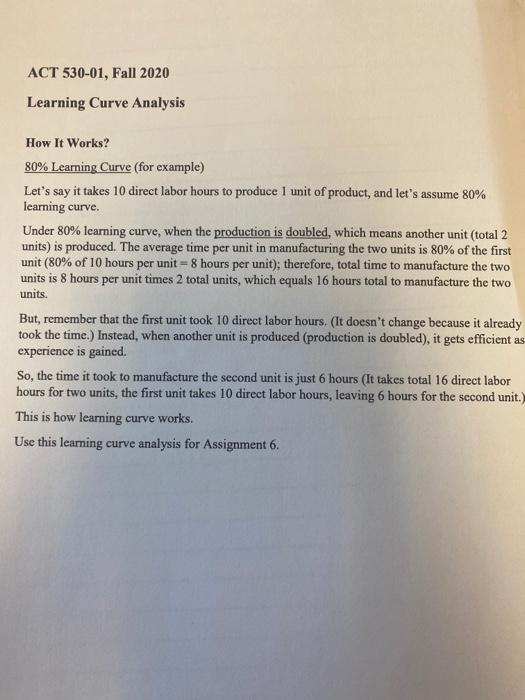

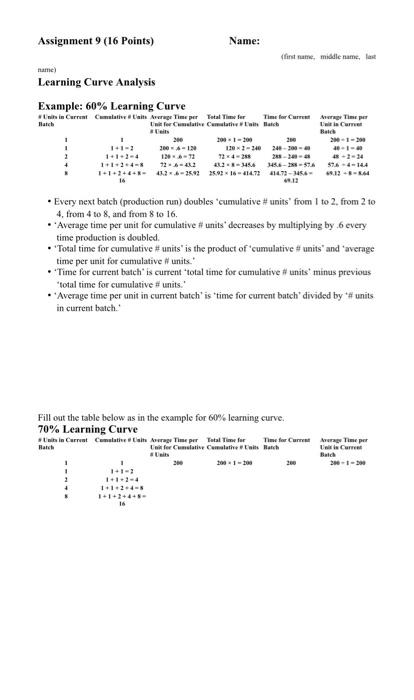

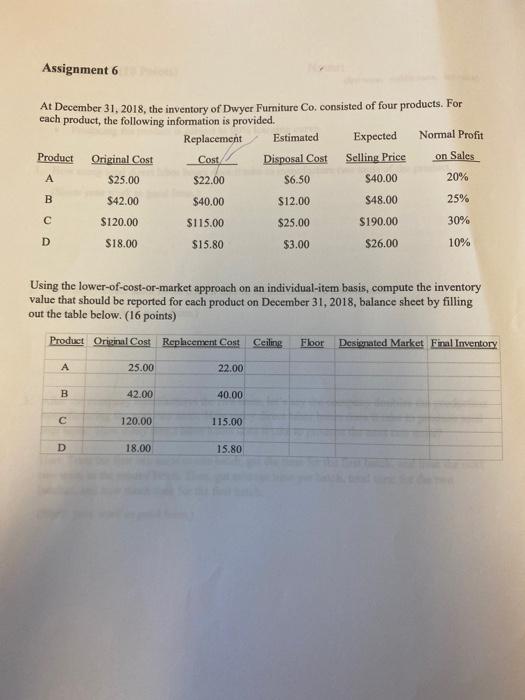

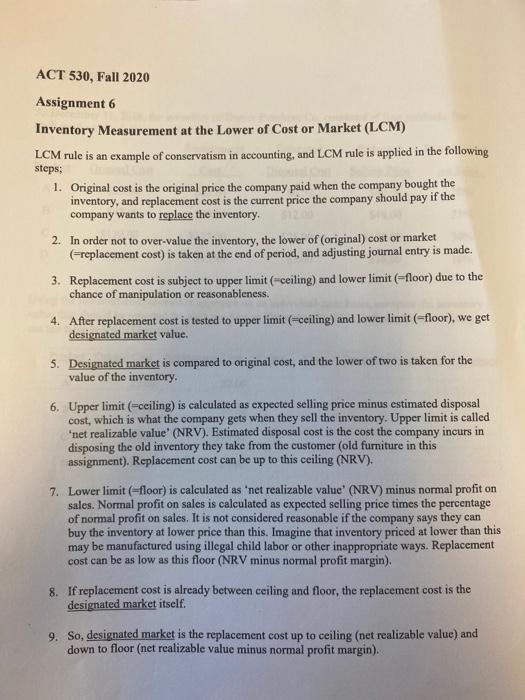

ACT 530-01, Fall 2020 Learning Curve Analysis How It Works? 80% Learning Curve (for example) Let's say it takes 10 direct labor hours to produce 1 unit of product, and let's assume 80% learning curve. Under 80% learning curve, when the production is doubled, which means another unit (total 2 units) is produced. The average time per unit in manufacturing the two units is 80% of the first unit (80% of 10 hours per unit = 8 hours per unit); therefore, total time to manufacture the two units is 8 hours per unit times 2 total units, which equals 16 hours total to manufacture the two units. But, remember that the first unit took 10 direct labor hours. (It doesn't change because it already took the time.) Instead, when another unit is produced (production is doubled), it gets efficient as experience is gained. So, the time it took to manufacture the second unit is just 6 hours (It takes total 16 direct labor hours for two units, the first unit takes 10 direct labor hours, leaving 6 hours for the second unit.) This is how learning curve works. Use this learning curve analysis for Assignment 6. Assignment 9 (16 points) Name: (first name, middle name, la name Learning Curve Analysis Example: 60% Learning Curve hin Gurrent Clative ai rage Time per Total Time for Time for Car Ang Time talaila Cartartin tmins laish -- 300-19 120*1-340-30- 2 12-13 24 25-34-183-34 1+1 24 72 -- 452 42-46 8.-I-SA 574-144 1+1+2+3+*-412-2.2 25.92 16-1472 147-15-13-3-5 Bali Every next batch (production run) doubles 'cumulative #units from 1 to 2. from 2 10 4, from 4 to and from 8 to 16. Average time per unit for cumulative #units' decreases by multiplying by 6 every time production is doubled Total time for cumulative #units" is the product of "cumulative# units" and average time per unit for cumulative units. Time for current batch is current total time for cumulative #units minus previous total time for cumulative units. Average time per unit in current batch' is time for current batch divided by *# units in current batch Fill out the table below as in the example for 60% learning curve. 70% Learning Curve in Current Cumulate forage Time per Tatal Time for Time for Current Average Time per alt for Cumulative Comalatietis Ratch Un Current Baie 300-300 1-30 1- 2 111-4 11.2.- 1+1++4+5- 16 Assignment 6 At December 31, 2018, the inventory of Dwyer Furniture Co. consisted of four products. For each product, the following information is provided. Replacement Estimated Expected Normal Profit Product Original Cost Cost Disposal Cost Selling Price on Sales $25.00 $22.00 $6.50 $40.00 20% $42.00 $40.00 $12.00 $48.00 25% $120.00 $115.00 $25.00 $190.00 30% B D $18.00 $15.80 $3.00 $26.00 10% Using the lower-of-cost-or-market approach on an individual-item basis, compute the inventory value that should be reported for each product on December 31, 2018, balance sheet by filling out the table below. (16 points) Product Original Cost Replacement Cost Ceiling Floor Designated Market Final Inventory 25.00 22.00 B 42.00 40.00 C 120.00 115.00 D 18.00 15.80 ACT 530, Fall 2020 Assignment 6 Inventory Measurement at the Lower of Cost or Market (LCM) LCM rule is an example of conservatism in accounting, and LCM rule is applied in the following steps: 1. Original cost is the original price the company paid when the company bought the inventory, and replacement cost is the current price the company should pay if the company wants to replace the inventory. 