Answered step by step

Verified Expert Solution

Question

1 Approved Answer

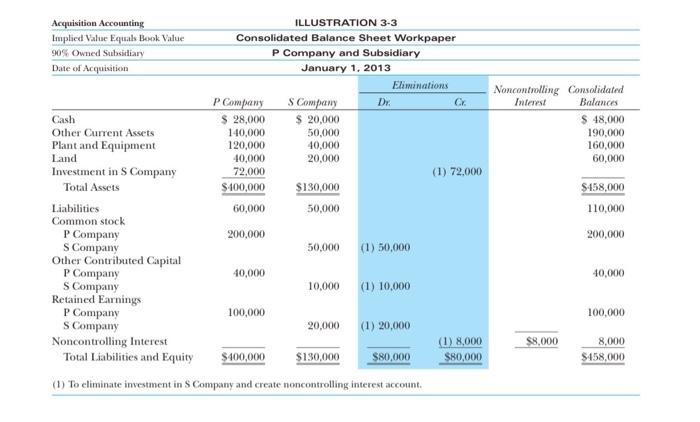

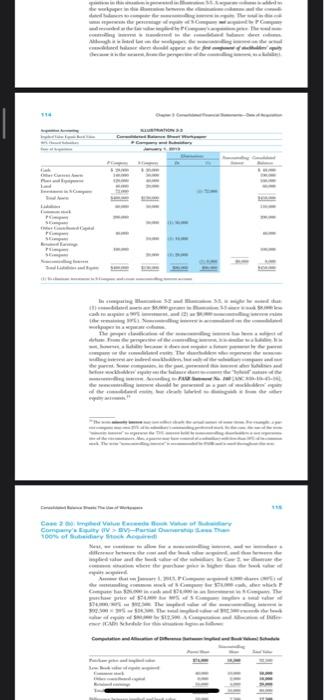

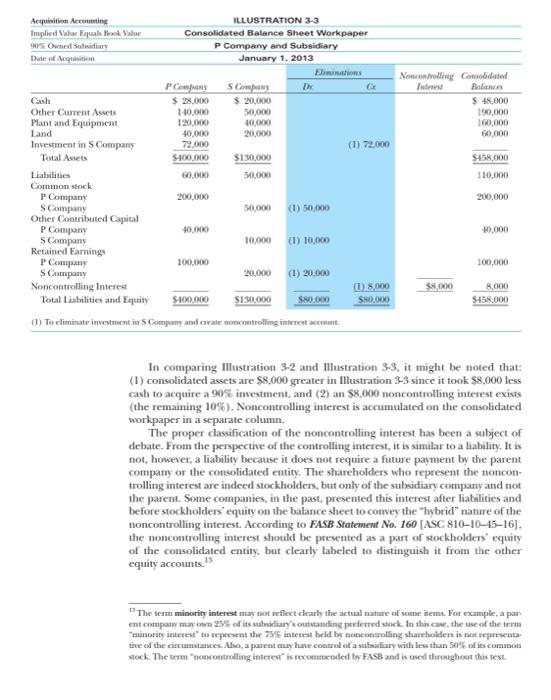

Acquisition Accounting Implied Value Equals Book Value 90% Owned Subsidiary Date of Acquisition ILLUSTRATION 3-3 Consolidated Balance Sheet Workpaper P Company and Subsidiary January 1,

