Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Above is the Case study and information needed to answer this question below. 1) Calculate the impact of dropping Grill A. Assume no other changes

Above is the Case study and information needed to answer this question below.

1) Calculate the impact of dropping Grill A. Assume no other changes to the plan.

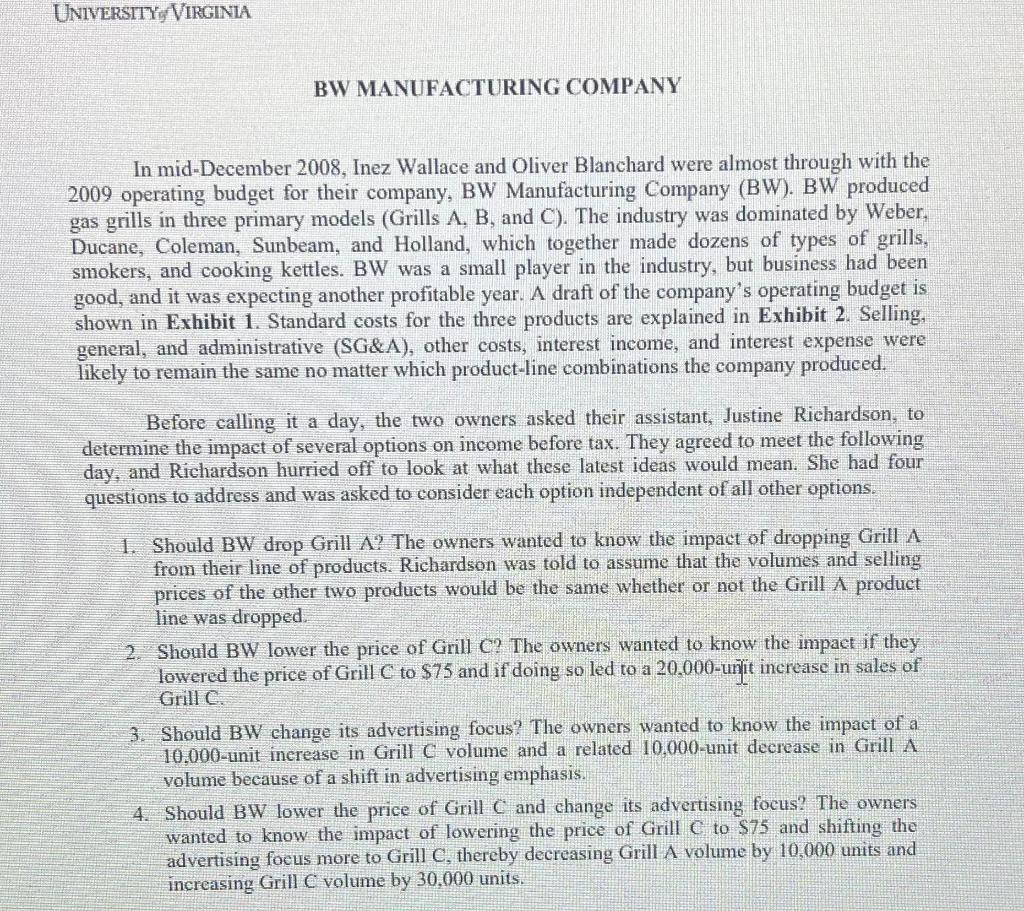

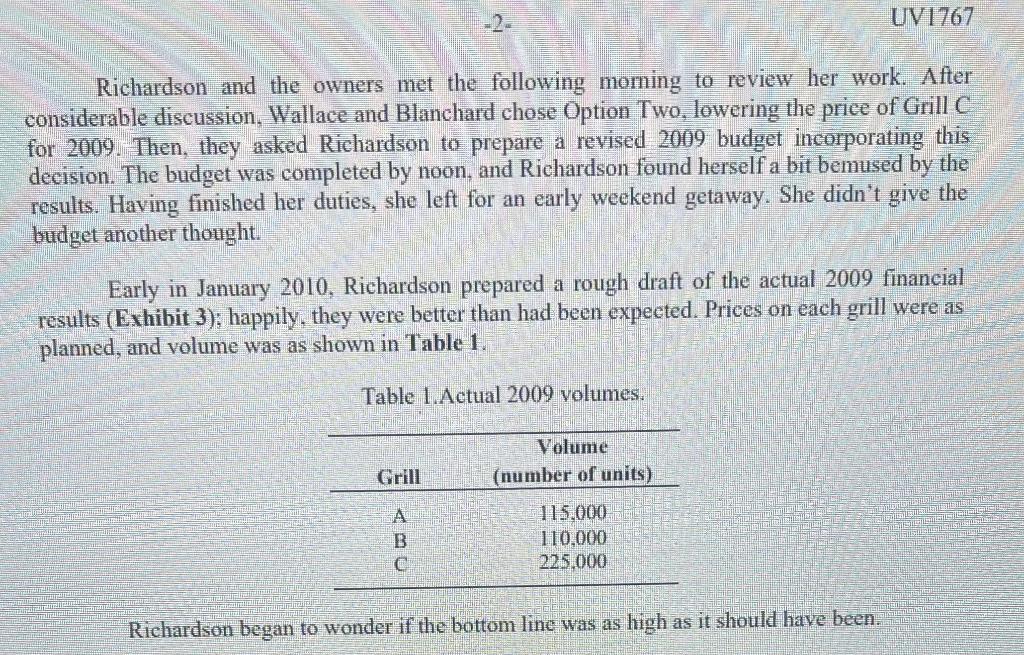

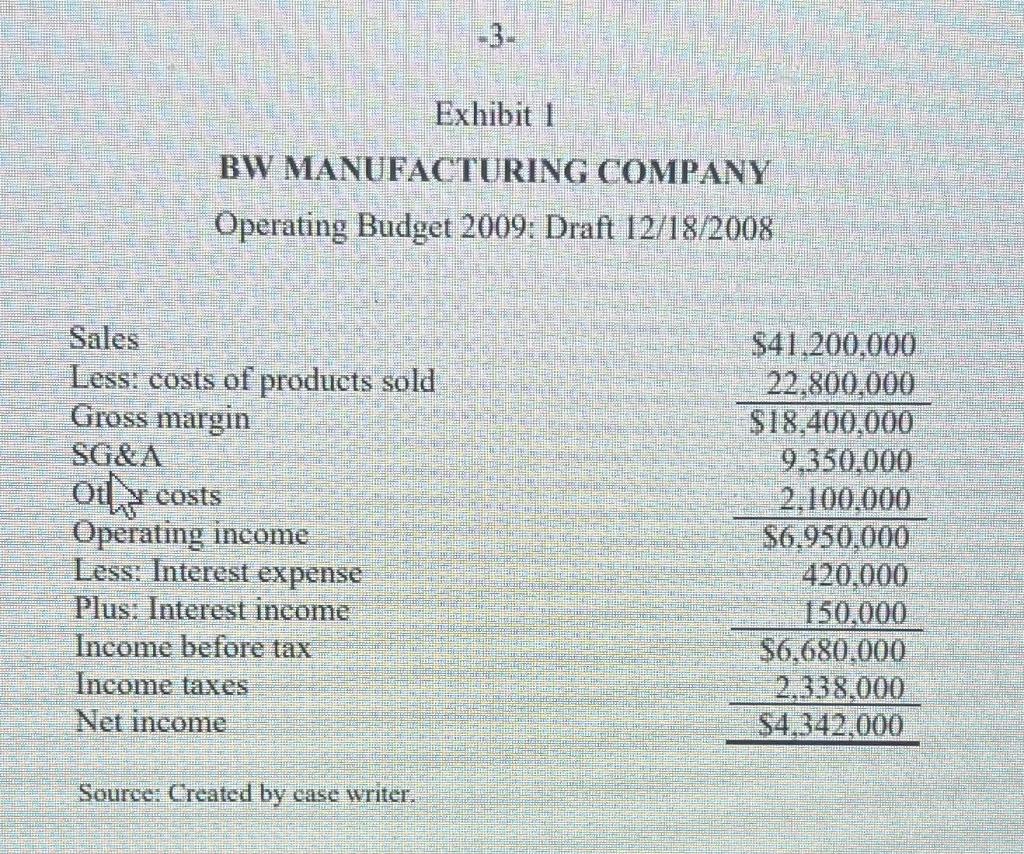

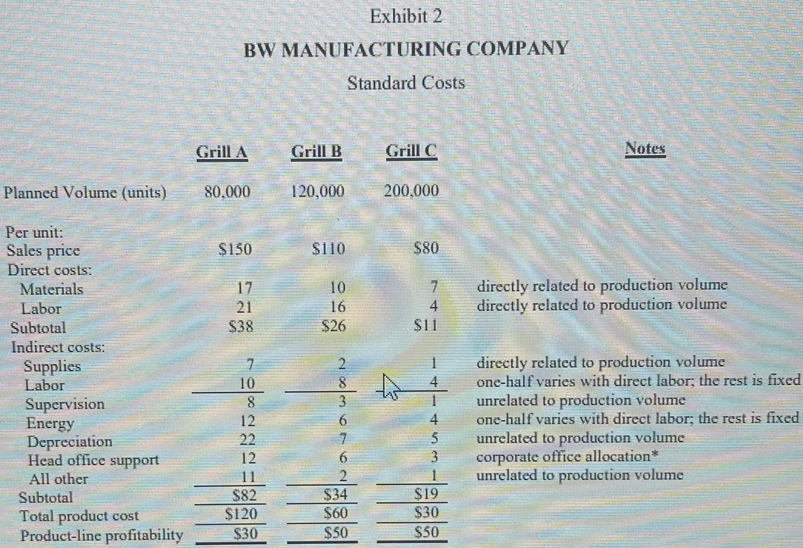

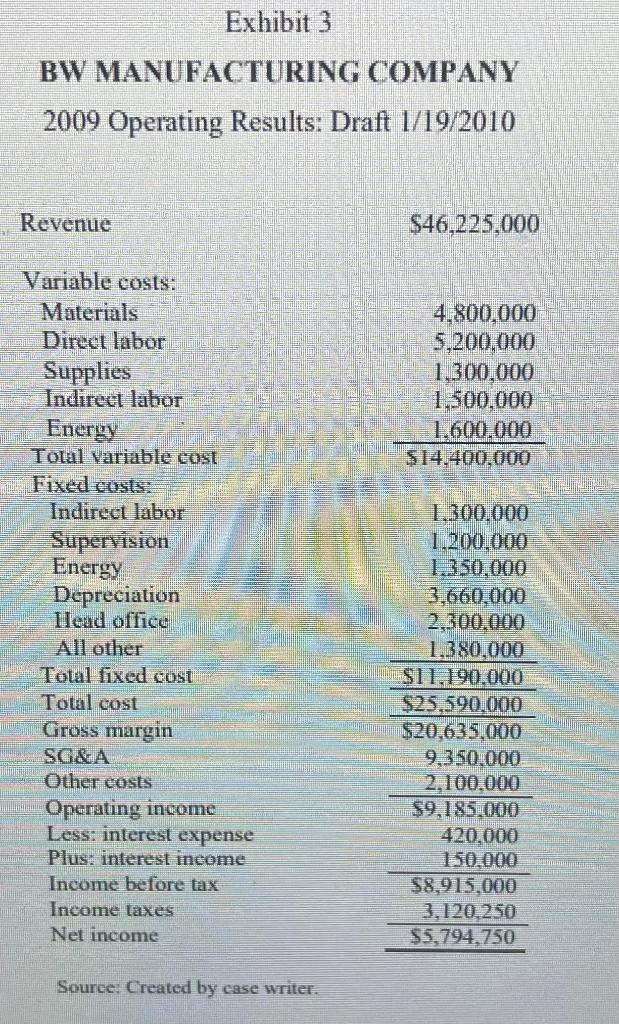

UNIVERSITY, VIRGINIA BW MANUFACTURING COMPANY In mid-December 2008, Inez Wallace and Oliver Blanchard were almost through with the 2009 operating budget for their company, BW Manufacturing Company (BW). BW produced gas grills in three primary models (Grills A, B, and C). The industry was dominated by Weber, Ducane, Coleman, Sunbeam, and Holland, which together made dozens of types of grills, smokers, and cooking kettles. BW was a small player in the industry, but business had been good, and it was expecting another profitable year. A draft of the company's operating budget is shown in Exhibit 1. Standard costs for the three products are explained in Exhibit 2. Selling, general, and administrative (SG&A), other costs, interest income, and interest expense were likely to remain the same no matter which product-line combinations the company