Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Crystal Ltd. is a subsidiary of Crystal Group, a large manufacturer of glass products headquartered in Europe. Although initially established as an industrial-glass producer,

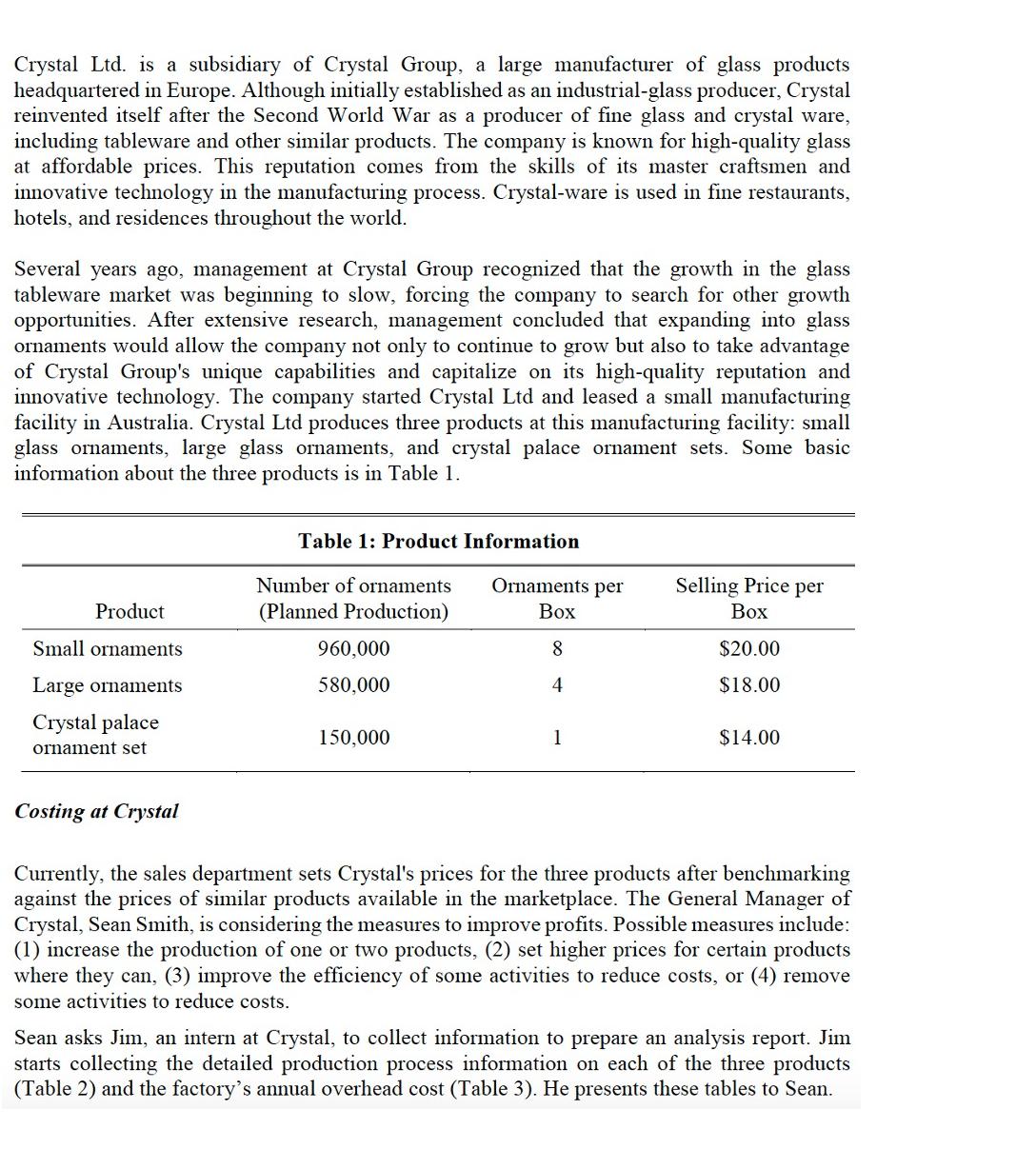

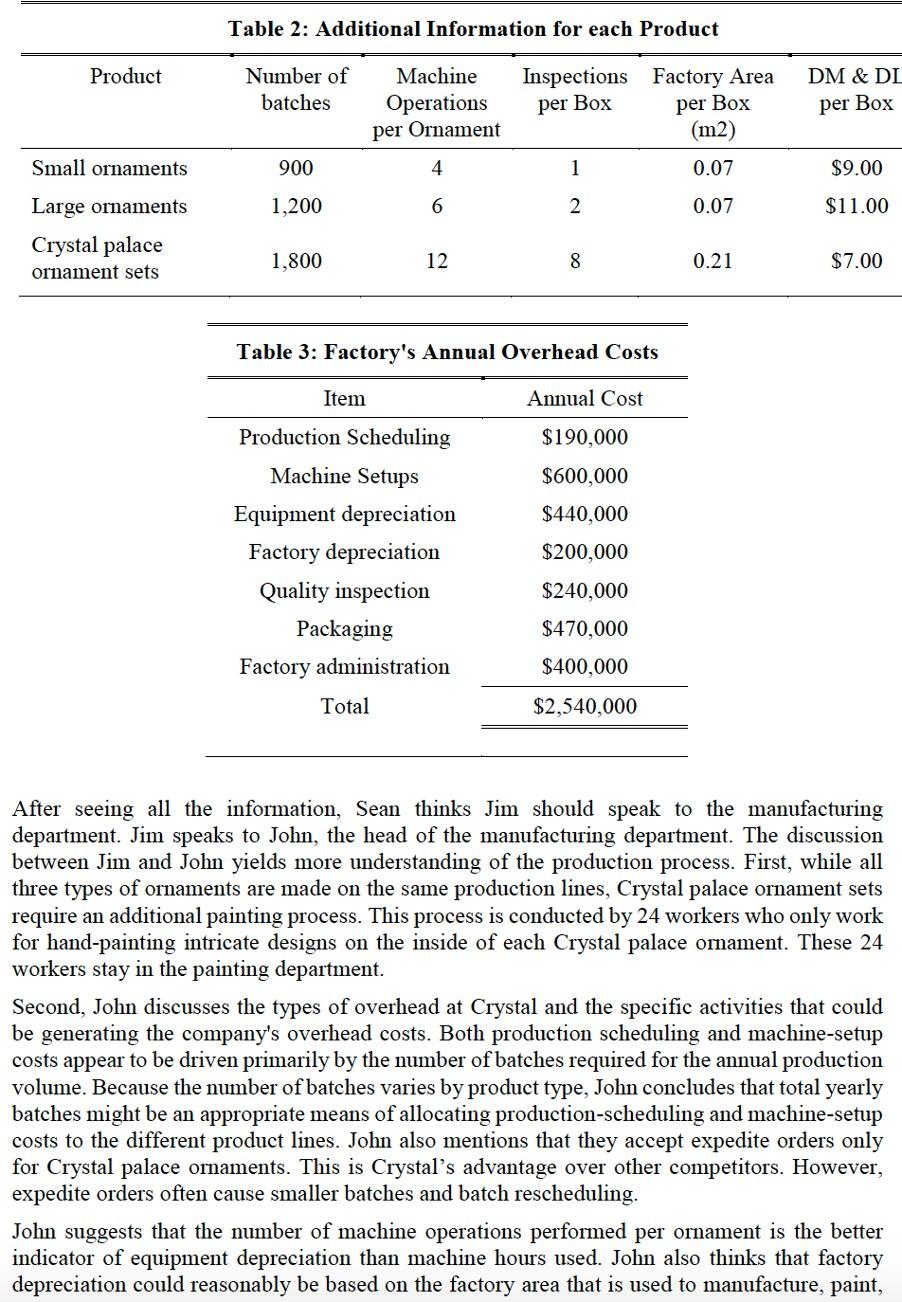

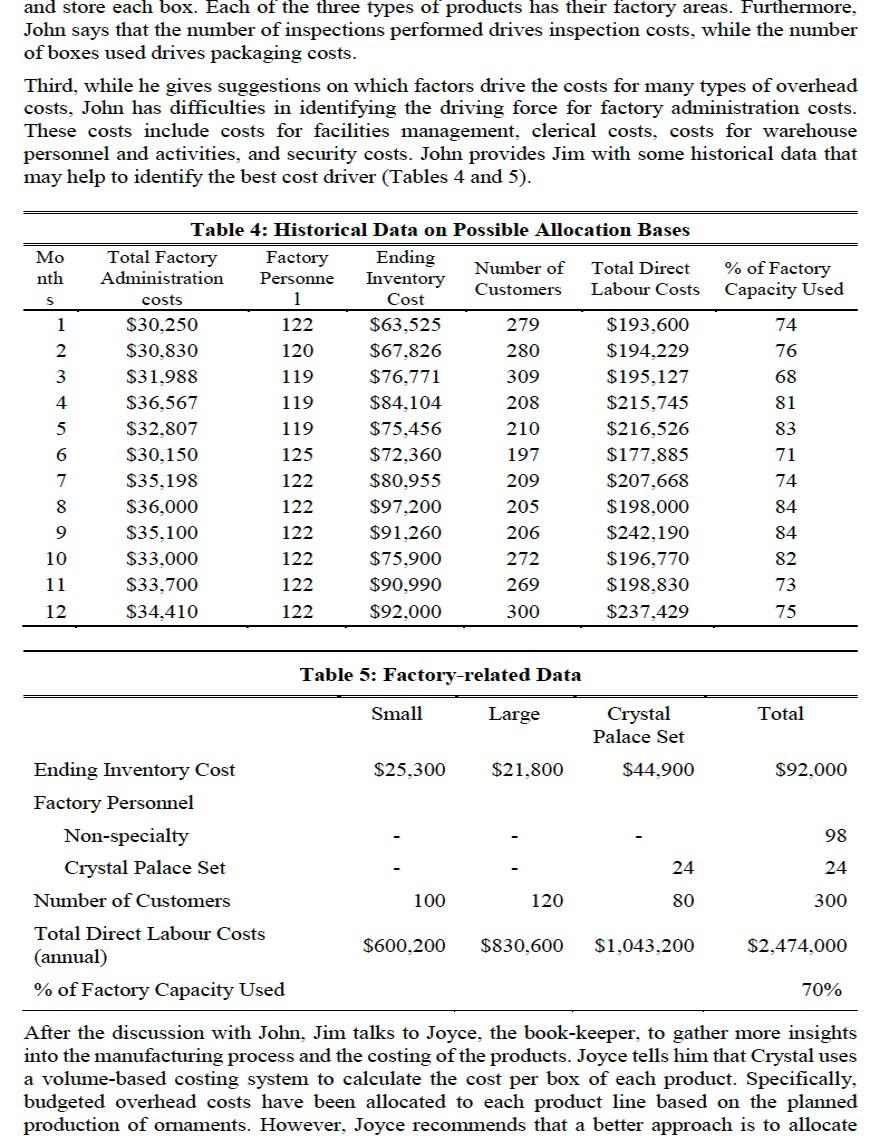

Crystal Ltd. is a subsidiary of Crystal Group, a large manufacturer of glass products headquartered in Europe. Although initially established as an industrial-glass producer, Crystal reinvented itself after the Second World War as a producer of fine glass and crystal ware, including tableware and other similar products. The company is known for high-quality glass at affordable prices. This reputation comes from the skills of its master craftsmen and innovative technology in the manufacturing process. Crystal-ware is used in fine restaurants, hotels, and residences throughout the world. Several years ago, management at Crystal Group recognized that the growth in the glass tableware market was beginning to slow, forcing the company to search for other growth opportunities. After extensive research, management concluded that expanding into glass ornaments would allow the company not only to continue to grow but also to take advantage of Crystal Group's unique capabilities and capitalize on its high-quality reputation and innovative technology. The company started Crystal Ltd and leased a small manufacturing facility in Australia. Crystal Ltd produces three products at this manufacturing facility: small glass ornaments, large glass ornaments, and crystal palace ornament sets. Some basic information about the three products is in Table 1. Product Small ornaments Large ornaments Crystal palace ornament set Costing at Crystal Table 1: Product Information Number of ornaments (Planned Production) 960,000 580,000 150,000 Ornaments per Box 8 4 1 Selling Price per Box $20.00 $18.00 $14.00 Currently, the sales department sets Crystal's