Question: Activity Based Costing (ABC) Background Information: Nick's Woodworking Inc. began operations in 2023 as a manufacturer of picnic tables with attached benches. During its first

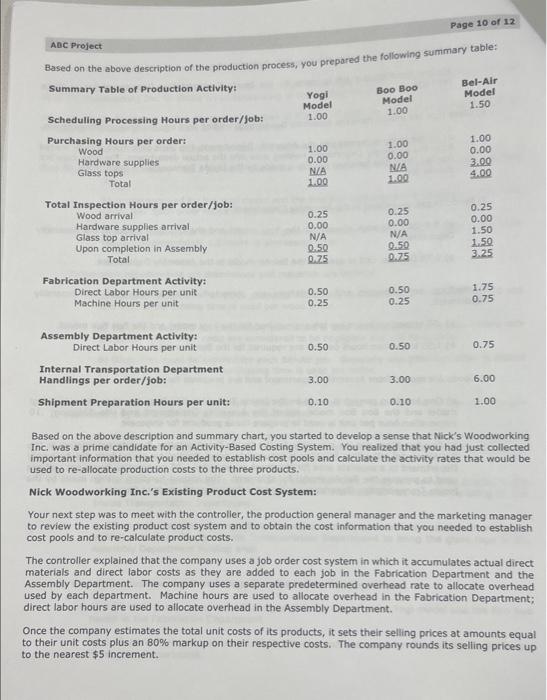

Background Information: Nick's Woodworking Inc. began operations in 2023 as a manufacturer of picnic tables with attached benches. During its first decade of operations, the company produced two styles of tables: the Yogi (deluxe) model and the Boo Boo (standard) model. The company was an overnight success as it found a strong market for its products among value-conscious consumers. Nick's Woodworking inc. Was able to place its products with leading retailers because of consumer demand as well as its reputation service-oriented trading partner. The company's cheesy marketing slogan, "Pick Nick's Tables", enhanced the company's reputation as a no-frills, no-nonsense supplier of high-quality products at reasonable prices. In early 2018, management decided that it needed to invest in a significant expansion and upgrade of its production facility. The project was completed by the end of 2018. Within months management realized that they over-built and therefore had excess production capacity. The excess capacity increased production costs of the company's products. At first, management decided to absorb the increased costs and therefore did not increase its selling prices. That choice resulted in a steady decline in the company's profits. Management was eventually forced to raise its prices during the last quarter of 2019 in an attempt to return its historical level of profitability. Consumer demand was relatively unaffected by the modest price increases; the company reported a higher level of profits for the first quarter of 2020 than it reported in any of the three previous quarters. Competing models still could not erode the company's market share and no new competing models were introduced during 2020. Management was pleased with the initial results of its actions, particularly because the company was unaffected by the pandemic and supply chain issues. However, it decided that the price increases were not the best solution to the excess capacity problem. Management felt that it should put the capacity to use by manufacturing a third product. Thus the company began developing a new product that would use the company's woodworking expertise. Management wanted the new product to complement the company's existing products by targeting consumers who would not normally be attracted to its traditional wooden picnic tables. Uitimately a more upscale table model was developed. The new table had a glass surface with a wooden base and attached benches. The table was designed to be constructed of a higher-quality wood than the Yogi and Boo Boo models. Nick's Woodworking Inc. unveiled its third product during the fourth quarter of 2021, marketing it as the Bel-Air model. During the planning process for 2022, the company revised its product costs to reflect the usage of the excess capacity costs by the Bel-Air model. The resulting estimated production costs for the Yogi model and the Boo Boo model were significantly lower than their estimated costs for 2021. The company decided to not reduce the selling prices of its all-wood tables at the outset of 2022 for two reasons. First, the market seemed to readily accept the 2021 price increases as demand for the product was steady as compared to the preceding years. Second, management wanted to be conservative in it pricing of its primary products just in case the Bel-Air model failed to meet expectations. Managemen feared that the anticipated cost reductions could fall short of expectations or fail to materialize completely Management did not want to face the prospect of needing to raise its prices within months of reducing them The manopement of Nick's Woodworking Inc. Was very pleased with the introduction of the Bel-Alir model. Retailers were receptive to stocking the product as they felt demand for the product would be strong given 2022 Eventst its unique style, quality construction and moderate pricing. Initial consumer demand actually exceeded Unfortunately the Bel-Air model presented a number of unexpected challenges. Nick's Woodworking Inc. expectations of both management and its retailers. had always produced 100% of its products. The company only relied on suppliers for its lumber and hardware supplies such as bolts and screws. However, for the Bel-Air model, the company needed an Management decided to outsource the fabrication of the table's glass surface. That decision resulted in a entirely new component piece, the glass top. couple of unforeseen consequences. The company was inadequately prepared in terms of lts personnel and its purchasing and production information systems to elfectively manage its supply-chain relationship with the glass fabricator and coordinate the production of the wood bases with the receipt of glass tops. Furthermore, the glass tops required special handing from the moment the pleces arrived from the glas5 fabricator until the fintshed tables were shipped to retailers. The company was therefore forced to add people, update its information systems and modify its materials and product handing systems. In the process, it significantly increased its overhead costs. At the end of both the first and second quarters of 2022, the controller, the production general manager, And the marketing manager met to analyze production costs. On both occasions they increased the company's. predetermined overhead rate that, in turn, increased the estimated unit costs to produce the company's three products. The increased overhead costs allocated to the Yogi and Boo Boo models essentially wiped out the anticipated cost savings from the Bel-Air model. By the end of the second quarter, the estimated production costs to produce the Yogl and the Boo Boo models were approximately equal to their 2021 production costs. Management was relieved that it had decided to not reduce the prices of the two models for 2022. Grven the unexpected strong demand for the Bel-Air model, management decided it could pass along the Givereases in the model's estimated production costs. It ralsed its price to retailers (and the suggested retail price to consumers) at the end of both quarters. Many retallers expressed concerns about the price increases: they feared the increases would adversely affect consumer demand. Those concerns turmed out to be-unfounded as third quarter sales of the Bel-Air model exceeded original projections as well as the actual sales of the model in each of the two previous quarters. During the third quarter of 2022, the management of Nick's Woodworking Inc. was troubled by a new development. Two well-established woodworking companies introduced their own models of one-piece, wooden picnic tables. Their tables were designed to directly compete with both the Yogi model and the Boo Boo model. The tables were similar in style and quality to Nick's Woodworking Inc.'s models. The competing tables prices were about 8 to 10%6 lower than the company's current prices. Once again, the controller, the production general manager and the marketing manager met to analyze production costs. They determined that their prior estimated production costs were accurate and therefore production costs. They determined that their prior cstimated production costs were accurate and therefori model and the Boo Boo model to meet the competitors' did not support a reduction in the prices of the Yogi mon concluded that the competitors had most likely underpriced their products in an attempt to prices. They con mer gain market share. Despite the company's recent production and cost is its production processes that it developed over timantages over its new competitors due to efficlencies in tors prod to raise their prices in relatively short period of time. As the third and fourth quarter of 