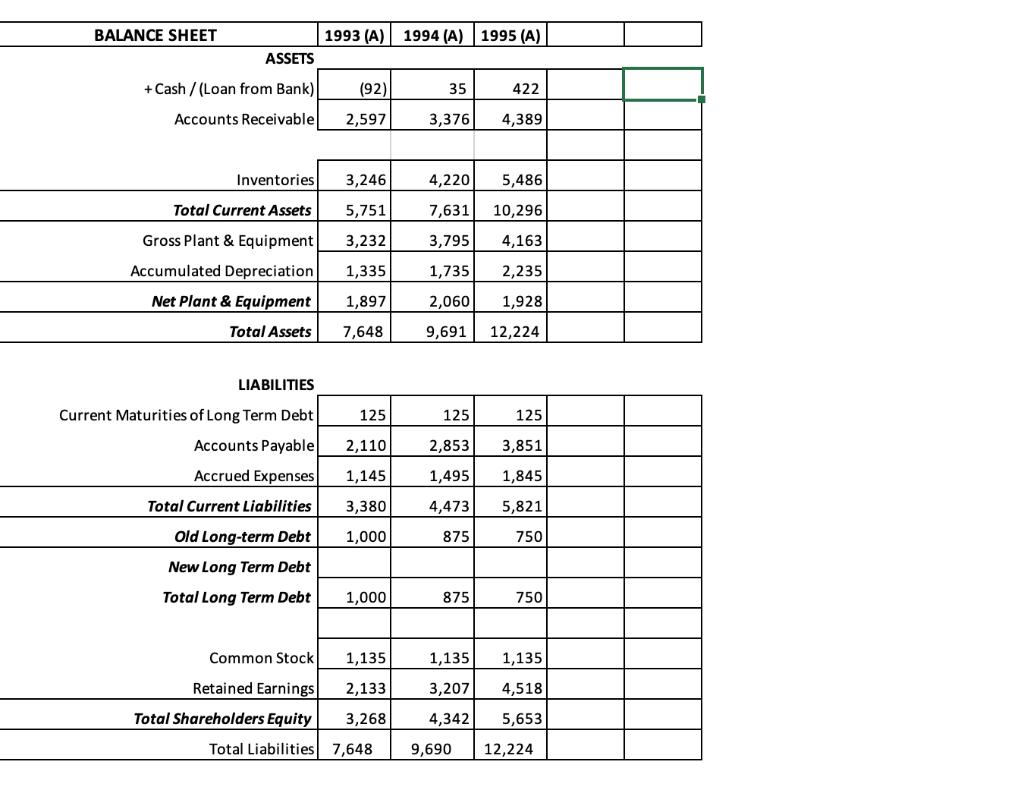

Tire City Inc. Mr. Abdullah, Chief Financial Officer (CFO) of Tire City Inc ('TCI') has a meeting with their bank later in the week.