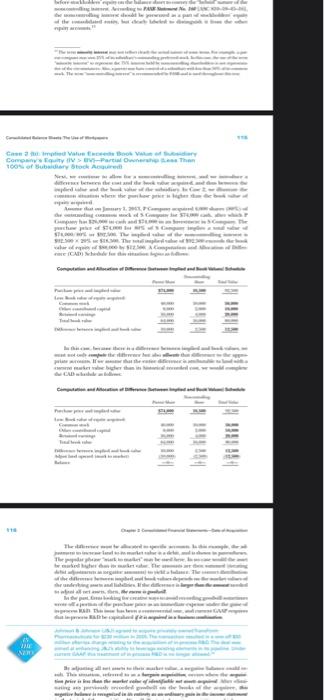

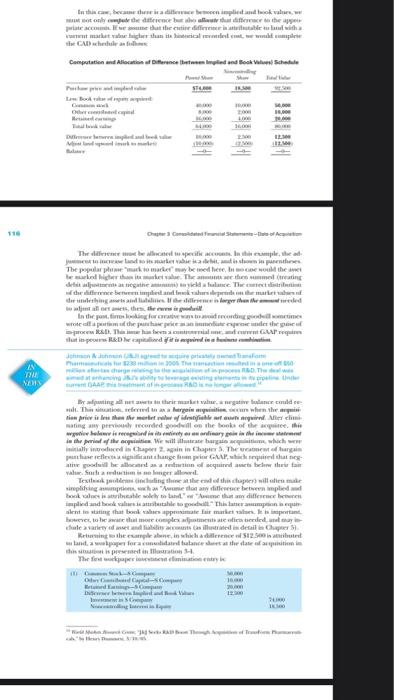

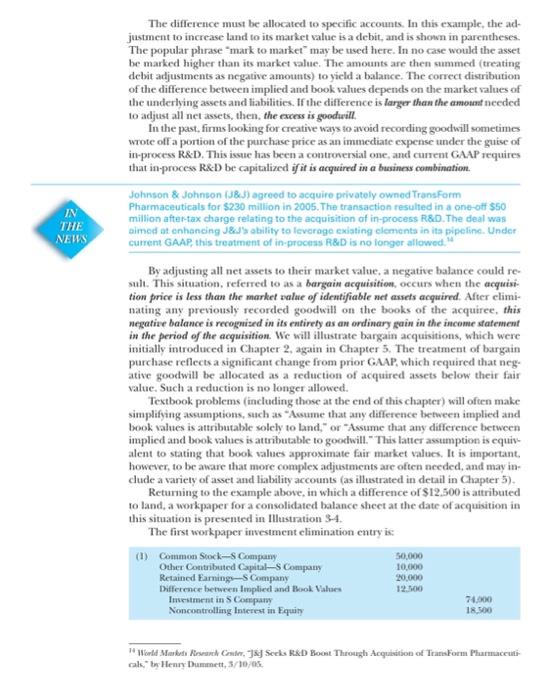

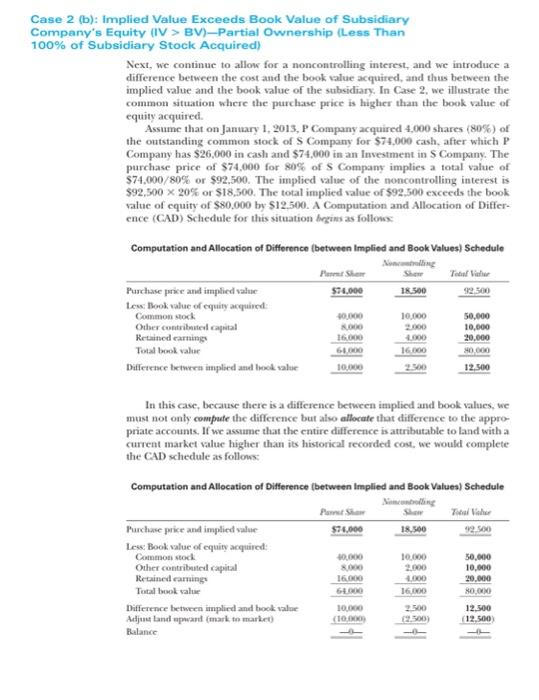

Acquisition Accounting Implied Value Equals Book Value 90% Owned Subsidiary Date of Acquisition ILLUSTRATION 3-3 Consolidated Balance Sheet Workpaper P Company and Subsidiary January 1, 2013 Eliminations P Company S Company Dr. Cr Noncontrolling Consolidated Interest Balances Cash $ 28,000 $ 20,000 $ 48,000 Other Current Assets 140,000 50,000 190,000 Plant and Equipment 120,000 40,000 160,000 Land 40,000 20,000 60,000 Investment in S Company 72,000 (1) 72,000 Total Assets $400,000 $130,000 $458,000 Liabilities 60,000 50,000 110,000 Common stock P Company 200,000 200,000 S Company 50,000 (1) 50,000 Other Contributed Capital P Company 40,000 40,000 S Company 10,000 (1) 10,000 Retained Earnings P Company 100,000 100,000 S Company 20,000 (1) 20,000 Noncontrolling Interest (1) 8,000) $8,000 8,000 Total Liabilities and Equity $400,000 $130,000 $80,000 $80,000 $458,000 (1) To eliminate investment in S Company and create noncontrolling interest account. Case 200 med Values Vale of Company's Equity (VSV-Partial Ownership The 100% of Subsidiary Stock Acquired coon where the a The the da Case 2 Implied Value Exceeds Book Value of Subsidiary Company's Equity > B-Partial Ownership Less Than 100% of Subsidiary Stock Acquired 116 the CAD d The few 116 In this case, because these is a difference been implied and book value must not only compute the difference but aho allocate that difference to the appe priate accoumes. If we assume that the entire difference is attributable to land with a comment market value higher than its historical moded cost, we would comple the CAD schedule as fol Computation and Allocation of Difference between Implied and Book Values Schedule Law Book of The difference be allocated to specific accounts. In this example, the ad justment to increase land so its marker value is a debit, and is shown in parentheses The popular phrase "mack to market may be used here. In one would the ant of the difference between implest and book values depends on the market sales of de underlying assets and labies If the difference is larger than the ded to just all net amets, then, the es i godi In the past, firms looking for crative ways to avoid recording goodwill sometimes wrote all a portion of the purchase price as an immediate expense under the pine of proces R&D). This has been a controversial on and slut in peers R&D be capitalised if it is aired in a h GAAP requires IN THE NOIS GAAP meatment of ingrass R&D is no longer allowed Beating all neat to their market value, a negative balance could re- in situation, referred to as a bargain aquisition occurs when the acquis tion price is less than the market value of identifiable to acquired. After clim nating any previously recorded goodwill on the books of the acquire, this in the period of the acquisition. We will illustrate bargain acquisitions, which were initially introduced in Chapter 2, again in Chapter 3. The weatment of bargain purchase reflects a significant change hom prior GAAP, which required that neg ative goodwill be allocated as a reduction of acquired assets below their fair Such a reduction is no longer allowed Textbook problems including those at the e at the end of this chapter) will aten make simplifying a sch as "Assume that any difference between implied and book does is attributable solely to land" or "me that any difference between implied and book o to goodwill This later asumption is equi alent to stating that book values approximate fair market sales pr however, to be aware that more complex adjustments are often needed, and may chale a variety of asset and B and liability accounts as illustrated in detail in Chapter 3). Returning the example abone, in which a dillerence of $12.500 inatibuted land, a workpaper for a consolidated balance sheet at the date of acquisitionin this situation is presented in Illustration 3-4 The first workpaper is elamination entry i Acquisition Accounting Implied Value Equal Book Value 90% Owned Subsidiary Date of Acquisition