2022 progressed, the competitors showed no signs of raising their prices. Weekly sales of the Yogi model and the Boo Boo model steadily decined to levels that were well below the sales of the products for the same weeks in preceding years. The compamy lost market share for the first time in its history. Meanwhile sales of the Bel-Alr model during this period steadily increased. However, the increase in sales of the Bel-Air model appeared to be insufficient to offset the decreases in sales of the other models. The company reported the lowest quarterly profit in its fourteen-year history during the third quarter of 2022 and it projected a small loss for the fourth quarter of the year. As the end of 2022 approached, the management of Nick's Woodworking inc. Was in crisis mode. Proposed Solutions: The production general manager organized a series of meetings of his production managers to discuss the company's recent cost and production problems and search for solutions to those problems. The production group quickly reached a consensus about the root cause of the problems and the course of action that the company should adopt to solve the problems. The production managers attributed the majority of the problems to the Bel-Air model. They therefore advocated dropping the Bel-Air model. They claimed that the Bel-Air model burdened the Yogi model and the Boo Boo model with increased production costs that, in turn, led to the company's inability to meet the prices of the new competing models. They also revealed that the Bel Air model was a constant source of production problems that frequently resulted in excess waste of materials and idie labor time. The production managers unveiled preliminary drawings and specifications for new, all-wooden tables in the tradition of the Yogi and Boo Boo models. The specifications for their proposed products were similar to the company's traditional products. The managers argued that the design similarities would lead to a reduction of overall production costs through the elimination of costs that were added specifically for the Bel-Air model. They provided cost and production estimates for the new products and analyses of their resulting effects on the costs of the Yogi model and the Boo Boo model. Based on the analyses, they concluded that the company would return to its former levels of profitability because it would be able to not oniy meet the prices of the new competitors but actually lower the prices of its existing products back to their early 2020 levels. The marketing managers also worked as a group to ferret out the key problems and issues and develop proposed solutions. They ultimately reached a set of very different conclusions from the production managers. They explained that the introduction of competing products into the marketplace was evidence that the market for the company's original products had matured. They maintained that consumers' tastes had changed to the point where the price had become more important to consumers than product quality. The marketing managers felt that to effectively compete in such a market the company could no longer view itself as a "no-frills, no nonsense supplier of high-quality products at reasonable prices." The company would need to fundamentally change itself and its mission and become a producer of "low-cost, marginalquality products." The marketing managers felt that such an extreme change was tll-advised. Instead, the marketing managers wanted the company to slowly withdraw from the all-wooden table market and shift its focus to the upscale market that the company successfully entered with its Bel-Air model. They argued for the development of new mixed-material products that would complement the Bel-Air model. To support their position, they presented market research studies that indicated the company could further increase the price of the Bel-Air model without affecting consumer demand. The research studies also provided evidence of an under-developed market for products similar to the Bel-Air model. By focusing on products for upscale consumers, Nick's Woodworking Inc. could continue its tradition as a supplier of highquality products at reasonable prices and return to its former levels of profitability. ABC Project Page 4 of 12 Uitimately, the two groups pitched their ldeas and arguments to the company's controller. As she listened to the presentations and reviewed the supporting documentation for the two wildly-opposite proposals, she became convinced that both arguments contained elements of truth that she needed to reconcile before she could recommend or reject elther proposal. She decided that she should write down her thoughts to ensure that she correctly understood the issues. Her notes read: Marketing Proposal 1) The marketing research relative to the Bel-Air model's pricing is the most compelling evidence in the proposal. 2) I analyzed the production costs of all of our products three times during the previous year and am satisfied that there were no errors or omissions in tracking and developing the production costs. 3) I interpret the market research results to mean that we set the price of the Bel-Air model too low despite the accuracy of the cost data produced by our accounting system. Production Proposal 1) I am equally fascinated with the production and cost analyses prepared by the production managers. 2) All of their assumptions and estimates are reasonable and their calculations are accurate. 3) I agree with their conclusions that the Yogi model and Boo Boo model could be produced at costs that would profitably support price decreases to their 2020 levels under two conditions: a) The Yogi and Boo Boo models cannot be burdened with the excess costs created by the Bel-Air model, and b) The Yogi and Boo Boo modeis cannot be burdened with the costs created by the old excess capacity. she finished writing the last note, she realized that the company's real problem might not be a marketing le or a production issue. The real problem might be an accounting issue. The marketing research cated that the Bel-Air model was underpriced yet product costs analyses indicated that it was not. fuction wanted to shift costs away from the Yogi model and the Boo Boo model by introducing new Jucts. However, maybe the costs could be shifted from the old models without developing entirely new lucts. Maybe the costs could be allocated to the Bel-Air model simply by changing the accounting em. If they could be shifted to the Bel-Air model then the resulting cost of the Bel-Air model would ort a higher price as suggested by the market research. finally, that is where you come in! will only make limited use of the information in the above narrative in this assignment. ever, you need to read the narrative carefully to be able to understand the typical business is that an Activity-Based Costing System addresses. I will be happy to answer any questions you might have about the facts presented in the narrative. You were hired as outside consultant(s) by Nick's Woodworking Inc. to analyze the company's existing product costing system and to recommend changes in that system. Your product in this assignment will be a memo to the controller of Nick's Woodworking Inc, that recommends changes to the company's current product cost system, product costs and the selling prices of its products. Your recommendations will focus on a switch from the company's traditional product costing system to an Activity-Based Costing System. Your report must include: 1) A one-page summary memo that includes: a) A one to two paragraph discussion that articulates your understanding of the problem that you were hired to address. b) A brief statement that identifies your recommendations relative to: i. changes in the company's product cost system ii. resulting changes in the production costs of the company's three products iii. new selling prices for the company's three products You may present your recommendations in bullet point format in the executive summary, and you may also include small tables. You should briefly present your recommendations in the executive summary without justifications and explanations. Normally a consultant would begin a memo to a client with a thorough discussion of the consultant's understanding of the client's problem. The consulting would then supply a general description of the work the consultant performed, the resources used and assumptions that were made. You SHOULD NOT include such discussions in your memo as you would merely be restating much of the background information and instructions that you received from me in this assignment handout. 