produced. Before calling it a day, the two owners asked their assistant, Justine Richardson, to determine the impact of several options on income before tax. They agreed to meet the following day, and Richardson hurried off to look at what these latest ideas would mean. She had four questions to address and was asked to consider each option independent of all other options. 1. Should BW drop Grill A? The owners wanted to know the impact of dropping Grill A from their line of products. Richardson was told to assume that the volumes and selling prices of the other two produets would be the same whether or not the Grill A product line was dropped. 2. Should BW lower the price of Grill C? The owners wanted to know the impact if they lowered the price of Grill C to $75 and if doing so led to a 20,000-unit increase in sales of Grillc. 3. Should BW change its advertising focus? The owners wanted to know the impact of a 10.000-unit increase in Grill C volume and a related 10.000-unit decrease in Grill A volume because of a shift in advertising emphasis. 4. Should BW lower the price of Grill C and change its advertising focus? The owners wanted to know the impact of lowering the price of Grill C to $75 and shifting the advertising focus more to Grill C, thereby decreasing Grill A volume by 10,000 units and increasing Grill C volume by 30.000 units. UV1767 Richardson and the owners met the following moming to review her work. After considerable discussion, Wallace and Blanchard chose Option Two, lowering the price of Grill C for 2009. Then, they asked Richardson to prepare a revised 2009 budget incorporating this decision. The budget was completed by noon, and Richardson found herself a bit bemused by the results. Having finished her duties, she left for an early weekend getaway. She didn't give the budget another thought. Early in January 2010, Richardson prepared a rough draft of the actual 2009 financial results (Exhibit 3); happily, they were better than had been expected. Prices on each grill were as planned, and volume was as shown in Table 1. Table 1. Actual 2009 volumes. Volume (number of units) Grill A B @ 115.000 110.000 225.000 Richardson began to wonder if the bottom line was as high as it should have been. Exhibit 1 BW MANUFACTURING COMPANY Operating Budget 2009: Draft 12/18/2008 ON Sales Less: costs of products sold Gross margin SG&A y costs Operating income Less: Interest expense Plus: Interest income Income before tax Income taxes Net income $41.200,000 22,800,000 $18,400,000 9.350.000 2.100.000 $6.950,000 420,000 150,000 $6,680.000 2.338.000 $4.342.000 Source: Created by case writer. Exhibit 2 BW MANUFACTURING COMPANY Standard Costs Grill A Grill B Grill C Notes Planned Volume (units) 80,000 120,000 200,000 $150 $110 $80 17 21 $38 10 16 $26 7 4 $11 directly related to production volume directly related