Answered step by step

Verified Expert Solution

Question

1 Approved Answer

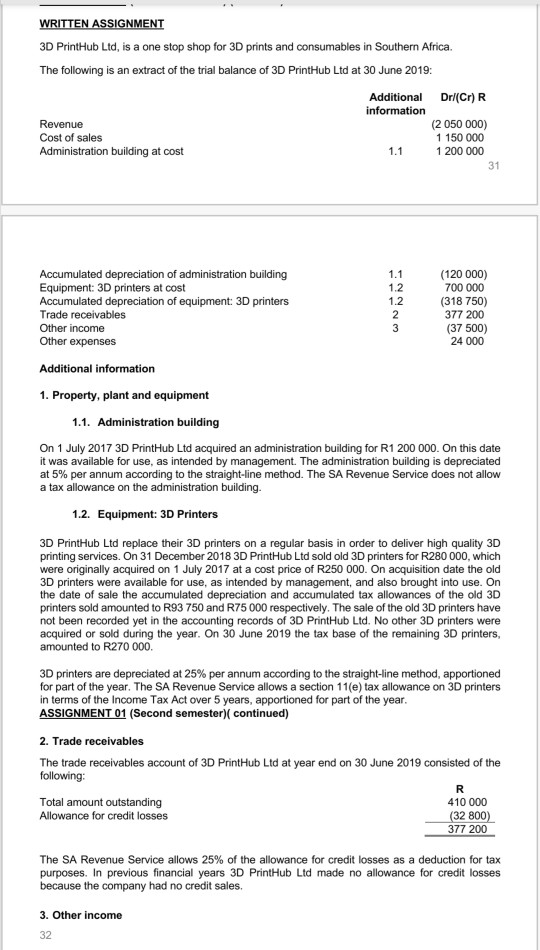

WRITTEN ASSIGNMENT 3D PrintHub Ltd, is a one stop shop for 3D prints and consumables in Southern Africa. The following is an extract of