ILLUSTRATION 3-3 Consolidated Balance Sheet Workpaper P Company and Subsidiary January 1, 2013 Eliminations PCompany S Company Dr. Noncontrolling Consolidated Interest Balances Cash $ 28,000 $ 20,000 $ 48,000 Other Current Assets 140,000 50,000 190,000 Plant and Equipment 120,000 40,000 160,000 Land 40,000 20,000 60,000 Investment in S Company 72,000 (1) 72,000 Total Assets $400,000 $130,000 $458,000 Liabilities 60,000 50,000 110,000. Common stock. P Company 200,000 200,000 S Company 50,000 (1) 50,000 Other Contributed Capital P Company 40,000 40,000 S Company 10,000 (1) 10,000 Retained Earnings P Company 100,000 100,000 S Company 20,000 (1) 20,000 Noncontrolling Interest (1) 8,000 $8,000 8,000 Total Liabilities and Equity $400,000 $130,000 $80,000 $80,000 $458,000 (1) To eliminate investment in S Company and create noncontrolling interest account. In comparing Illustration 3-2 and Illustration 3-3, it might be noted that: (1) consolidated assets are $8,000 greater in Illustration 3-3 since it took $8,000 less cash to acquire a 90% investment, and (2) an $8,000 noncontrolling interest exists (the remaining 10%). Noncontrolling interest is accumulated on the consolidated workpaper in a separate column. The proper classification of the noncontrolling interest has been a subject of debate. From the perspective of the controlling interest, it is similar to a liability. It is not, however, a liability because it does not require a future payment by the parent company or the consolidated entity. The shareholders who represent the noncon- trolling interest are indeed stockholders, but only of the subsidiary company and not the parent. Some companies, in the past, presented this interest after liabilities and before stockholders' equity on the balance sheet to convey the "hybrid" nature of the noncontrolling interest. According to FASB Statement No. 160 [ASC 810-10-45-16]. the noncontrolling interest should be presented as a part of stockholders' equity of the consolidated entity, but clearly labeled to distinguish it from the other equity accounts. "The term minority interest may not reflect clearly the actual nature of some items. For example, a par- ent company may own 25% of its subsidiary's outstanding preferred stock. In this case, the use of the term "minority interest" to represent the 75% interest held by noncontrolling shareholders is not representa tive of the circumstances. Also, a parent may have control of a subsidiary with less than 50% of its common stock. The term "noncontrolling interest" is recommended by FASB and is used throughout this text. IN THE NEWS The difference must be allocated to specific accounts. In this example, the ad- justment to increase land to its market value is a debit, and is shown in parentheses. The popular phrase "mark to market" may be used here. In no case would the asset be marked higher than its market value. The amounts are then summed (treating debit adjustments as negative amounts) to yield a balance. The correct distribution of the difference between implied and book values depends on the market values of the underlying assets and liabilities. If the difference is larger than the amount needed to adjust all net assets, then, the excess is goodwill. In the past, firms looking for creative ways to avoid recording goodwill sometimes wrote off a portion of the purchase price as an immediate expense under the guise of in-process R&D. This issue has been a controversial one, and current GAAP requires that in-process R&D be capitalized if it is acquired in a business combination. Johnson & Johnson (J&J) agreed to acquire privately owned TransForm Pharmaceuticals for $230 million in 2005. The transaction resulted in a one-off $50 million after-tax charge relating to the acquisition of in-process R&D. The deal was aimed at enhancing J&J's ability to leverage existing elements in its pipeline. Under current GAAP, this treatment of in-process R&D is no longer allowed." By adjusting all net assets to their market value, a negative balance could re- sult. This situation, referred to as a bargain acquisition, occurs when the acquisi tion price is less than