Answered step by step

Verified Expert Solution

Question

1 Approved Answer

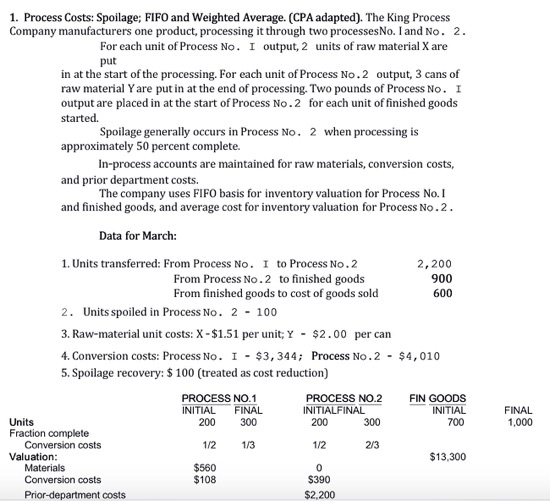

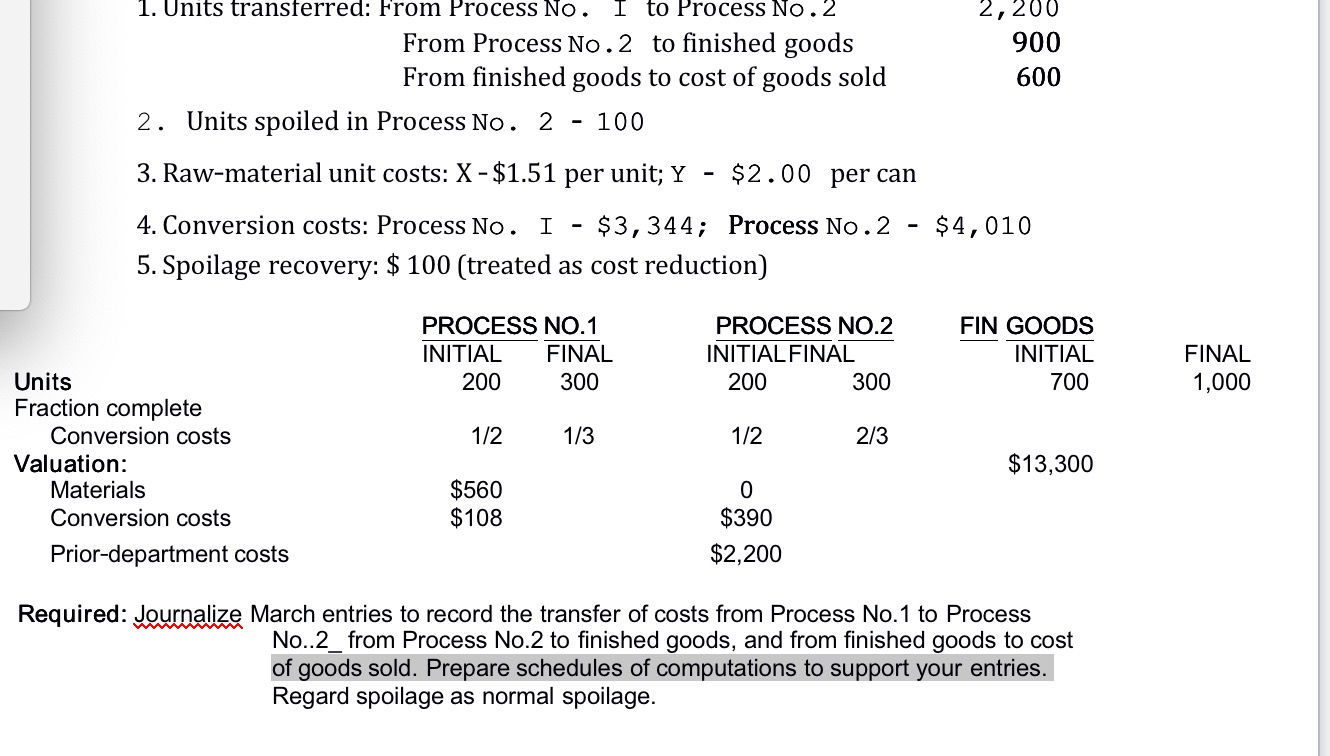

about the acctg question. the problem is the below 1. Process Costs: Spoilage; FIFO and Weighted Average. (CPA adapted). The King Process Company manufacturers one

about the acctg question. the problem is the below

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Sampling

Authors: Ray Whittington, Dan M Guy, D R Carmichael

5th Edition

047137590X, 9780471375906