prices for the three products after benchmarking against the prices of similar products available in the marketplace. The General Manager of Crystal, Sean Smith, is considering the measures to improve profits. Possible measures include: (1) increase the production of one or two products, (2) set higher prices for certain products where they can, (3) improve the efficiency of some activities to reduce costs, or (4) remove some activities to reduce costs. Sean asks Jim, an intern at Crystal, to collect information to prepare an analysis report. Jim starts collecting the detailed production process information on each of the three products (Table 2) and the factory's annual overhead cost (Table 3). He presents these tables to Sean. Product Small ornaments Large ornaments Crystal palace ornament sets Table 2: Additional Information for each Product Number of batches 900 1,200 1,800 Machine Inspections Operations per Box per Ornament Item 4 6 12 Total Production Scheduling Machine Setups Equipment depreciation Factory depreciation Quality inspection Packaging Factory administration 1 2 Table 3: Factory's Annual Overhead Costs Annual Cost $190,000 $600,000 $440,000 $200,000 $240,000 $470,000 $400,000 $2,540,000 8 Factory Area per Box (m2) 0.07 0.07 0.21 DM & DL per Box $9.00 $11.00 $7.00 After seeing all the information, Sean thinks Jim should speak to the manufacturing department. Jim speaks to John, the head of the manufacturing department. The discussion between Jim and John yields more understanding of the production process. First, while all three types of ornaments are made on the same production lines, Crystal palace ornament sets require an additional painting process. This process is conducted by 24 workers who only work for hand-painting intricate designs on the inside of each Crystal palace ornament. These 24 workers stay in the painting department. Second, John discusses the types of overhead at Crystal and the specific activities that could be generating