Answered step by step

Verified Expert Solution

Question

1 Approved Answer

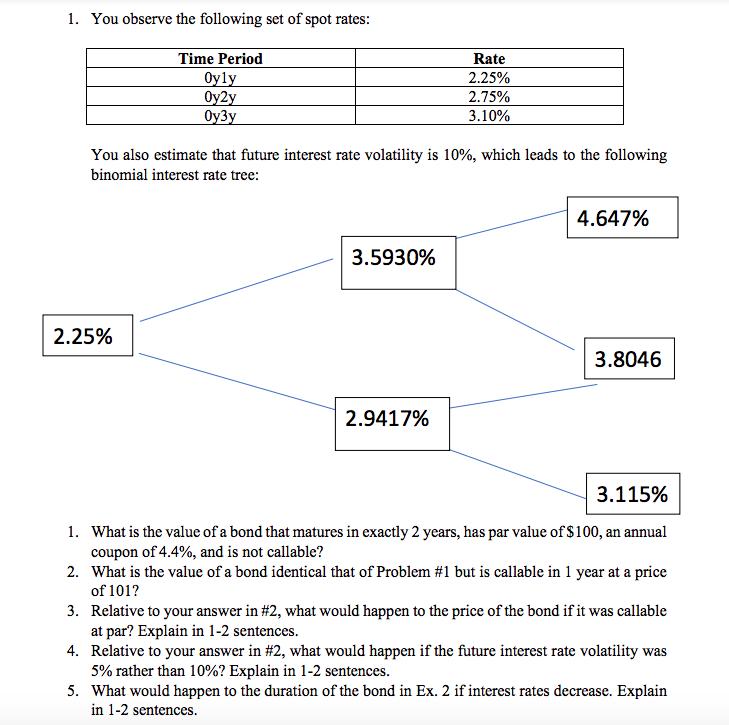

1. You observe the following set of spot rates: Time Period Rate Oyly Oy2y Oy3y 2.25% 2.75% 3.10% You also estimate that future interest

1. You observe the following set of spot rates: Time Period Rate Oyly Oy2y Oy3y 2.25% 2.75% 3.10% You also estimate that future interest rate volatility is 10%, which leads to the following binomial interest rate tree: 4.647% 3.5930% 2.25% 3.8046 2.9417% 3.115% 1. What is the value of a bond that matures in exactly 2 years, has par value of $100, an annual coupon of 4.4%, and is not callable? 2. What is the value of a bond identical that of Problem #1 but is callable in 1 year at a price of 101? 3. Relative to your answer in #2, what would happen to the price of the bond if it was callable at par? Explain in 1-2 sentences. 4. Relative to your answer in #2, what would happen if the future interest rate volatility was 5% rather than 10%? Explain in 1-2 sentences. 5. What would happen to the duration of the bond in Ex. 2 if interest rates decrease. Explain in 1-2 sentences.

Step by Step Solution

★★★★★

3.41 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

1 Value of a bond that matures in exactly 2 years has par value of 100 an annual coupon of 44 a...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Research Methods

Authors: Donald R. Cooper, Pamela S. Schindler

12th edition

9780077774431, 0073521507, 77774434, 978-0073521503