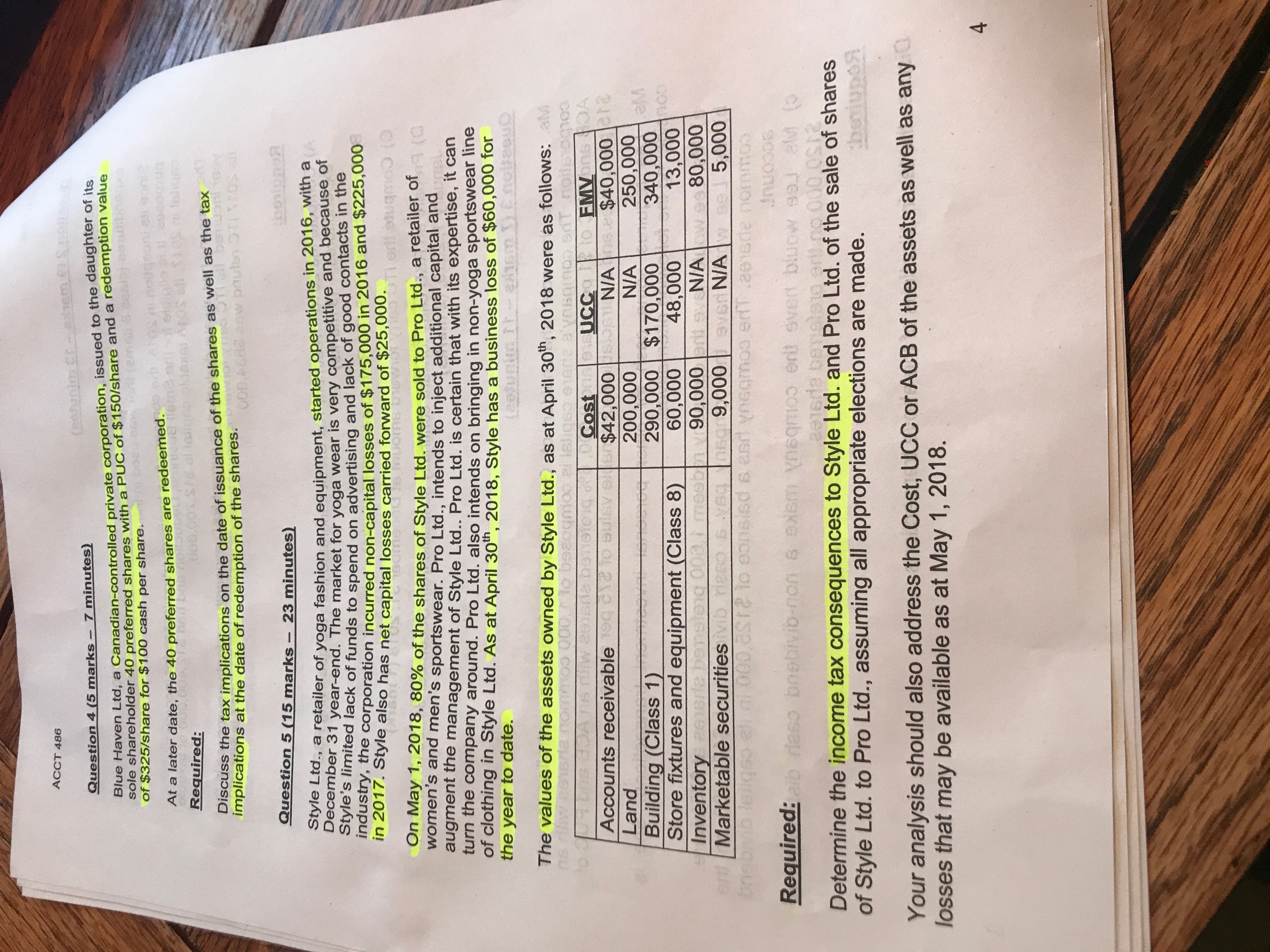

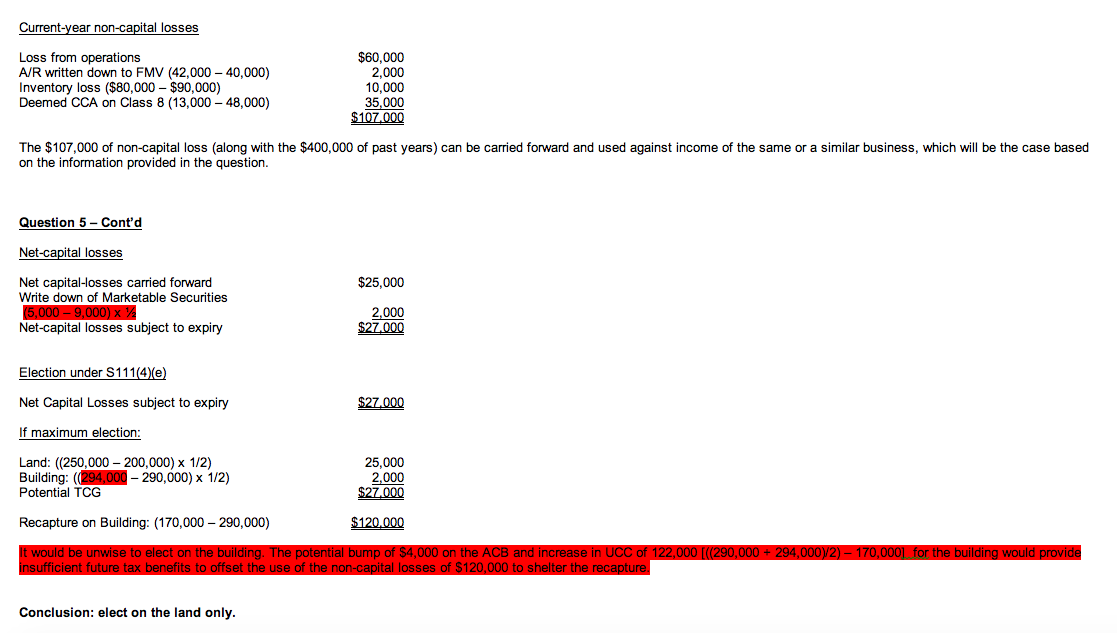

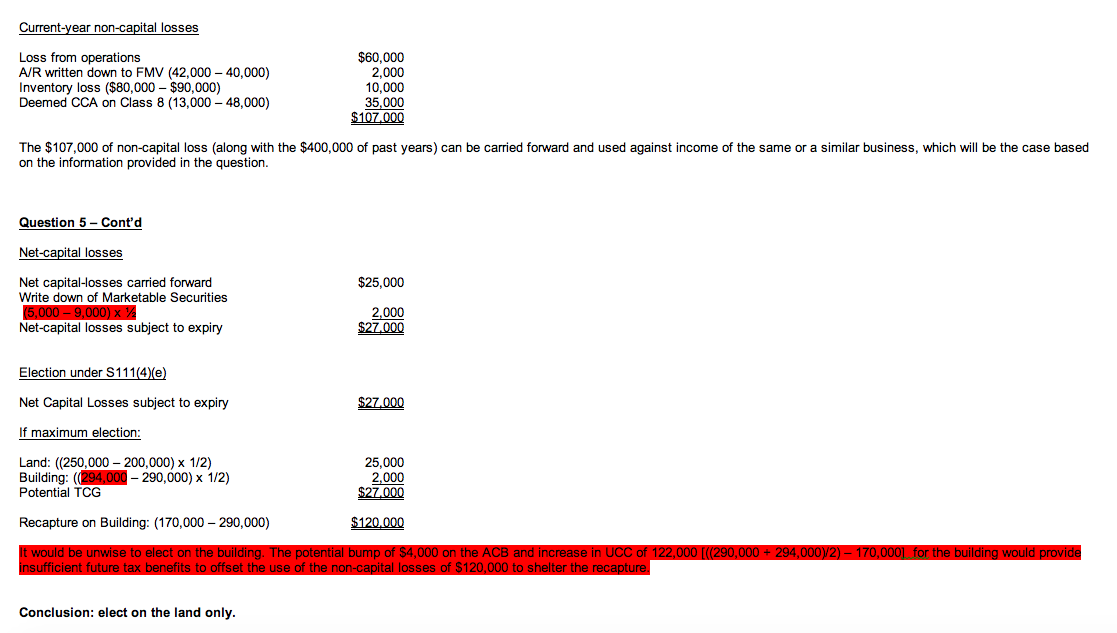

ACCT 486 them O Snow Question 4 (5 marks - 7 minutes) Blue Haven Lid, a Canadian-controlled private corporation, issued to the daughter of its sole shareholder 40 preferred shares with a PUC of $150/share and a redemption value of $325/share for $100 cash per share. At a later date, the 40 preferred shares are redeemed. is ai nollcount est eon Required: Discuss the tax implications on the date of issuance of the shares as well as the tax any implications at the date of redemption of the shares. Question 5 (15 marks - 23 minutes) Style Lid., a retailer of yoga fashion and equipment, started operations in 2016, with a December 31 year-end. The market for yoga wear is very competitive and because of Style's limited lack of funds to spend on advertising and lack of good contacts in the industry, the corporation incurred non-capital losses of $175,000 in 2016 and $225,000 in 2017. Style also has net capital losses carried forward of $25,000. slugmoo (0 On May 1, 2018, 80% of the shares of Style Lid. were sold to Pro Lid., a retailer of women's and men's sportswear. Pro Lid., intends to inject additional capital and augment the management of Style Ltd.. Pro Ltd. is certain that with its expertise, it can turn the company around. Pro Ltd. also intends on bringing in non-yoga sportswear line the year to date. of clothing in Style Lid. As at April 30th, 2018, Style has a business loss of $60,000 for The values of the assets