2) You will begin your memo with a brief description of Nick's Woodworking Inc.'s current product cost system. As part of your discussion, you must include a table or a series of tables that clearly identify: a) The 2023 unit cost and selling price of each model based on the current product cost system. b) Projected 2023 sales in units and in total revenue for each model resulting from the costs and prices resulting from the current product system. c) The company's projected operating profit or loss for 2023 based on the current product cost system and other budgeted information. d) The company's annual breakeven point using the cost projections obtained from the current product cost system. Use the Existing worksheet in the Excel file provided to prepare these supporting calculations. ABC Project 3) You will then provide a brief description of your recommended changes in the product cost system used by Nick's Woodworking Inc. As part of your discussion, you must include brief justifications for these changes, You must also present a table or a serles of tobles that clearly identify: a) The 2023 unit cost and selling price of each model based on the new product cost system. b) Projected 2023 sales in units and in total revenue for each model resulting from the costs and prices resulting from the new product system. c) The company's projected operating profit or loss for 2023 based on the information derived from the new product cost system. d) The company's annual breakeven point using the cost projections obtained from the new product cost system. Use the Proposed worksheet in the Excel file provided to prepare these supporting calculations. 4) You will then provide a brief conclusion that identifies the effects of your recommended changes in the product cost system used by Nick's Woodworking Inc. You should identify and quantify, whenever possible, the benefits of the new system. You may use a bullet point format and/or tables in your discussion. As you read the details of the production process, you should attempt to identify at least one production activity that would be considered a "non-value added activity" that the company should attempt to eliminate. You should include a description of that activity and explain to the client why the client should attempt to eliminate that activity. Other Instructions/Requirements: Your memo must be typed. I would prefer double spaced lines so that I may have room to include my grading comments. I assume that your memo will need to be a minimum of four pages (including the executive summary) to minimally address the assignment requirements. You will present the required supporting calculations in the worksheet in the Excel file provided. You will upload your Excel file to Blackboard for my review. Please include at least one team member's name in the file name prior to uploading it to Blackboard. This assignment will be due Wednesday, April 5. arading Criteria: will grade your using the following criteria and weights. Nick's Woodworking Inc.'s Production Processt As part of your work, you met with the production managers including the general manger and the controller of Nick's Woodworking Inc. to obtain an understanding of the production process. As a group you developed a step-by-step description of the major activities that occur in the production process of the three products. Here is that description: 1) Customer orders are received and jobs are entered into production schedule. a) The company uses a job order cost system. Each customer order is produced as a separate job. b) Orders received for the Yogl model and the Boo Boo model generally average at 250 units per order. Each order requires approximately 1.0 hour of processing time. c) Orders received for the Bel-Air model generally average at 100 units per order. Each order requires approximately 1.5 hours of processing time. 2) Materials requirements are determined and materials are ordered. a) Wood is required for all three products. Generally one wood order is placed per job and one hour of purchasing time is used per wood order. b) Hardware supplies are periodically purchased in bulk using standing purchase orders with suppliers. Their order costs are considered to be negligible and will be ignored. b) Glass tops must be ordered for each Bel-Air job. Generally one glass top order is placed per job and three hours of purchasing time is used per order. 3) Materials arrive from the suppliers and are inspected and then moved to the appropriate department by the Inside Transportation Department. a) Wood requires. 25 inspection hours per order/job on arrival from the lumber mill and one handling per order/job is made by the Inside Transportation Department to bring the wood to the Fabrication Department. b) Hardware supplies require little, if any, inspection time. They are delivered directly to the Assembly Department area by the suppliers and therefore do not require handling by the Inside Transportation Department. c) Glass tops require 1.5 inspection hours per order/job on arrival and one handling per order/job is made by the Inside Transportation Department to bring the glass tops to the Assembly Department holding area. 4) The wood is fabricated (cut and shaped) in the Fabrication Department. a) 0.25 MH's per unit and 0.50 DLH's per unit are used for the Yogi model and the Boo Boo model in the Fabrication Department. b) 0.75 Mh's DLH per unit and 1.75 DLH's per unit are used for the Bel-Air model in the Fabrication Department. Page 9 of 12 5) The fabricated wood is sent to the Assembly Department. a) One handling per job is made by the Inside Transportation Department for all three products. 6) Glass tops are moved from the Assembly Department holding area into the Assembly Department. a) As the wood is moved into the Assembly Department, the glass tops must also be moved from the Assembly Department Holding area into the actual department. The glass tops are fragile. Thus one handling per job is made by the Inside Transportation Department on each Bel-Air job. 7) Products are assembled in the Assembly Department. a) 0.5 DLH per unit is used for the Yogi model and the Boo Boo model in the Assembly Department b) 0.75DL per unit is used for the Bel-Air model in the Assembly Department. 8) Products are inspected and any defects are corrected before goods leave the Assembly Department. a) .50 inspection hours per job are required for the Yogi model and the Boo Boo model. b) 1.50 inspection hours per job are required for the Bel-Air model. 9) Goods are moved from Assembly Department and are prepared for shipment: a) One handling per job is made by the Inside Transportation Department to move the Yogi model and the Boo Boo model out of the Assembly Department and into Shipping; .10 preparation hour per unit is used to prepare these products for shipment b) Two handlings per job are made by the Inside Transportation Department relative to the Bel-Air model. The first handling is required to move the Bel-Air model from the Assembly Department to a separate area for shipment preparation. . 