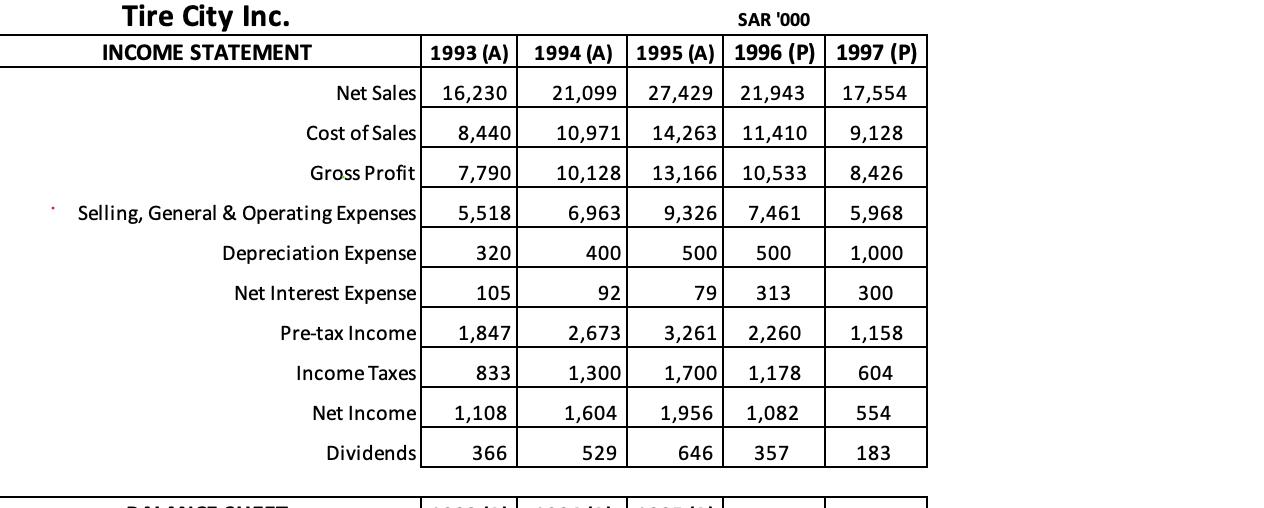

Tire City Inc. Mr. Abdullah, Chief Financial Officer (CFO) of Tire City Inc ('TCI') has a meeting with their bank later in the week. At the meeting he needs to present a request to the bank for funding requirement(s) for a Long Term Loan facility to finance expected growth of the company. The historical financial statements of the company collected by Mr. Abdullah are attached herewith in the Excel file; Company's Background Tire City is a rapidly growing retailer of automobile tires in Saudi Arabia. TCI sells tires through 15 locations throughout Saudi Arabia. All these stores keep sufficient inventory on hand to service immediate customer requirements, but the bulk of TCI's inventories is kept at a central warehouse in Kharj just outside of Riyadh. Each store can be serviced by this warehouse which could fill their extra orders within 24 hours Sales have been growing for the last several years due to the excellent service level and customer satisfaction but after work on expansion of the warehouse was initiated sales estimates were revised due to the changing macroeconomic conditions and discovery of a viral disease globally after which sales are expected to decrease by 20% each year from the previous year's levels in 1996 and 1997. Mr. Abdullah is confident that this drop in sales is a short-term phenomenon and sales will jump back to previous levels and TCI is pushing forward with the warehouse expansion Past Relationship with Amana Bank In 1991 TCI borrowed funds from Amana Bank to build the Kharj warehouse. This loan was being repaid in equal annual installments. At the end of 1997 the balance outstanding was SAR750,000. Another line of credit for working capital requirements of TCI was also established in 1991 but it had not been utilized to date Current Financing Requirement TCI is now contemplating expanding the warehouse in Kharj to accommodate future growth of the company by expanding the warehouse at a cost of SAR5M (CAPEX), of which SAR2.5M will be spent in 1996 and remaining in 1997 (TCI has no other capital expenditure plans for these two years). The expanded warehouse will fulfill the company's storage requirements for many years to come and will have a useful life of 10 years and depreciated using the straight-line method. The construction of the warehouse is projected to be completed in early 1997. TCI would not charge any depreciation on the warehouse during the construction phase in 1996. (You can assume that the SAR value of depreciation of other assets will continue to be the same as 1995 in 1996, 1997 and 1998) Page 2 The warehouse expansion has been planned in such a way that it will have very little disruptive effect on operations of the company. However due to the ongoing construction work, inventories would have to be reduced to 10% of sales by the end of 1996 to make room for construction equipment and materials which will be stored on the same site. The % level of inventories to sales would revert to 1995 level as soon as the warehouse construction is completed in early 1997. TCI's operations would not be affected in any other way due to the ongoing expansion; Operating Profit Margin will remain in line with the historical trends. Current Accounts (except for inventories) will maintain the same steady relationship with sales. Cash Balances / Overdraft or Short Term Loan required from Bank is one item that Mr. Abdullah is concerned about and has asked his staff to determine what will be the ending levels in 1996 and 1997 TCI's corporate tax rate is 35% but after adding miscellaneous local taxes the effective TCI had been historically higher and the same trend was expected to average tax rate continue. TCI is expected to maintain dividend payout ratio to make sure that the stock price of the company was unaffected during the construction phase. In preliminary discussion with Amana Bank about modus operandi of how they can borrow money to finance the expansion project the bank agreed that TCI can borrow money in two separate installments on an as-needed basis, one in 1996 and the other in 1997. The loan would be repayable in 5 equal annual installments, with first installment becoming due after the completion of the