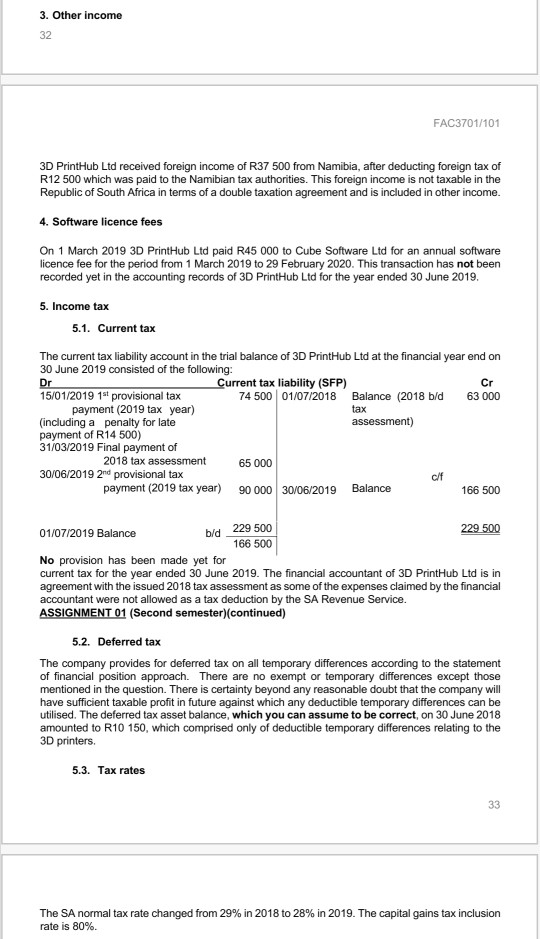

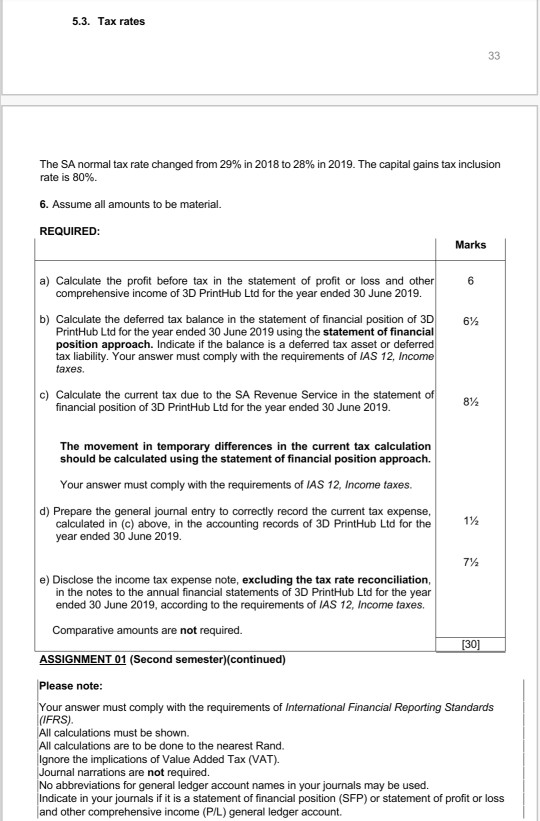

WRITTEN ASSIGNMENT 3D PrintHub Ltd, is a one stop shop for 3D prints and consumables in Southern Africa. The following is an extract of the trial balance of 3D PrintHub Ltd at 30 June 2019: Revenue Cost of sales Administration building at cost Additional information 1.1 Accumulated depreciation of administration building Equipment: 3D printers at cost Accumulated depreciation of equipment: 3D printers Trade receivables Other income Other expenses Additional information 1. Property, plant and equipment 1.1. Administration building On 1 July 2017 3D PrintHub Ltd acquired an administration building for R1 200 000. On this date it was available for use, as intended by management. The administration building is depreciated at 5% per annum according to the straight-line method. The SA Revenue Service does not allow a tax allowance on the administration building. 1.2. Equipment: 3D Printers 1.1 1.2 Total amount outstanding Allowance for credit losses Dr/(Cr) R (2 050 000) 1 150 000 1 200 000 1.2 2 3 3. Other income 32 31 (120 000) 700 000 (318 750) 377 200 (37 500) 24 000 3D PrintHub Ltd replace their 3D printers on a regular basis in order to deliver high quality 3D printing services. On 31 December 2018 3D PrintHub Ltd sold old 3D printers for R280 000, which were originally acquired on 1 July 2017 at a cost price of R250 000. On acquisition date the old 3D printers were available for use, as intended by management, and also brought into use. On the date of sale the accumulated depreciation and accumulated tax allowances of the old 3D printers sold amounted to R93 750 and R75 000 respectively. The sale of the old 3D printers have not been recorded yet in the accounting records of 3D PrintHub Ltd. No other 3D printers were acquired or sold during the year. On 30 June 2019 the tax base of the remaining 3D printers, amounted to R270 000. 3D printers are depreciated at 25% per annum according to the straight-line method, apportioned for part of the year. The SA Revenue Service allows a section 11(e) tax allowance on 3D printers in terms of the Income Tax Act over 5 years, apportioned for part of the year. ASSIGNMENT 01 (Second semester)( continued) 2. Trade receivables The trade receivables account of 3D PrintHub Ltd at year end on 30 June 2019 consisted of the following: R 410 000 (32 800) 377 200 The SA Revenue Service allows 25% of the allowance for credit losses as a deduction for tax purposes. In previous financial years 3D PrintHub Ltd made no allowance for credit losses because the company had no credit sales. 3. Other income 32 3D PrintHub Ltd received foreign income of R37 500 from Namibia, after deducting foreign tax of R12 500 which was paid to the Namibian tax authorities. This foreign income is not taxable in the Republic of South Africa in terms of a double taxation agreement and is included in other income. 4. Software licence fees On 1 March 2019 3D PrintHub Ltd paid R45 000 to Cube Software Ltd for an annual software licence fee for the period from 1 March 2019 to 29 February 2020. This transaction has not been recorded yet in the accounting records of 3D PrintHub Ltd for the year ended 30 June 2019. 