25 preparation hours per unit are used to prepare the Bel-Air model for shipment. The second handling is then made by the Inside Transportation Department to transfer the prepared goods to Shipping. ABC Project Based on tha ahave descriotion of the production process, you prepored the following summary table: Based on the above description and summary chart, you started to develop a sense that Nick's Woodworking Inc. was a prime candidate for an Activity-Based Costing System. You realized that you had just collected important information that you needed to establish cost pools and calculate the activity rates that would be used to re-allocate production costs to the three products. Nick Woodworking Inc.'s Existing Product Cost System: Your next step was to meet with the controller, the production general manager and the marketing manager to review the existing product cost system and to obtain the cost information that you needed to establish cost pools and to re-calculate product costs. The controller explained that the company uses a job order cost system in which it accumulates actual direct materials and direct labor costs as they are added to each job in the Fabrication Department and the Assembly Department. The company uses a separate predetermined overhead rate to allocate overhead used by each department. Machine hours are used to allocate overhead in the Fabrication Department; direct labor hours are used to allocate overhead in the Assembly Department. Once the company estimates the total unit costs of its products, it sets their selling prices at amounts equal to their unit costs plus an B0\% markup on their respective costs. The company rounds its selling prices up to the nearest $5 increment. mu5, if the company determined that a product had a unit cost (including materials, labor and overhead) of $130; it would add an 80% markup or $104 to that cost to arrive at a preliminary selling price of $234 per unit. The company would then round that price up to the nearest $5 increment and would therefore charge $235 for the product. The controller handed to you an analysis of product demand, production activity and expected product costs that she had prepared with assistance from the marketing manager and the production general manager. Their analysis was based on the assumption that the company would not change its prices for its three products as it entered 2023 . The analysis revealed important information that you needed to calculate product costs and other important measurements using the client's current product cost system. The results of that analysis are presented in the Existing worksheet in the Excel file provided. As you continued your discussion with the client personnel, you obtained additional information that you needed for your analysis and memo. 1) The company classifies 100% of its manufacturing overhead costs as foxed costs for both the Fabrication Department overhead and the Assembly Department overhead. 2) The company budgeted its Selling, General and Administrative costs at a total of $28,392,500. The company classifies $9,112,500 of this amount as variable costs and classifies the remaining $19,280,000 as fixed costs. 3) Even though the company budgeted an increase in production and sales of the Bel-Air model, it believes that it will experience unused capacity in all phases of its production process. The unused capacity will result from the anticipated decline in demand and sales of the Yogi Model and the Boo Boo model due to the company's inability to match the prices of its new competition. 4) The company budgeted an operating loss for 2023 based on its existing product cost system. Toward the end of the meeting, you gave the client personnel coples of the summary table of production activity that you prepared after your earlier meetings. You explained that you will use the information in the summary table as the basis for the new Activity-Based Costing System that you are planning for Nick's Woodworking Inc. You requested a follow up meeting as a group in which you hoped that you could work together to allocate the estimated overhead costs from the Fabricating Department and the Assembly Department to the production activities that you listed in your summary table. You hinted that you were confident that the new Activity-Based Cost System would result in more accurate product costs and that those costs would likely indicate that the company should make significant changes in the selling prices of its products. Everyone agreed to assist you in the process and a meeting time was set for the following day. Developing the New Activity-Based Costing System for Nick's Woodworking Inc.: When you arrived for your meeting the next day, you were amazed to learn that the controller, the production manager and the marketing manager worked through night on an analysis of budgeted production activities and related-costs using the classifications from your summary table. They actually completed an original version of the analysis early in the evening. However, when they looked over their results, they realized that, if they were correct, they could recommend that the company re-price its three products for 2023 . They felt their results demonstrated that the company could lower its prices of its two original products. Such actions would likely lead to an increase in demand for the products. The change in demand would require changes in sales projections and budgeted production activities and costs for 2023 . They therefore re-performed their entire analysis and prepared an adjusted budget for 2023 budget based on the following assumptions: 1) The company will lower the prices of the Yogi model and the Boo Boo model to match the competitors' prices. 2) The company will establish new selling prices for its products using its traditional pricing strategy. The company will preliminarily set the selling prices of its products at amounts equal to their unit costs as generated by the new Activity-Based Costing System and plus an 80% markup on their respective costs. The company will round its selling prices up to the nearest $5 increment. 3) The company will recover the market share that it lost relative to the Yogi and Boo Boo models because of the reduction in their prices. The company will therefore use its excess capacity to produce the additional goods required to meet the increased level of consumer demand. 4) The company will not change its projections of units of the Bel-Air model that it will produce and sell as demand for the product is not expected to increase above original projections. In addition, as indicated by the company's market research, demand for the Bel-Alr model will likely remain constant even if the company chooses to increase its selling price for 2023. 5) The unit cost of direct materials and direct labor for the three products will not be affected by the new accounting system and any changes in demand and production caused by the likely selling price adjustments. 6) The company continues to classify 100% of its manufacturing overhead costs as fixed costs. 