Answered step by step

Verified Expert Solution

Question

1 Approved Answer

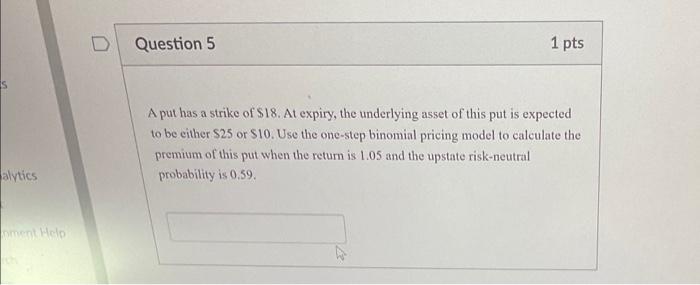

alytics nment Help Question 5 1 pts A put has a strike of $18. At expiry, the underlying asset of this put is expected

alytics nment Help Question 5 1 pts A put has a strike of $18. At expiry, the underlying asset of this put is expected to be either $25 or $10. Use the one-step binomial pricing model to calculate the premium of this put when the return is 1.05 and the upstate risk-neutral probability is 0.59.

Step by Step Solution

★★★★★

3.35 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

Return is 105 Riskneutral probability is 059 and Strike Price ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics The Exploration & Analysis Of Data

Authors: Roxy Peck, Jay L. Devore

7th Edition

0840058012, 978-0840058010