the market value of identifiable net assets acquired. After climi- nating any previously recorded goodwill on the books of the acquiree, this negative balance is recognized in its entirety as an ordinary gain in the income statement in the period of the acquisition. We will illustrate bargain acquisitions, which were initially introduced in Chapter 2, again in Chapter 5. The treatment of bargain purchase reflects a significant change from prior GAAP, which required that neg ative goodwill be allocated as a reduction of acquired assets below their fair value. Such a reduction is no longer allowed. Textbook problems (including those at the end of this chapter) will often make simplifying assumptions, such as "Assume that any difference between implied and book values is attributable solely to land," or "Assume that any difference between implied and book values is attributable to goodwill." This latter assumption is equiv alent to stating that book values approximate fair market values. It is important, however, to be aware that more complex adjustments are often needed, and may in- clude a variety of asset and liability accounts (as illustrated in detail in Chapter 5). Returning to the example above, in which a difference of $12.500 is attributed to land, a workpaper for a consolidated balance sheet at the date of acquisition in this situation is presented in Illustration 3-4. The first workpaper investment elimination entry is: (1) Common Stock-S Company 50,000 Other Contributed Capital-S Company 10,000 Retained Earnings-S Company 20,000 Difference between Implied and Book Values Investment in S Company 12.500 74,000 Noncontrolling Interest in Equity 18,500 World Markets Research Center, J&J Seeks R&D Boost Through Acquisition of TransForm Pharmaceuti cals," by Henry Dummett, 3/10/05. Case 2 (b): Implied Value Exceeds Book Value of Subsidiary Company's Equity (IV> BV)-Partial Ownership (Less Than 100% of Subsidiary Stock Acquired) Next, we continue to allow for a noncontrolling interest, and we introduce a difference between the cost and the book value acquired, and thus between the implied value and the book value of the subsidiary. In Case 2, we illustrate the common situation where the purchase price is higher than the book value of equity acquired. Assume that on January 1, 2013, P Company acquired 4,000 shares (80%) of the outstanding common stock of S Company for $74,000 cash, after which P Company has $26,000 in cash and $74,000 in an Investment in S Company. The purchase price of $74,000 for 80% of S Company implies a total value of $74,000/80% or $92,500. The implied value of the noncontrolling interest is $92,500 x 20% or $18,500. The total implied value of $92.500 exceeds the book value of equity of $80,000 by $12.500. A Computation and Allocation of Differ- ence (CAD) Schedule for this situation begins as follows: Computation and Allocation of Difference (between Implied and Book Values) Schedule Noncontrolling Parent Shee Share Total Vie Purchase price and implied value $74,000 18,500 92.500 Less: Book value of equity acquired: Common stock 40,000 10,000 50,000 Other contributed capital 8,000 2000 10,000 Retained earnings 16,000 4,000 20,000 Total book value 64,000 16.000 80,000 Difference between implied and book value 10,000 12,500 In this case, because there is a difference between implied and book values, we must not only compute the difference but also allocate that difference to the appro- priate accounts. If we assume that the entire difference is attributable to land with a current market value higher than its historical recorded cost, we would complete the CAD schedule as follows: Computation and Allocation of Difference (between Implied and Book Values) Schedule Noncontrolling Shaw Total Value Purchase price and implied value $74,000 18,500 92,500 Less: Book value of equity acquired: Common stock 40,000 10,000 50,000 Other contributed capital 8,000 2.000 10,000 Retained earnings 16,000 4,000 20,000 Total book value 64.000 16,000 80,000 Difference between implied and book value 10,000 2500 12,500 Adjust land upward (mark to market) (10000) (2.500) (12,500) Balance