7). The company will re-budget its Selling, General and Administrative costs to a total of $29,442,500. The company will classify $10,162,500 of this amount as variable costs and will classify the remaining $19,280,000 as fixed costs. The Proposed worksheet in the Excel file provided contains tables that were prepared for you by the controller, the production general manager and the marketing manager. The first table reflected the changes in demand, sales and production for the Yogi model and the Boo Boo model resulting from their lower reduced selling prices. The second table included the information that you requested for your analysis. The analysis re-allocated the Fabrication Department overhead and the Assembly Department overhead to the eight production activities that you listed in your production summary table )on page 10 above). In addition, the table was created to detail the total quantity of each production activity that three products were budgeted to use during 2023 . The table also included a column in which the total amount of the budgeted activity for 2023 was calculated for you. Background Information: Nick's Woodworking Inc. began operations in 2023 as a manufacturer of picnic tables with attached benches. During its first decade of operations, the company produced two styles of tables: the Yogi (deluxe) model and the Boo Boo (standard) model. The company was an overnight success as it found a strong market for its products among value-conscious consumers. Nick's Woodworking inc. Was able to place its products with leading retailers because of consumer demand as well as its reputation service-oriented trading partner. The company's cheesy marketing slogan, "Pick Nick's Tables", enhanced the company's reputation as a no-frills, no-nonsense supplier of high-quality products at reasonable prices. In early 2018, management decided that it needed to invest in a significant expansion and upgrade of its production facility. The project was completed by the end of 2018. Within months management realized that they over-built and therefore had excess production capacity. The excess capacity increased production costs of the company's products. At first, management decided to absorb the increased costs and therefore did not increase its selling prices. That choice resulted in a steady decline in the company's profits. Management was eventually forced to raise its prices during the last quarter of 2019 in an attempt to return its historical level of profitability. Consumer demand was relatively unaffected by the modest price increases; the company reported a higher level of profits for the first quarter of 2020 than it reported in any of the three previous quarters. Competing models still could not erode the company's market share and no new competing models were introduced during 2020. Management was pleased with the initial results of its actions, particularly because the company was unaffected by the pandemic and supply chain issues. However, it decided that the price increases were not the best solution to the excess capacity problem. Management felt that it should put the capacity to use by manufacturing a third product. Thus the company began developing a new product that would use the company's woodworking expertise. Management wanted the new product to complement the company's existing products by targeting consumers who would not normally be attracted to its traditional wooden picnic tables. Uitimately a more upscale table model was developed. The new table had a glass surface with a wooden base and attached benches. The table was designed to be constructed of a higher-quality wood than the Yogi and Boo Boo models. Nick's Woodworking Inc. unveiled its third product during the fourth quarter of 2021, marketing it as the Bel-Air model. During the planning process for 2022, the company revised its product costs to reflect the usage of the excess capacity costs by the Bel-Air model. The resulting estimated production costs for the Yogi model and the Boo Boo model were significantly lower than their estimated costs for 2021. The company decided to not reduce the selling prices of its all-wood tables at the outset of 2022 for two reasons. First, the market seemed to readily accept the 2021 price increases as demand for the product was steady as compared to the preceding years. Second, management wanted to be conservative in it pricing of its primary products just in case the Bel-Air model failed to meet expectations. Managemen feared that the anticipated cost reductions could fall short of expectations or fail to materialize completely Management did not want to face the prospect of needing to raise its prices within months of reducing them The manopement of Nick's Woodworking Inc. Was very pleased with the introduction of the Bel-Alir model. Retailers were receptive to stocking the product as they felt demand for the product would be strong given 2022 Eventst its unique style, quality construction and moderate pricing. Initial consumer demand actually exceeded Unfortunately the Bel-Air model presented a number of unexpected challenges. Nick's Woodworking Inc. expectations of both management and its retailers. had always produced 100% of its products. The company only relied on suppliers for its lumber and hardware supplies such as bolts and screws. However, for the Bel-Air model, the company needed an Management decided to outsource the fabrication of the table's glass surface. That decision resulted in a entirely new component piece, the glass top. couple of unforeseen consequences. The company was inadequately prepared in terms of lts personnel and its purchasing and production information systems to elfectively manage its supply-chain relationship with the glass fabricator and coordinate the production of the wood bases with the receipt of glass tops. Furthermore, the glass tops required special handing from the moment the pleces arrived from the glas5 fabricator until the fintshed tables were shipped to retailers. The company was therefore forced to add people, update its information systems and modify its materials and product handing systems. In the process, it significantly increased its overhead costs. At the end of both the first and second quarters of 2022, the controller, the production general manager, And the marketing manager met to analyze production costs. On both occasions they increased the company's. predetermined overhead rate that, in turn, increased the estimated unit costs to produce the company's three products. The increased overhead costs allocated to the Yogi and Boo Boo models essentially wiped out the anticipated cost savings from the Bel-Air model. By the end of the second quarter, the estimated production costs to produce the Yogl and the Boo Boo models were approximately equal to their 2021 production costs. Management was relieved that it had decided to not reduce the prices of the two models for 2022. Grven the unexpected strong demand for the Bel-Air model, management decided it could pass along the Givereases in the model's estimated production costs. It ralsed its price to retailers (and the suggested retail price to consumers) at the end of both quarters. Many retallers expressed concerns about the price increases: they feared the increases would adversely affect consumer demand. Those concerns turmed out to be-unfounded as third quarter sales of the Bel-Air model exceeded original projections as well as the actual sales of the model in each of the two previous quarters. During the third quarter of 2022, the management of Nick's Woodworking Inc. was troubled by a new development. Two well-established woodworking companies introduced their own models of one-piece, wooden picnic tables. Their tables were designed to directly compete with both the Yogi model and the Boo Boo model. The tables were similar in style and quality to Nick's Woodworking Inc.'s models. The competing tables prices were about 8 to 10%6 lower than the company's current prices. Once again, the controller, the production general manager and the marketing manager met to analyze production costs. They determined that their prior estimated production costs were accurate and therefore production costs. They determined that their prior cstimated production costs were accurate and therefori model and the Boo Boo model to meet the competitors' did not support a reduction in the prices of the Yogi mon concluded that the competitors had most likely underpriced their products in an attempt to prices. They con mer gain market share. Despite the company's recent production and cost is its production processes that it developed over timantages over its new competitors due to efficlencies in tors prod to raise their prices in relatively short period of time. As the third and fourth quarter of 2022 progressed, the competitors showed no signs of raising their prices. Weekly sales of the Yogi model and the Boo Boo