warehouse (in 1998). The interest rate offered is 10% p.a. Tire City Inc. SAR '000 INCOME STATEMENT 1993 (A) 1994 (A) 1995 (A) 1996 (P) 1997 (P) Net Sales 16,230 21,099 27,429 21,943 17,554 Cost of Sales 8,440 10,971 14,263 11,410 9,128 Gross Profit 7,790 10,128 13,166 10,533 8,426 Selling, General & Operating Expenses 5,518 6,963 9,326 7,461 5,968 Depreciation Expense 320 400 500 500 1,000 Net Interest Expense 105 92 79 313 300 Pre-tax Income 1,847 2,673 3,261 2,260 1,158 Income Taxes 833 1,300 1,700 1,178 604 Net Income 1,108 1,604 1,956 1,082 554 Dividends 366 529 646 357 183 BALANCE SHEET 1993 (A) 1994 (A) 1995 (A). ASSETS + Cash / (Loan from Bank) (92) 35 422 Accounts Receivable 2,597 3,376 4,389 Inventories 3,246 4,220 5,486 Total Current Assets 5,751 7,631 10,296 Gross Plant & Equipment 3,232 3,795 4,163 Accumulated Depreciation 1,335 1,735 2,235 Net Plant & Equipment 1,897 2,060 1,928 Total Assets 7,648 9,691 12,224 LIABILITIES Current Maturities of Long Term Debt 125 125 125 Accounts Payable 2,110 2,853 3,851 Accrued Expenses 1,145 1,495 1,845 Total Current Liabilities 3,380 4,473 5,821 Old Long-term Debt 1,000 875 750 New Long Term Debt Total Long Term Debt 1,000 875 750 Common Stock 1,135 1,135 1,135 Retained Earnings 2,133 3,207 4,518 Total Shareholders Equity 3,268 4,342 5,653 Total Liabilities 7,648 9,690 12,224 Tire City Inc. Mr. Abdullah, Chief Financial Officer (CFO) of Tire City Inc ('TCI') has a meeting with their bank later in the week. At the meeting he needs to present a request to the bank for funding requirement(s) for a Long Term Loan facility to finance expected growth of the company. The historical financial statements of the company collected by Mr. Abdullah are attached herewith in the Excel file; Company's Background Tire City is a rapidly growing retailer of automobile tires in Saudi Arabia. TCI sells tires through 15 locations throughout Saudi Arabia. All these stores keep sufficient inventory on hand to service immediate customer requirements, but the bulk of TCI's inventories is kept at a central warehouse in Kharj just outside of Riyadh. Each store can be serviced by this warehouse which could fill their extra orders within 24 hours Sales have been growing for the last several years due to the excellent service level and customer satisfaction but after work on expansion of the warehouse was initiated sales estimates were revised due to the changing macroeconomic conditions and discovery of a viral disease globally after which sales are expected to decrease by 20% each year from the previous year's levels in 1996 and 1997. Mr. Abdullah is confident that this drop in sales is a short-term phenomenon and sales will jump back to previous levels and TCI is pushing forward with the warehouse expansion Past Relationship with Amana Bank In 1991 TCI borrowed funds from Amana Bank to build the Kharj warehouse. This loan was being repaid in equal annual installments. At the end of 1997 the balance outstanding was SAR750,000. Another line of credit for working capital requirements of TCI was also established in 1991 but it had not been utilized to date Current Financing Requirement TCI is now contemplating expanding the warehouse in Kharj to accommodate future growth of the company by expanding the warehouse at a cost of SAR5M (CAPEX), of which SAR2.5M will be spent in 1996 and remaining in 1997 (TCI has no other capital expenditure plans for these two years). The expanded warehouse will fulfill the company's storage requirements for many years to come and will have a useful life of 10 years and depreciated using the straight-line method. The construction of the warehouse is projected to be completed in early 1997. TCI would not charge any depreciation on the warehouse during the construction phase in 1996. (You can assume that the SAR value of depreciation of other assets will continue to be the same as 1995 in 1996, 1997 and 1998) Page 2 The warehouse expansion has been planned in such a way that it will have very little disruptive effect on operations of the company. However due to the ongoing construction work, inventories would have to be reduced to 10% of sales by the end of 1996 to make room for construction equipment and materials which will be stored