to production volume Per unit: Sales price Direct costs: Materials Labor Subtotal Indirect costs: Supplies Labor Supervision Energy Depreciation Head office support All other Subtotal Total product cost Product-line profitability 7 10 Bolo Nomor |2014... Talele | 12 22 12 11 $82 $120 $30 2 8 3 6 7 6 2 $34 $60 $50 directly related to production volume one-half varies with direct labor; the rest is fixed unrelated to production volume one-half varies with direct labor, the rest is fixed unrelated to production volume corporate office allocation* unrelated to production volume Exhibit 3 BW MANUFACTURING COMPANY 2009 Operating Results: Draft 1/19/2010 Revenue $46,225,000 4,800,000 5,200,000 1,300,000 1.500.000 1.600.000 $14.400.000 Variable costs: Materials Direct labor Supplies Indirect labor Energy Total variable cost Fixed costs: Indirect labor Supervision Energy Depreciation Hlead office All other Total fixed cost Total cost Gross margin SG&A Other costs Operating income Less: interest expense Plus, interest income Income before tax Income taxes Net income 1.300.000 1.200.000 1.350.000 3.660.000 2.300.000 1.380.000 S11.190.000 $25,590.000 $20,635,000 9.350.000 2,100,000 $9,185.000 420.000 150.000 $8,915,000 3,120.250 $5,794.750 Source: Created by case writerStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Fraud Prevention And Detection

Authors: Joseph T. Wells

5th Edition

1119351987, 9781119351986