model steadily decined to levels that were well below the sales of the products for the same weeks in preceding years. The compamy lost market share for the first time in its history. Meanwhile sales of the Bel-Alr model during this period steadily increased. However, the increase in sales of the Bel-Air model appeared to be insufficient to offset the decreases in sales of the other models. The company reported the lowest quarterly profit in its fourteen-year history during the third quarter of 2022 and it projected a small loss for the fourth quarter of the year. As the end of 2022 approached, the management of Nick's Woodworking inc. Was in crisis mode. Proposed Solutions: The production general manager organized a series of meetings of his production managers to discuss the company's recent cost and production problems and search for solutions to those problems. The production group quickly reached a consensus about the root cause of the problems and the course of action that the company should adopt to solve the problems. The production managers attributed the majority of the problems to the Bel-Air model. They therefore advocated dropping the Bel-Air model. They claimed that the Bel-Air model burdened the Yogi model and the Boo Boo model with increased production costs that, in turn, led to the company's inability to meet the prices of the new competing models. They also revealed that the Bel Air model was a constant source of production problems that frequently resulted in excess waste of materials and idie labor time. The production managers unveiled preliminary drawings and specifications for new, all-wooden tables in the tradition of the Yogi and Boo Boo models. The specifications for their proposed products were similar to the company's traditional products. The managers argued that the design similarities would lead to a reduction of overall production costs through the elimination of costs that were added specifically for the Bel-Air model. They provided cost and production estimates for the new products and analyses of their resulting effects on the costs of the Yogi model and the Boo Boo model. Based on the analyses, they concluded that the company would return to its former levels of profitability because it would be able to not oniy meet the prices of the new competitors but actually lower the prices of its existing products back to their early 2020 levels. The marketing managers also worked as a group to ferret out the key problems and issues and develop proposed solutions. They ultimately reached a set of very different conclusions from the production managers. They explained that the introduction of competing products into the marketplace was evidence that the market for the company's original products had matured. They maintained that consumers' tastes had changed to the point where the price had become more important to consumers than product quality. The marketing managers felt that to effectively compete in such a market the company could no longer view itself as a "no-frills, no nonsense supplier of high-quality products at reasonable prices." The company would need to fundamentally change itself and its mission and become a producer of "low-cost, marginalquality products." The marketing managers felt that such an extreme change was tll-advised. Instead, the marketing managers wanted the company to slowly withdraw from the all-wooden table market and shift its focus to the upscale market that the company successfully entered with its Bel-Air model. They argued for the development of new mixed-material products that would complement the Bel-Air model. To support their position, they presented market research studies that indicated the company could further increase the price of the Bel-Air model without affecting consumer demand. The research studies also provided evidence of an under-developed market for products similar to the Bel-Air model. By focusing on products for upscale consumers, Nick's Woodworking Inc. could continue its tradition as a supplier of highquality products at reasonable prices and return to its former levels of profitability. ABC Project Page 4 of 12 Uitimately, the two groups pitched their ldeas and arguments to the company's controller. As she listened to the presentations and reviewed the supporting documentation for the two wildly-opposite proposals, she became convinced that both arguments contained elements of truth that she needed to reconcile before she could recommend or reject elther proposal. She decided that she should write down her thoughts to ensure that she correctly understood the issues. Her notes read: Marketing Proposal 1) The marketing research relative to the Bel-Air model's pricing is the most compelling evidence in the proposal. 2) I analyzed the production costs of all of our products three times during the previous year and am satisfied that there were no errors or omissions in tracking and developing the production costs. 3) I interpret the market research results to mean that we set the price of the Bel-Air model too low despite the accuracy of the cost data produced by our accounting system. Production Proposal 1) I am equally fascinated with the production and cost analyses prepared by the production managers. 2) All of their assumptions and estimates are reasonable and their calculations are accurate. 3) I agree with their conclusions that the Yogi model and Boo Boo model could be produced at costs that would profitably support price decreases to their 2020 levels under two conditions: a) The Yogi and Boo Boo models cannot be burdened with the excess costs created by the Bel-Air model, and b) The Yogi and Boo Boo modeis cannot be burdened with the costs created by the old excess capacity. she finished writing the last note, she realized that the company's real problem might not be a marketing le or a production issue. The real problem might be an accounting issue. The marketing research cated that the Bel-Air model was underpriced yet product costs analyses indicated that it was not. fuction wanted to shift costs away from the Yogi model and the Boo Boo model by introducing new Jucts. However, maybe the costs could be shifted from the old models without developing entirely new lucts. Maybe the costs could be allocated to the Bel-Air model simply by changing the accounting em. If they could be shifted to the Bel-Air model then the resulting cost of the Bel-Air model would ort a higher price as suggested by the market research. finally, that is where you come in! will only make limited use of the information in the above narrative in this assignment. ever, you need to read the narrative carefully to be able to understand the typical business is that an Activity-Based Costing System addresses. I will be happy to answer any questions you might have about the facts presented in the narrative. You were hired as outside consultant(s) by Nick's Woodworking Inc. to analyze the company's existing product costing system and to recommend changes in that system. Your product in this assignment will be a memo to the controller of Nick's Woodworking Inc, that recommends changes to the company's current product cost system, product costs and the selling prices of its products. Your recommendations will focus on a switch from the company's traditional product costing system to an Activity-Based Costing System. Your report must include: 1) A one-page summary memo that includes: a) A one to two paragraph discussion that articulates your understanding of the problem that you were hired to address. b) A brief statement that identifies your recommendations relative to: i. changes in the company's product cost system ii. resulting changes in the production costs of the company's three products iii. new selling prices for the company's three products You may present your recommendations in bullet point format in the executive summary, and you may also include small tables. You should briefly present your recommendations in the executive summary without justifications and explanations. Normally a consultant would begin a memo to a client with a thorough discussion of the consultant's understanding of the client's problem. The consulting would then supply a general description of the work the consultant performed, the resources used and assumptions that were made. You SHOULD NOT include such discussions in your memo as you would merely be restating much of the background information and instructions that you received from me in this assignment handout. 