5. Income tax 5.1. Current tax The current tax liability account in the trial balance of 3D PrintHub Ltd at the financial year end on 30 June 2019 consisted of the following: Dr 15/01/2019 1st provisional tax payment (2019 tax year) (including a penalty for late payment of R14 500) 31/03/2019 Final payment of Current tax liability (SFP) 74 500 01/07/2018 2018 tax assessment 30/06/2019 2nd provisional tax payment (2019 tax year) 65 000 90 000 30/06/2019 FAC3701/101 229 500 166 500 Balance (2018 b/d tax assessment) Balance c/f Cr 63 000 166 500 229 500 01/07/2019 Balance b/d No provision has been made yet for current tax for the year ended 30 June 2019. The financial accountant of 3D PrintHub Ltd is in agreement with the issued 2018 tax assessment as some of the expenses claimed by the financial accountant were not allowed as a tax deduction by the SA Revenue Service. ASSIGNMENT 01 (Second semester) (continued) 5.2. Deferred tax The company provides for deferred tax on all temporary differences according to the statement of financial position approach. There are no exempt or temporary differences except those mentioned in the question. There is certainty beyond any reasonable doubt that the company will have sufficient taxable profit in future against which any deductible temporary differences can be utilised. The deferred tax asset balance, which you can assume to be correct, on 30 June 2018 amounted to R10 150, which comprised only of deductible temporary differences relating to the 3D printers. 5.3. Tax rates 33 The SA normal tax rate changed from 29% in 2018 to 28% in 2019. The capital gains tax inclusion rate is 80%. 5.3. Tax rates The SA normal tax rate changed from 29% in 2018 to 28% in 2019. The capital gains tax inclusion rate is 80%. 6. Assume all amounts to be material. REQUIRED: a) Calculate the profit before tax in the statement of profit or loss and other comprehensive income of 3D PrintHub Ltd for the year ended 30 June 2019. b) Calculate the deferred tax balance in the statement of financial position of 3D PrintHub Ltd for the year ended 30 June 2019 using the statement of financial position approach. Indicate if the balance is a deferred tax asset or deferred tax liability. Your answer must comply with the requirements of IAS 12, Income taxes. c) Calculate the current tax due to the SA Revenue Service in the statement of financial position of 3D PrintHub Ltd for the year ended 30 June 2019. The movement in temporary differences in the current tax calculation should be calculated using the statement of financial position approach. Your answer must comply with the requirements of IAS 12, Income taxes. d) Prepare the general journal entry to correctly record the current tax expense, calculated in (c) above, in the accounting records of 3D PrintHub Ltd for the year ended 30 June 2019. Marks 6 6 8 1 7 33 e) Disclose the income tax expense note, excluding the tax rate reconciliation, in the notes to the annual financial statements of 3D PrintHub Ltd for the year ended 30 June 2019, according to the requirements of IAS 12, Income taxes. Comparative amounts are not required. ASSIGNMENT 01 (Second semester) (continued) Please note: Your answer must comply with the requirements of International Financial Reporting Standards (IFRS). [30] All calculations must be shown. All calculations are to be done to the nearest Rand. Ignore the implications of Value Added Tax (VAT). Journal narrations are not required. No abbreviations for general ledger account names in your journals may be used. Indicate in your journals if it is a statement of financial position (SFP) or statement of profit or loss and other comprehensive income (P/L) general ledger account.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Working Note Calculation of dep for PPE Administration building co...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting

Authors: Lew Edwards, John Medlin, Keryn Chalmers, Andreas Hellmann, Claire Beattie, Jodie Maxfield, John Hoggett

9th edition

1118608224, 1118608227, 730323994, 9780730323990, 730319172, 9780730319177, 978-1118608227