owned by Style Lid., as at April 30", 2018 were as follows: aM 100 Cost FMV DA Accounts receivable UCC Land $42,000 N/A $40,000 Building (Class 1) 200,000 N/A 250,000 We Store fixtures and equipment (Class 8) 290,000 $170,000 340,000 60,000 48,000 Inventory 13,000 160 90,000 Marketable securities N/A 80,000 9,000 N/A 5,000 aste lo eonsled s and ynegmoo eff aisle nommod Required: a less boshiviberon & exem vneqmoo ent svert blow sol al to JnuoooB Determine the income tax consequences to Style Lid. and Pro Lid. of the sale of shares of Style Lid. to Pro Ltd., assuming all appropriate elections are made. Your analysis should also address the Cost, UCC or ACB of the assets as well as any losses that may be available as at May 1, 2018. 4Currentyear mncapital losses Loss from operations $60,000 NR written down to FMV {42,000 40,000) 2,000 Inventory loss {$00,000 $90,000) 10,000 Deemed CCA on Class 8 {13,000 43,000) 35,000 m The $107,000 of mncapital loss {along with the $400,000 of past years) can be carried forward and used against income of the same or a similar business, which will be the case based on the information provided in the question. Question 5 Cont'd Netapital losses Net capitallosses carried forward $25,000 Write down of Marketable Securities 2.000 Netcapital losses subject to expiry m Election under Si'l'lHe] Net Capital Losses subject to expiry m If maximum election: Land: \"250.000 200,000) x 1:2) 25.000 Building: {_ 290,000) x 1:2) 2,000 Potential Tcs m Recapture on Building: {170.000 290.000) M Conclusion: elect. on the land only