2) You will begin your memo with a brief description of Nick's Woodworking Inc.'s current product cost system. As part of your discussion, you must include a table or a series of tables that clearly identify: a) The 2023 unit cost and selling price of each model based on the current product cost system. b) Projected 2023 sales in units and in total revenue for each model resulting from the costs and prices resulting from the current product system. c) The company's projected operating profit or loss for 2023 based on the current product cost system and other budgeted information. d) The company's annual breakeven point using the cost projections obtained from the current product cost system. Use the Existing worksheet in the Excel file provided to prepare these supporting calculations. ABC Project 3) You will then provide a brief description of your recommended changes in the product cost system used by Nick's Woodworking Inc. As part of your discussion, you must include brief justifications for these changes, You must also present a table or a serles of tobles that clearly identify: a) The 2023 unit cost and selling price of each model based on the new product cost system. b) Projected 2023 sales in units and in total revenue for each model resulting from the costs and prices resulting from the new product system. c) The company's projected operating profit or loss for 2023 based on the information derived from the new product cost system. d) The company's annual breakeven point using the cost projections obtained from the new product cost system. Use the Proposed worksheet in the Excel file provided to prepare these supporting calculations. 4) You will then provide a brief conclusion that identifies the effects of your recommended changes in the product cost system used by Nick's Woodworking Inc. You should identify and quantify, whenever possible, the benefits of the new system. You may use a bullet point format and/or tables in your discussion. As you read the details of the production process, you should attempt to identify at least one production activity that would be considered a "non-value added activity" that the company should attempt to eliminate. You should include a description of that activity and explain to the client why the client should attempt to eliminate that activity. Other Instructions/Requirements: Your memo must be typed. I would prefer double spaced lines so that I may have room to include my grading comments. I assume that your memo will need to be a minimum of four pages (including the executive summary) to minimally address the assignment requirements. You will present the required supporting calculations in the worksheet in the Excel file provided. You will upload your Excel file to Blackboard for my review. Please include at least one team member's name in the file name prior to uploading it to Blackboard. This assignment will be due Wednesday, April 5. arading Criteria: will grade your using the following criteria and weights. Nick's Woodworking Inc.'s Production Processt As part of your work, you met with the production managers including the general manger and the controller of Nick's Woodworking Inc. to obtain an understanding of the production process. As a group you developed a step-by-step description of the major activities that occur in the production process of the three products. Here is that description: 1) Customer orders are received and jobs are entered into production schedule. a) The company uses a job order cost system. Each customer order is produced as a separate job. b) Orders received for the Yogl model and the Boo Boo model generally average at 250 units per order. Each order requires approximately 1.0 hour of processing time. c) Orders received for the Bel-Air model generally average at 100 units per order. Each order requires approximately 1.5 hours of processing time. 2) Materials requirements are determined and materials are ordered. a) Wood is required for all three products. Generally one wood order is placed per job and one hour of purchasing time is used per wood order. b) Hardware supplies are periodically purchased in bulk using standing purchase orders with suppliers. Their order costs are considered to be negligible and will be ignored. b) Glass tops must be ordered for each Bel-Air job. Generally one glass top order is placed per job and three hours of purchasing time is used per order. 3) Materials arrive from the suppliers and are inspected and then moved to the appropriate department by the Inside Transportation Department. a) Wood requires. 25 inspection hours per order/job on arrival from the lumber mill and one handling per order/job is made by the Inside Transportation Department to bring the wood to the Fabrication Department. b) Hardware supplies require little, if any, inspection time. They are delivered directly to the Assembly Department area by the suppliers and therefore do not require handling by the Inside Transportation Department. c) Glass tops require 1.5 inspection hours per order/job on arrival and one handling per order/job is made by the Inside Transportation Department to bring the glass tops to the Assembly Department holding area. 4) The wood is fabricated (cut and shaped) in the Fabrication Department. a) 0.25 MH's per unit and 0.50 DLH's per unit are used for the Yogi model and the Boo Boo model in the Fabrication Department. b) 0.75 Mh's DLH per unit and 1.75 DLH's per unit are used for the Bel-Air model in the Fabrication Department. Page 9 of 12 5) The fabricated wood is sent to the Assembly Department. a) One handling per job is made by the Inside Transportation Department for all three products. 6) Glass tops are moved from the Assembly Department holding area into the Assembly Department. a) As the wood is moved into the Assembly Department, the glass tops must also be moved from the Assembly Department Holding area into the actual department. The glass tops are fragile. Thus one handling per job is made by the Inside Transportation Department on each Bel-Air job. 7) Products are assembled in the Assembly Department. a) 0.5 DLH per unit is used for the Yogi model and the Boo Boo model in the Assembly Department b) 0.75DL per unit is used for the Bel-Air model in the Assembly Department. 8) Products are inspected and any defects are corrected before goods leave the Assembly Department. a) .50 inspection hours per job are required for the Yogi model and the Boo Boo model. b) 1.50 inspection hours per job are required for the Bel-Air model. 9) Goods are moved from Assembly Department and are prepared for shipment: a) One handling per job is made by the Inside Transportation Department to move the Yogi model and the Boo Boo model out of the Assembly Department and into Shipping; .10 preparation hour per unit is used to prepare these products for shipment b) Two handlings per job are made by the Inside Transportation Department relative to the Bel-Air model. The first handling is required to move the Bel-Air model from the Assembly Department to a separate area for shipment preparation. . 