on the same site. The % level of inventories to sales would revert to 1995 level as soon as the warehouse construction is completed in early 1997. TCI's operations would not be affected in any other way due to the ongoing expansion; Operating Profit Margin will remain in line with the historical trends. Current Accounts (except for inventories) will maintain the same steady relationship with sales. Cash Balances / Overdraft or Short Term Loan required from Bank is one item that Mr. Abdullah is concerned about and has asked his staff to determine what will be the ending levels in 1996 and 1997 TCI's corporate tax rate is 35% but after adding miscellaneous local taxes the effective TCI had been historically higher and the same trend was expected to average tax rate continue. TCI is expected to maintain dividend payout ratio to make sure that the stock price of the company was unaffected during the construction phase. In preliminary discussion with Amana Bank about modus operandi of how they can borrow money to finance the expansion project the bank agreed that TCI can borrow money in two separate installments on an as-needed basis, one in 1996 and the other in 1997. The loan would be repayable in 5 equal annual installments, with first installment becoming due after the completion of the warehouse (in 1998). The interest rate offered is 10% p.a. Tire City Inc. SAR '000 INCOME STATEMENT 1993 (A) 1994 (A) 1995 (A) 1996 (P) 1997 (P) Net Sales 16,230 21,099 27,429 21,943 17,554 Cost of Sales 8,440 10,971 14,263 11,410 9,128 Gross Profit 7,790 10,128 13,166 10,533 8,426 Selling, General & Operating Expenses 5,518 6,963 9,326 7,461 5,968 Depreciation Expense 320 400 500 500 1,000 Net Interest Expense 105 92 79 313 300 Pre-tax Income 1,847 2,673 3,261 2,260 1,158 Income Taxes 833 1,300 1,700 1,178 604 Net Income 1,108 1,604 1,956 1,082 554 Dividends 366 529 646 357 183 BALANCE SHEET 1993 (A) 1994 (A) 1995 (A). ASSETS + Cash / (Loan from Bank) (92) 35 422 Accounts Receivable 2,597 3,376 4,389 Inventories 3,246 4,220 5,486 Total Current Assets 5,751 7,631 10,296 Gross Plant & Equipment 3,232 3,795 4,163 Accumulated Depreciation 1,335 1,735 2,235 Net Plant & Equipment 1,897 2,060 1,928 Total Assets 7,648 9,691 12,224 LIABILITIES Current Maturities of Long Term Debt 125 125 125 Accounts Payable 2,110 2,853 3,851 Accrued Expenses 1,145 1,495 1,845 Total Current Liabilities 3,380 4,473 5,821 Old Long-term Debt 1,000 875 750 New Long Term Debt Total Long Term Debt 1,000 875 750 Common Stock 1,135 1,135 1,135 Retained Earnings 2,133 3,207 4,518 Total Shareholders Equity 3,268 4,342 5,653 Total Liabilities 7,648 9,690 12,224 Tire City Inc. Mr. Abdullah, Chief Financial Officer (CFO) of Tire City Inc ('TCI') has a meeting with their bank later in the week. At the meeting he needs to present a request to the bank for funding requirement(s) for a Long Term Loan facility to finance expected growth of the company. The historical financial statements of the company collected by Mr. Abdullah are attached herewith in the Excel file; Company's Background Tire City is a rapidly growing retailer of automobile tires in Saudi Arabia. TCI sells tires through 15 locations throughout Saudi Arabia. All these stores keep sufficient inventory on hand to service immediate customer requirements, but the bulk of TCI's inventories is kept at a central warehouse in Kharj just outside of Riyadh. Each store can be serviced by this warehouse which could fill their extra orders within 24 hours Sales have been growing for the last several years due to the excellent service level and customer satisfaction but after work on expansion of the warehouse was initiated sales estimates were revised due to the changing macroeconomic conditions and discovery of a viral disease globally after which sales are expected to decrease by 20% each year from the previous year's levels in 1996 and 1997. Mr. Abdullah is confident that this drop in sales is a short-term phenomenon and sales will jump back to previous levels and TCI is pushing forward with the warehouse expansion Past Relationship with Amana Bank In 1991 TCI borrowed funds from Amana Bank to build the Kharj warehouse. This loan was being repaid in equal annual installments. At the end