Answered step by step

Verified Expert Solution

Question

1 Approved Answer

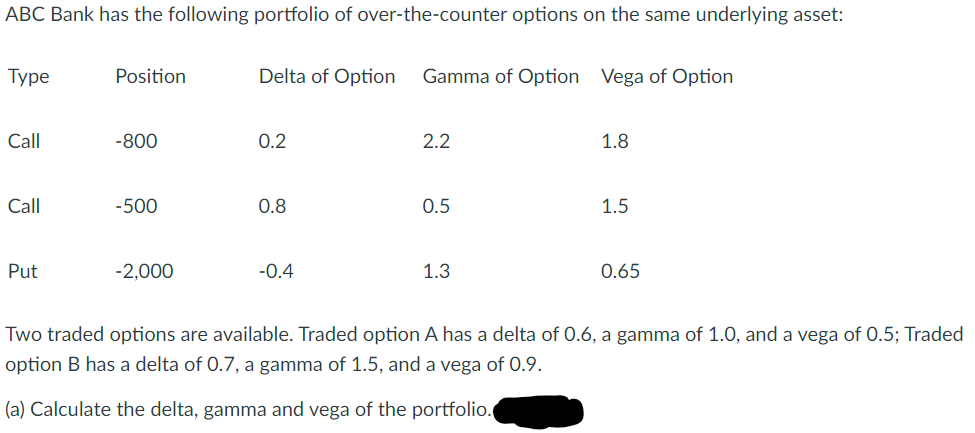

ABC Bank has the following portfolio of over-the-counter options on the same underlying asset: 1 Two traded options are available. Traded option A has a

ABC Bank has the following portfolio of over-the-counter options on the same underlying asset: 1 Two traded options are available. Traded option A has a delta of 0.6 , a gamma of 1.0, and a vega of 0.5 ; Traded option B has a delta of 0.7 , a gamma of 1.5 , and a vega of 0.9 (a) Calculate the delta, gamma and vega of the portfolio

ABC Bank has the following portfolio of over-the-counter options on the same underlying asset: 1 Two traded options are available. Traded option A has a delta of 0.6 , a gamma of 1.0, and a vega of 0.5 ; Traded option B has a delta of 0.7 , a gamma of 1.5 , and a vega of 0.9 (a) Calculate the delta, gamma and vega of the portfolio Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Criminal Capital How The Finance Industry Facilitates Crime

Authors: S. Platt

1st Edition

113733729X,1137337303