25 preparation hours per unit are used to prepare the Bel-Air model for shipment. The second handling is then made by the Inside Transportation Department to transfer the prepared goods to Shipping. ABC Project Based on tha ahave descriotion of the production process, you prepored the following summary table: Based on the above description and summary chart, you started to develop a sense that Nick's Woodworking Inc. was a prime candidate for an Activity-Based Costing System. You realized that you had just collected important information that you needed to establish cost pools and calculate the activity rates that would be used to re-allocate production costs to the three products. Nick Woodworking Inc.'s Existing Product Cost System: Your next step was to meet with the controller, the production general manager and the marketing manager to review the existing product cost system and to obtain the cost information that you needed to establish cost pools and to re-calculate product costs. The controller explained that the company uses a job order cost system in which it accumulates actual direct materials and direct labor costs as they are added to each job in the Fabrication Department and the Assembly Department. The company uses a separate predetermined overhead rate to allocate overhead used by each department. Machine hours are used to allocate overhead in the Fabrication Department; direct labor hours are used to allocate overhead in the Assembly Department. Once the company estimates the total unit costs of its products, it sets their selling prices at amounts equal to their unit costs plus an B0\% markup on their respective costs. The company rounds its selling prices up to the nearest $5 increment. mu5, if the company determined that a product had a unit cost (including materials, labor and overhead) of $130; it would add an 80% markup or $104 to that cost to arrive at a preliminary selling price of $234 per unit. The company would then round that price up to the nearest $5 increment and would therefore charge $235 for the product. The controller handed to you an analysis of product demand, production activity and expected product costs that she had prepared with assistance from the marketing manager and the production general manager. Their analysis was based on the assumption that the company would not change its prices for its three products as it entered 2023 . The analysis revealed important information that you needed to calculate product costs and other important measurements using the client's current product cost system. The results of that analysis are presented in the Existing worksheet in the Excel file provided. As you continued your discussion with the client personnel, you obtained additional information that you needed for your analysis and memo. 1) The company classifies 100% of its manufacturing overhead costs as foxed costs for both the Fabrication Department overhead and the Assembly Department overhead. 2) The company budgeted its Selling, General and Administrative costs at a total of $28,392,500. The company classifies $9,112,500 of this amount as variable costs and classifies the remaining $19,280,000 as fixed costs. 3) Even though the company budgeted an increase in production and sales of the Bel-Air model, it believes that it will experience unused capacity in all phases of its production process. The unused capacity will result from the anticipated decline in demand and sales of the Yogi Model and the Boo Boo model due to the company's inability to match the prices of its new competition. 4) The company budgeted an operating loss for 2023 based on its existing product cost system. Toward the end of the meeting, you gave the client personnel coples of the summary table of production activity that you prepared after your earlier meetings. You explained that you will use the information in the summary table as the basis for the new Activity-Based Costing System that you are planning for Nick's Woodworking Inc. You requested a follow up meeting as a group in which you hoped that you could work together to allocate the estimated overhead costs from the Fabricating Department and the Assembly Department to the production activities that you listed in your summary table. You hinted that you were confident that the new Activity-Based Cost System would result in more accurate product costs and that those costs would likely indicate that the company should make significant changes in the selling prices of its products. Everyone agreed to assist you in the process and a meeting time was set for the following day. Developing the New Activity-Based Costing System for Nick's Woodworking Inc.: When you arrived for your meeting the next day, you were amazed to learn that the controller, the production manager and the marketing manager worked through night on an analysis of budgeted production activities and related-costs using the classifications from your summary table. They actually completed an original version of the analysis early in the evening. However, when they looked over their results, they realized that, if they were correct, they could recommend that the company re-price its three products for 2023 . They felt their results demonstrated that the company could lower its prices of its two original products. Such actions would likely lead to an increase in demand for the products. The change in demand would require changes in sales projections and budgeted production activities and costs for 2023 . They therefore re-performed their entire analysis and prepared an adjusted budget for 2023 budget based on the following assumptions: 1) The company will lower the prices of the Yogi model and the Boo Boo model to match the competitors' prices. 2) The company will establish new selling prices for its products using its traditional pricing strategy. The company will preliminarily set the selling prices of its products at amounts equal to their unit costs as generated by the new Activity-Based Costing System and plus an 80% markup on their respective costs. The company will round its selling prices up to the nearest $5 increment. 3) The company will recover the market share that it lost relative to the Yogi and Boo Boo models because of the reduction in their prices. The company will therefore use its excess capacity to produce the additional goods required to meet the increased level of consumer demand. 4) The company will not change its projections of units of the Bel-Air model that it will produce and sell as demand for the product is not expected to increase above original projections. In addition, as indicated by the company's market research, demand for the Bel-Alr model will likely remain constant even if the company chooses to increase its selling price for 2023. 5) The unit cost of direct materials and direct labor for the three products will not be affected by the new accounting system and any changes in demand and production caused by the likely selling price adjustments. 6) The company continues to classify 100% of its manufacturing overhead costs as fixed costs. 7). The company will re-budget its Selling, General and Administrative costs to a total of $29,442,500. The company will classify $10,162,500 of this amount as variable costs and will classify the remaining $19,280,000 as fixed costs. The Proposed worksheet in the Excel file provided contains tables that were prepared for you by the controller, the production general manager and the marketing manager. The first table reflected the changes in demand, sales and production for the Yogi model and the Boo Boo model resulting from their lower reduced selling prices. The second table included the information that you requested for your analysis. The analysis re-allocated the Fabrication Department overhead and the Assembly Department overhead to the eight production activities that you listed in your production summary table )on page 10 above). In addition, the table was created to detail the total quantity of each production activity that three products were budgeted to use during 2023 . The table also included a column in which the total amount of the budgete

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts