Answered step by step

Verified Expert Solution

Question

1 Approved Answer

a-2 What is the expected value and standard deviation of its rate of return?(Do not round intermediate calculations. Enter your answers as decimals rounded to

a-2 What is the expected value and standard deviation of its rate of return?(Do not round intermediate calculations. Enter your answers as decimals rounded to 4 places.)

| Rate of return | |

| Expected return | |

| Standard deviation |

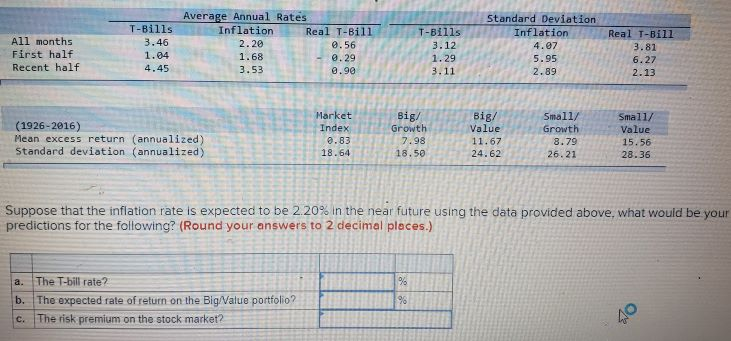

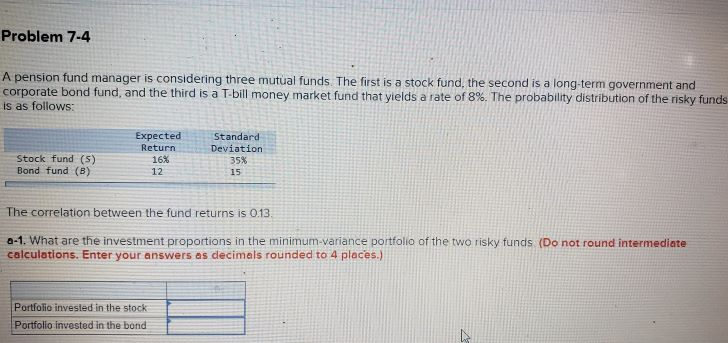

All months First half Recent half T-Bills 3.46 1.84 4.45 Average Annual Rates Inflation Real T-Bill 2.20 0.56 1.68 0.29 3.53 0.90 T-Bills 3.12 1.29 3.11 Standard Deviation Inflation 4.07 5.95 2.89 Real T-Bill 3.81 6.27 2.13 Big (1926-2016) Mean excess return (annualized) Standard deviation (annualized) Market Index 0.83 18.64 Growth 7.98 18.50 Big Value 11.67 24.62 Small/ Growth 8.79 26.21 Small/ Value 15.56 28.36 Suppose that the inflation rate is expected to be 2.20% in the near future using the data provided above, what would be your predictions for the following? (Round your answers to 2 decimal places.) % a. The T-bill rate? b. The expected rate of return on the Big/Value portfolio? c. The risk premium on the stock market? 98 Problem 7-4 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 8%. The probability distribution of the risky funds is as follows: Stock fund (5) Bond fund (B) Expected Return 16% 12 Standard Deviation 35% 15 The correlation between the fund returns is 0.13 0-1. What are the investment proportions in the minimum-variance portfolio of the two risky funds (Do not round intermediate calculations. Enter your answers as decimals rounded to 4 places.) Portfolio invested in the stock Portfolio invested in the bond

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Leverage Space Trading Model

Authors: Ralph Vince

1st Edition

0470455950, 978-0470455951