2. In order not to over-value the inventory, the lower of (original) cost or market (=replacement cost) is taken at the end of period, and adjusting journal entry is made. 3. Replacement cost is subject to upper limit (-ceiling) and lower limit (=floor) due to the chance of manipulation or reasonableness. 4. After replacement cost is tested to upper limit (-ceiling) and lower limit (-floor), we get designated market value. 5. Designated market is compared to original cost, and the lower of two is taken for the value of the inventory 6. Upper limit (=cciling) is calculated as expected selling price minus estimated disposal cost, which is what the company gets when they sell the inventory. Upper limit is called "net realizable value' (NRV). Estimated disposal cost is the cost the company incurs in disposing the old inventory they take from the customer (old furniture in this assignment). Replacement cost can be up to this ceiling (NRV). 7. Lower limit (-floor) is calculated as 'net realizable value' (NRV) minus normal profit on sales. Normal profit on sales is calculated as expected selling price times the percentage of normal profit on sales. It is not considered reasonable if the company says they can buy the inventory at lower price than this. Imagine that inventory priced at lower than this may be manufactured using illegal child labor or other inappropriate ways. Replacement cost can be as low as this floor (NRV minus normal profit margin). 8. If replacement cost is already between ceiling and floor, the replacement cost is the designated market itself. 9. So, designated market is the replacement cost up to ceiling (net realizable value) and down to floor (net realizable value minus normal profit margin). ACT 530-01, Fall 2020 Learning Curve Analysis How It Works? 80% Learning Curve (for example) Let's say it takes 10 direct labor hours to produce 1 unit of product, and let's assume 80% learning curve. Under 80% learning curve, when the production is doubled, which means another unit (total 2 units) is produced. The average time per unit in manufacturing the two units is 80% of the first unit (80% of 10 hours per unit = 8 hours per unit); therefore, total time to manufacture the two units is 8 hours per unit times 2 total units, which equals 16 hours total to manufacture the two units. But, remember that the first unit took 10 direct labor hours. (It doesn't change because it already took the time.) Instead, when another unit is produced (production is doubled), it gets efficient as experience is gained. So, the time it took to manufacture the second unit is just 6 hours (It takes total 16 direct labor hours for two units, the first unit takes 10 direct labor hours, leaving 6 hours for the second unit.) This is how learning curve works. Use this learning curve analysis for Assignment 6. Assignment 9 (16 points) Name: (first name, middle name, la name Learning Curve Analysis Example: 60% Learning Curve hin Gurrent Clative ai rage Time per Total Time for Time for Car Ang Time talaila Cartartin tmins laish -- 300-19 120*1-340-30- 2 12-13 24 25-34-183-34 1+1 24 72 -- 452 42-46 8.