Acquisition Accounting Implied Value Equals Book Value 90% Owned Subsidiary Date of Acquisition ILLUSTRATION 3-3 Consolidated Balance Sheet Workpaper P Company and Subsidiary January 1, 2013 Eliminations P Company S Company Dr. Cr Noncontrolling Consolidated Interest Balances Cash $ 28,000 $ 20,000 $ 48,000 Other Current Assets 140,000 50,000 190,000 Plant and Equipment 120,000 40,000 160,000 Land 40,000 20,000 60,000 Investment in S Company 72,000 (1) 72,000 Total Assets $400,000 $130,000 $458,000 Liabilities 60,000 50,000 110,000 Common stock P Company 200,000 200,000 S Company 50,000 (1) 50,000 Other Contributed Capital P Company 40,000 40,000 S Company 10,000 (1) 10,000 Retained Earnings P Company 100,000 100,000 S Company 20,000 (1) 20,000 Noncontrolling Interest (1) 8,000) $8,000 8,000 Total Liabilities and Equity $400,000 $130,000 $80,000 $80,000 $458,000 (1) To eliminate investment in S Company and create noncontrolling interest account. Case 200 med Values Vale of Company's Equity (VSV-Partial Ownership The 100% of Subsidiary Stock Acquired coon where the a The the da Case 2 Implied Value Exceeds Book Value of Subsidiary Company's Equity > B-Partial Ownership Less Than 100% of Subsidiary Stock Acquired 116 the CAD d The few 116 In this case, because these is a difference been implied and book value must not only compute the difference but aho allocate that difference to the appe priate accoumes. If we assume that the entire difference is attributable to land with a comment market value higher than its historical moded cost, we would comple the CAD schedule as fol Computation and Allocation of Difference between Implied and Book Values Schedule Law Book of The difference be allocated to specific accounts. In this example, the ad justment to increase land so its marker value is a debit, and is shown in parentheses The popular phrase "mack to market may be used here. In one would the ant of the difference between implest and book values depends on the market sales of de underlying assets and labies If the difference is larger than the ded to just all net amets, then, the es i godi In the past, firms looking for crative ways to avoid recording goodwill sometimes wrote all a portion of the purchase price as an immediate expense under the pine of proces R&D). This has been a controversial on and slut in peers R&D be capitalised if it is aired in a h GAAP requires IN THE NOIS GAAP meatment of ingrass R&D is no longer allowed Beating all neat to their market value, a negative balance could re- in situation, referred to as a bargain aquisition occurs when the acquis tion price is less than the market value of identifiable to acquired. After clim nating any previously recorded goodwill on the books of the acquire, this in the period of the acquisition. We will illustrate bargain acquisitions, which were initially introduced in Chapter 2, again in Chapter 3. The weatment of bargain purchase reflects a significant change hom prior GAAP, which required that neg ative goodwill be allocated as a reduction of acquired assets below their fair Such a reduction is no longer allowed Textbook problems including those at the e at the end of this chapter) will aten make simplifying a sch as "Assume that any difference between implied and book does is attributable solely to land" or "me that any difference between implied and book o to goodwill This later asumption is equi alent to stating that book values approximate fair market sales pr however, to be aware that more complex adjustments are often needed, and may chale a variety of asset and B and liability accounts as illustrated in detail in Chapter 3). Returning the example abone, in which a dillerence of $12.500 inatibuted land, a workpaper for a consolidated balance sheet at the date of acquisitionin this situation is presented in Illustration 3-4 The first workpaper is elamination entry i Acquisition Accounting Implied Value Equal Book Value 90% Owned Subsidiary Date of Acquisition ILLUSTRATION 3-3 Consolidated Balance Sheet Workpaper P Company and Subsidiary January 1, 2013 Eliminations PCompany S Company Dr. Noncontrolling Consolidated Interest