of 1997 the balance outstanding was SAR750,000. Another line of credit for working capital requirements of TCI was also established in 1991 but it had not been utilized to date Current Financing Requirement TCI is now contemplating expanding the warehouse in Kharj to accommodate future growth of the company by expanding the warehouse at a cost of SAR5M (CAPEX), of which SAR2.5M will be spent in 1996 and remaining in 1997 (TCI has no other capital expenditure plans for these two years). The expanded warehouse will fulfill the company's storage requirements for many years to come and will have a useful life of 10 years and depreciated using the straight-line method. The construction of the warehouse is projected to be completed in early 1997. TCI would not charge any depreciation on the warehouse during the construction phase in 1996. (You can assume that the SAR value of depreciation of other assets will continue to be the same as 1995 in 1996, 1997 and 1998) Page 2 The warehouse expansion has been planned in such a way that it will have very little disruptive effect on operations of the company. However due to the ongoing construction work, inventories would have to be reduced to 10% of sales by the end of 1996 to make room for construction equipment and materials which will be stored on the same site. The % level of inventories to sales would revert to 1995 level as soon as the warehouse construction is completed in early 1997. TCI's operations would not be affected in any other way due to the ongoing expansion; Operating Profit Margin will remain in line with the historical trends. Current Accounts (except for inventories) will maintain the same steady relationship with sales. Cash Balances / Overdraft or Short Term Loan required from Bank is one item that Mr. Abdullah is concerned about and has asked his staff to determine what will be the ending levels in 1996 and 1997 TCI's corporate tax rate is 35% but after adding miscellaneous local taxes the effective TCI had been historically higher and the same trend was expected to average tax rate continue. TCI is expected to maintain dividend payout ratio to make sure that the stock price of the company was unaffected during the construction phase. In preliminary discussion with Amana Bank about modus operandi of how they can borrow money to finance the expansion project the bank agreed that TCI can borrow money in two separate installments on an as-needed basis, one in 1996 and the other in 1997. The loan would be repayable in 5 equal annual installments, with first installment becoming due after the completion of the warehouse (in 1998). The interest rate offered is 10% p.a. Tire City Inc. SAR '000 INCOME STATEMENT 1993 (A) 1994 (A) 1995 (A) 1996 (P) 1997 (P) Net Sales 16,230 21,099 27,429 21,943 17,554 Cost of Sales 8,440 10,971 14,263 11,410 9,128 Gross Profit 7,790 10,128 13,166 10,533 8,426 Selling, General & Operating Expenses 5,518 6,963 9,326 7,461 5,968 Depreciation Expense 320 400 500 500 1,000 Net Interest Expense 105 92 79 313 300 Pre-tax Income 1,847 2,673 3,261 2,260 1,158 Income Taxes 833 1,300 1,700 1,178 604 Net Income 1,108 1,604 1,956 1,082 554 Dividends 366 529 646 357 183 BALANCE SHEET 1993 (A) 1994 (A) 1995 (A). ASSETS + Cash / (Loan from Bank) (92) 35 422 Accounts Receivable 2,597 3,376 4,389 Inventories 3,246 4,220 5,486 Total Current Assets 5,751 7,631 10,296 Gross Plant & Equipment 3,232 3,795 4,163 Accumulated Depreciation 1,335 1,735 2,235 Net Plant & Equipment 1,897 2,060 1,928 Total Assets 7,648 9,691 12,224 LIABILITIES Current Maturities of Long Term Debt 125 125 125 Accounts Payable 2,110 2,853 3,851 Accrued Expenses 1,145 1,495 1,845 Total Current Liabilities 3,380 4,473 5,821 Old Long-term Debt 1,000 875 750 New Long Term Debt Total Long Term Debt 1,000 875 750 Common Stock 1,135 1,135 1,135 Retained Earnings 2,133 3,207 4,518 Total Shareholders Equity 3,268 4,342 5,653 Total Liabilities 7,648 9,690 12,224

Step by Step Solution

There are 3 Steps involved in it

Step: 1

The Balance Sheet of 1996 and 1997 would be as below Balance Shee...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: J. David Spiceland, Wayne Thomas, Don Herrmann

3rd edition

9780077506902, 78025540, 77506901, 978-0078025549