-I-SA 574-144 1+1+2+3+*-412-2.2 25.92 16-1472 147-15-13-3-5 Bali Every next batch (production run) doubles 'cumulative #units from 1 to 2. from 2 10 4, from 4 to and from 8 to 16. Average time per unit for cumulative #units' decreases by multiplying by 6 every time production is doubled Total time for cumulative #units" is the product of "cumulative# units" and average time per unit for cumulative units. Time for current batch is current total time for cumulative #units minus previous total time for cumulative units. Average time per unit in current batch' is time for current batch divided by *# units in current batch Fill out the table below as in the example for 60% learning curve. 70% Learning Curve in Current Cumulate forage Time per Tatal Time for Time for Current Average Time per alt for Cumulative Comalatietis Ratch Un Current Baie 300-300 1-30 1- 2 111-4 11.2.- 1+1++4+5- 16 Assignment 6 At December 31, 2018, the inventory of Dwyer Furniture Co. consisted of four products. For each product, the following information is provided. Replacement Estimated Expected Normal Profit Product Original Cost Cost Disposal Cost Selling Price on Sales $25.00 $22.00 $6.50 $40.00 20% $42.00 $40.00 $12.00 $48.00 25% $120.00 $115.00 $25.00 $190.00 30% B D $18.00 $15.80 $3.00 $26.00 10% Using the lower-of-cost-or-market approach on an individual-item basis, compute the inventory value that should be reported for each product on December 31, 2018, balance sheet by filling out the table below. (16 points) Product Original Cost Replacement Cost Ceiling Floor Designated Market Final Inventory 25.00 22.00 B 42.00 40.00 C 120.00 115.00 D 18.00 15.80 ACT 530, Fall 2020 Assignment 6 Inventory Measurement at the Lower of Cost or Market (LCM) LCM rule is an example of conservatism in accounting, and LCM rule is applied in the following steps: 1. Original cost is the original price the company paid when the company bought the inventory, and replacement cost is the current price the company should pay if the company wants to replace the inventory. 2. In order not to over-value the inventory, the lower of (original) cost or market (=replacement cost) is taken at the end of period, and adjusting journal entry is made. 3. Replacement cost is subject to upper limit (-ceiling) and lower limit (=floor) due to the chance of manipulation or reasonableness. 4. After replacement cost is tested to upper limit (-ceiling) and lower limit (-floor), we get designated market value. 5. Designated market is compared to original cost, and the lower of two is taken for the value of the inventory 6. Upper limit (=cciling) is calculated as expected selling price minus estimated disposal cost, which is what the company gets when they sell the inventory. Upper limit is called "net realizable value' (NRV). Estimated disposal cost is the cost the company incurs in disposing the old inventory they take from the customer (old furniture in this assignment). Replacement cost can be up to this ceiling (NRV). 7. Lower limit (-floor) is calculated as 'net realizable value' (NRV) minus normal profit on sales. Normal profit on sales is calculated as expected selling price times the percentage of normal profit on sales. It is not considered reasonable if the company says they can buy the inventory at lower price than this. Imagine that inventory priced at lower than this may be manufactured using illegal child labor or other inappropriate ways. Replacement cost can be as low as this floor (NRV minus normal profit margin). 8. If replacement cost is already between ceiling and floor, the replacement cost is the designated market itself. 9. So, designated market is the replacement cost up to ceiling (net realizable value) and down to floor (net realizable value minus normal profit margin)