Balances Cash $ 28,000 $ 20,000 $ 48,000 Other Current Assets 140,000 50,000 190,000 Plant and Equipment 120,000 40,000 160,000 Land 40,000 20,000 60,000 Investment in S Company 72,000 (1) 72,000 Total Assets $400,000 $130,000 $458,000 Liabilities 60,000 50,000 110,000. Common stock. P Company 200,000 200,000 S Company 50,000 (1) 50,000 Other Contributed Capital P Company 40,000 40,000 S Company 10,000 (1) 10,000 Retained Earnings P Company 100,000 100,000 S Company 20,000 (1) 20,000 Noncontrolling Interest (1) 8,000 $8,000 8,000 Total Liabilities and Equity $400,000 $130,000 $80,000 $80,000 $458,000 (1) To eliminate investment in S Company and create noncontrolling interest account. In comparing Illustration 3-2 and Illustration 3-3, it might be noted that: (1) consolidated assets are $8,000 greater in Illustration 3-3 since it took $8,000 less cash to acquire a 90% investment, and (2) an $8,000 noncontrolling interest exists (the remaining 10%). Noncontrolling interest is accumulated on the consolidated workpaper in a separate column. The proper classification of the noncontrolling interest has been a subject of debate. From the perspective of the controlling interest, it is similar to a liability. It is not, however, a liability because it does not require a future payment by the parent company or the consolidated entity. The shareholders who represent the noncon- trolling interest are indeed stockholders, but only of the subsidiary company and not the parent. Some companies, in the past, presented this interest after liabilities and before stockholders' equity on the balance sheet to convey the "hybrid" nature of the noncontrolling interest. According to FASB Statement No. 160 [ASC 810-10-45-16]. the noncontrolling interest should be presented as a part of stockholders' equity of the consolidated entity, but clearly labeled to distinguish it from the other equity accounts. "The term minority interest may not reflect clearly the actual nature of some items. For example, a par- ent company may own 25% of its subsidiary's outstanding preferred stock. In this case, the use of the term "minority interest" to represent the 75% interest held by noncontrolling shareholders is not representa tive of the circumstances. Also, a parent may have control of a subsidiary with less than 50% of its common stock. The term "noncontrolling interest" is recommended by FASB and is used throughout this text. IN THE NEWS The difference must be allocated to specific accounts. In this example, the ad- justment to increase land to its market value is a debit, and is shown in parentheses. The popular phrase "mark to market" may be used here. In no case would the asset be marked higher than its market value. The amounts are then summed (treating debit adjustments as negative amounts) to yield a balance. The correct distribution of the difference between implied and book values depends on the market values of the underlying assets and liabilities. If the difference is larger than the amount needed to adjust all net assets, then, the excess is goodwill. In the past, firms looking for creative ways to avoid recording goodwill sometimes wrote off a portion of the purchase price as an immediate expense under the guise of in-process R&D. This issue has been a controversial one, and current GAAP requires that in-process R&D be capitalized if it is acquired in a business combination. Johnson & Johnson (J&J) agreed to acquire privately owned TransForm Pharmaceuticals for $230 million in 2005. The transaction resulted in a one-off $50 million after-tax charge relating to the acquisition of in-process R&D. The deal was aimed at enhancing J&J's ability to leverage existing elements in its pipeline. Under current GAAP, this treatment of in-process R&D is no longer allowed." By adjusting all net assets to their market value, a negative balance could re- sult. This situation, referred to as a bargain acquisition, occurs when the acquisi tion price is less than the market value of identifiable net assets acquired. After climi- nating any previously recorded goodwill on the books of the acquiree, this negative balance is recognized