attributable to its eligible RDTOH and 80% to its non-eligble RDTOH. Additional Information 1. On December 16, 2022, R Lid paid taxable dividends to its shareholders totalling $315,000. No other dividends were paid during the vear. It is the policy of the company to designate dividends as eligible only to the extent that the dividend will generate a dividend refund. 2. R Ltd has a 2018 net capital loss balance of $76, 100. In addition, there is a 2020 non-capital loss balance of $40,600. R Lid would tike to deduct the maximum amount of these carry forward losses for the 2022 taxation year. 3. R Ltd has controled both D Lid and F Lid since 2018, and as a result, the three corporations are all associated in the 2022 taxation year and in the immedately preceding taxation year. The companies have agreed that R Lid will be alocated $325,000 of the annual small business limit for 2022, D Ltd $100,000, and F Ltd $75,000. All three corporations use the same taxation vear end. 4. The combined A. II for the three associated corporations for the 2021 taxation year is $48,700 and will be $58,450 for 2022 . The TCEC of the three associaned corporations totals $9,125,000 for the 2021 taxation year and will equal $11,660,000 for 2022 . 5. At December 31, 2021, R Ltd had an eligble ROTOH balance of $26,875, a non-eligble RDTOH balance of $103,850, and a GRIP account balance of $167000. In 2021, R Ltd paid taxcable dividends of $96,500,$16,500 of which were designstod as eligble. As a result of paying the dividends, F Ltd received a dividend refund of $36,991 [(S8 1/3\%) ($96,500). 6. Assume for the purposes of the federal abatement that 97% of R Ltd's taxable income is considered to have been earned in the year in a province or territory. Required: Show all of the calculations used to provide the following required information, including those for which the result is nil. For R Ltd's 2022 taxation year, calculate the following amounts: A. Part I tax payable B. The refundable portion of Part I tax C. Part N tax D. The balance in the GRIP account on December 31,2022 E. The balance in both the eligible RDTOH and noneligble RDTOH on December 31, 2022 F. The dividend refund, if any, showing separately the amount attributable to eligible dividends and the amount attributable to non-eligble dividends G. Total fedoral income tax payable inet of amy dividend refund

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting A Concepts Based Introduction

Authors: David Kolitz

1st Edition

1138844977, 978-1138844971