the company's overhead costs. Both production scheduling and machine-setup costs appear to be driven primarily by the number of batches required for the annual production volume. Because the number of batches varies by product type, John concludes that total yearly batches might be an appropriate means of allocating production-scheduling and machine-setup costs to the different product lines. John also mentions that they accept expedite orders only for Crystal palace ornaments. This is Crystal's advantage over other competitors. However, expedite orders often cause smaller batches and batch rescheduling. John suggests that the number of machine operations performed per ornament is the better indicator of equipment depreciation than machine hours used. John also thinks that factory depreciation could reasonably be based on the factory area that is used to manufacture, paint, and store each box. Each of the three types of products has their factory areas. Furthermore, John says that the number of inspections performed drives inspection costs, while the number of boxes used drives packaging costs. Third, while he gives suggestions on which factors drive the costs for many types of overhead costs, John has difficulties in identifying the driving force for factory administration costs. These costs include costs for facilities management, clerical costs, costs for warehouse personnel and activities, and security costs. John provides Jim with some historical data that may help to identify the best cost driver (Tables 4 and 5). Mo nth S 1 2 3 4 5 6 7 8 9 10 11 12 Table 4: Historical Data on Possible Allocation Bases Ending Inventory Cost $63,525 $67,826 $76,771 $84,104 $75,456 $72,360 $80,955 $97.200 $91,260 $75.900 $90,990 $92,000 Total Factory Administration costs $30,250 $30,830 $31,988 $36,567 $32,807 $30,150 $35,198 $36,000 $35,100 $33.000 $33,700 $34,410 Factory Personne 1 122 120 119 119 119 125 122 122 122 122 122 122 Ending Inventory Cost Factory Personnel Non-specialty