in its entirety as an ordinary gain in the income statement in the period of the acquisition. We will illustrate bargain acquisitions, which were initially introduced in Chapter 2, again in Chapter 5. The treatment of bargain purchase reflects a significant change from prior GAAP, which required that neg ative goodwill be allocated as a reduction of acquired assets below their fair value. Such a reduction is no longer allowed. Textbook problems (including those at the end of this chapter) will often make simplifying assumptions, such as "Assume that any difference between implied and book values is attributable solely to land," or "Assume that any difference between implied and book values is attributable to goodwill." This latter assumption is equiv alent to stating that book values approximate fair market values. It is important, however, to be aware that more complex adjustments are often needed, and may in- clude a variety of asset and liability accounts (as illustrated in detail in Chapter 5). Returning to the example above, in which a difference of $12.500 is attributed to land, a workpaper for a consolidated balance sheet at the date of acquisition in this situation is presented in Illustration 3-4. The first workpaper investment elimination entry is: (1) Common Stock-S Company 50,000 Other Contributed Capital-S Company 10,000 Retained Earnings-S Company 20,000 Difference between Implied and Book Values Investment in S Company 12.500 74,000 Noncontrolling Interest in Equity 18,500 World Markets Research Center, J&J Seeks R&D Boost Through Acquisition of TransForm Pharmaceuti cals," by Henry Dummett, 3/10/05. Case 2 (b): Implied Value Exceeds Book Value of Subsidiary Company's Equity (IV> BV)-Partial Ownership (Less Than 100% of Subsidiary Stock Acquired) Next, we continue to allow for a noncontrolling interest, and we introduce a difference between the cost and the book value acquired, and thus between the implied value and the book value of the subsidiary. In Case 2, we illustrate the common situation where the purchase price is higher than the book value of equity acquired. Assume that on January 1, 2013, P Company acquired 4,000 shares (80%) of the outstanding common stock of S Company for $74,000 cash, after which P Company has $26,000 in cash and $74,000 in an Investment in S Company. The purchase price of $74,000 for 80% of S Company implies a total value of $74,000/80% or $92,500. The implied value of the noncontrolling interest is $92,500 x 20% or $18,500. The total implied value of $92.500 exceeds the book value of equity of $80,000 by $12.500. A Computation and Allocation of Differ- ence (CAD) Schedule for this situation begins as follows: Computation and Allocation of Difference (between Implied and Book Values) Schedule Noncontrolling Parent Shee Share Total Vie Purchase price and implied value $74,000 18,500 92.500 Less: Book value of equity acquired: Common stock 40,000 10,000 50,000 Other contributed capital 8,000 2000 10,000 Retained earnings 16,000 4,000 20,000 Total book value 64,000 16.000 80,000 Difference between implied and book value 10,000 12,500 In this case, because there is a difference between implied and book values, we must not only compute the difference but also allocate that difference to the appro- priate accounts. If we assume that the entire difference is attributable to land with a current market value higher than its historical recorded cost, we would complete the CAD schedule as follows: Computation and Allocation of Difference (between Implied and Book Values) Schedule Noncontrolling Shaw Total Value Purchase price and implied value $74,000 18,500 92,500 Less: Book value of equity acquired: Common stock 40,000 10,000 50,000 Other contributed capital 8,000 2.000 10,000 Retained earnings 16,000 4,000 20,000 Total book value 64.000 16,000 80,000 Difference between implied and book value 10,000 2500 12,500 Adjust land upward (mark to market) (10000) (2.500) (12,500) Balance Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield, Nicola M. Young, Irene M. Wiecek, Bruce J. McConomy

11th Canadian edition Volume 2

1119048540, 978-1119048541