Crystal Palace Set Number of Customers Total Direct Labour Costs (annual) % of Factory Capacity Used Small $25,300 Number of Customers 100 279 280 309 Table 5: Factory-related Data 208 210 197 209 205 206 272 269 300 Large $21,800 120 $600,200 $830,600 Total Direct Labour Costs $193,600 $194,229 $195,127 $215.745 $216,526 $177,885 $207,668 $198.000 $242,190 $196,770 $198,830 $237,429 Crystal Palace Set $44.900 24 80 $1,043,200 % of Factory Capacity Used 74 76 68 81 83 71 74 84 84 82 73 75 Total $92,000 98 24 300 $2,474,000 70% After the discussion with John, Jim talks to Joyce, the book-keeper, to gather more insights into the manufacturing process and the costing of the products. Joyce tells him that Crystal uses a volume-based costing system to calculate the cost per box of each product. Specifically, budgeted overhead costs have been allocated to each product line based on the planned production of ornaments. However, Joyce recommends that a better approach is to allocate budgeted overhead costs to each product based upon the total of direct material and direct labor costs. Jim returns to Sean's office with all the information. Sean decides to enlist outside help. Sean recalls playing golf with Axel Baker, the principal of ARA Consultants. After rummaging around to find Axel's business card, he calls him to set up a meeting to discuss Crystal's situation. 3. Discuss what drives the differences in total manufacturing costs and profitability of the three products using three allocation methods. Indicate the best allocation method and explain your reasons. (5 marks) 4. Discuss the possible decisions that Crystal can consider to improve profit. Hints: draw on activity-based management. (10 marks)

Step by Step Solution

★★★★★

3.40 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applying International Financial Reporting Standards

Authors: Keith Alfredson, Ken Leo, Ruth Picker, Paul Pacter, Jennie Radford Victoria Wise

3rd edition

730302121, 978-0730302124