Answered step by step

Verified Expert Solution

Question

1 Approved Answer

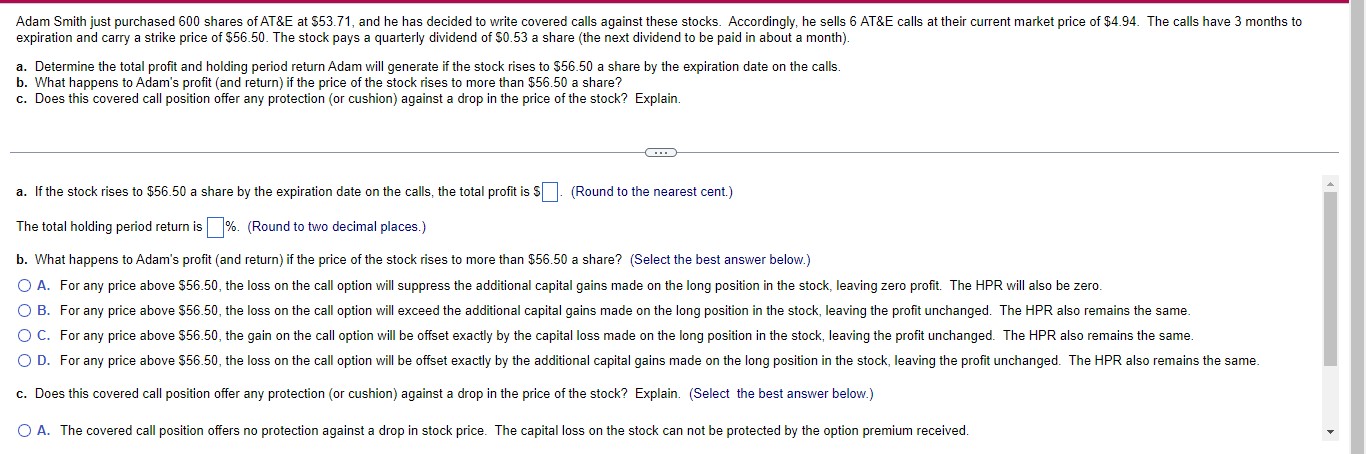

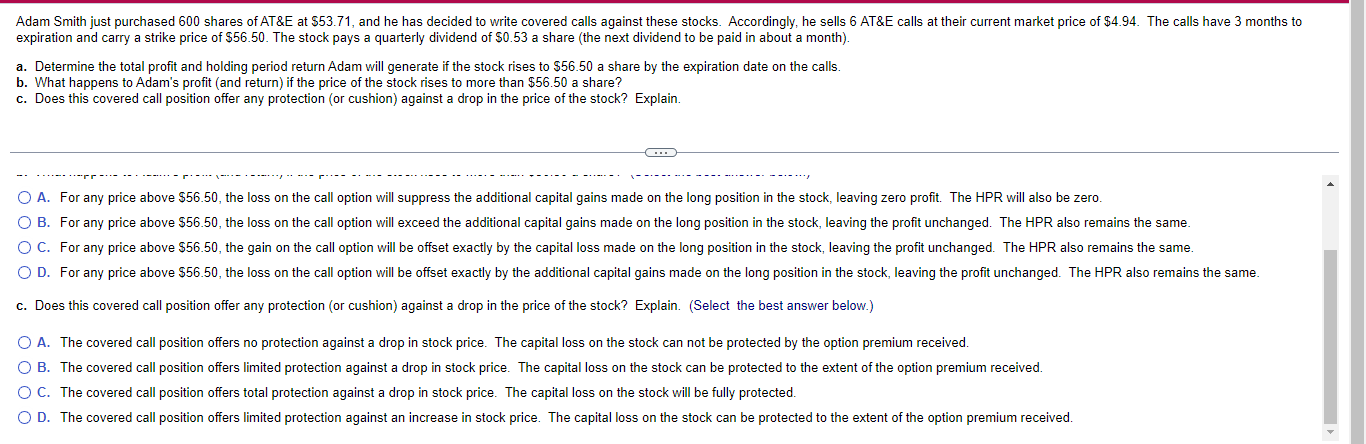

Adam Smith just purchased 600 shares of AT&E at $53.71, and he has decided to write covered calls against these stocks. Accordingly, he sells

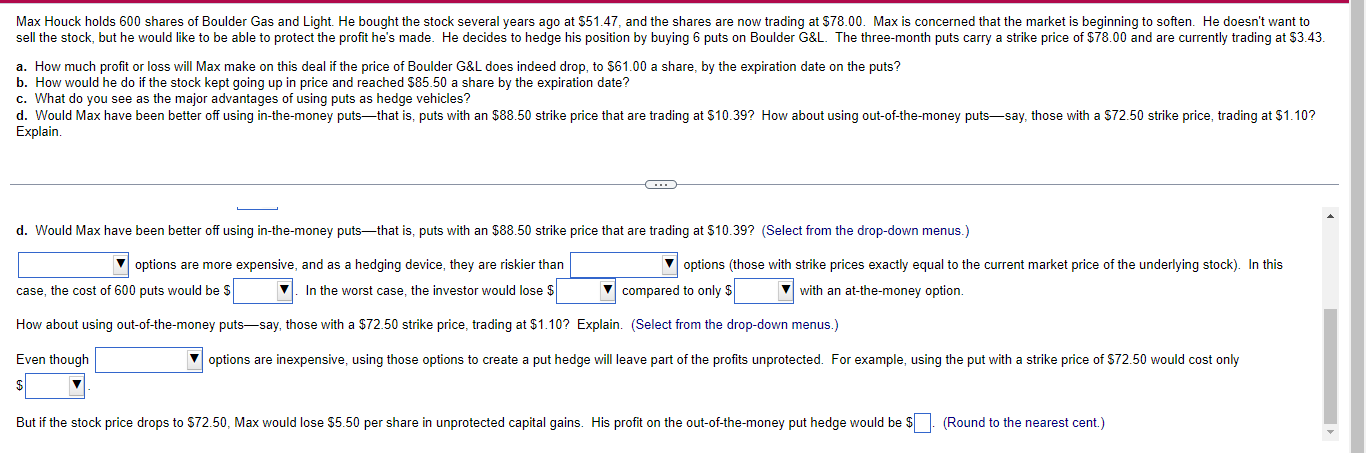

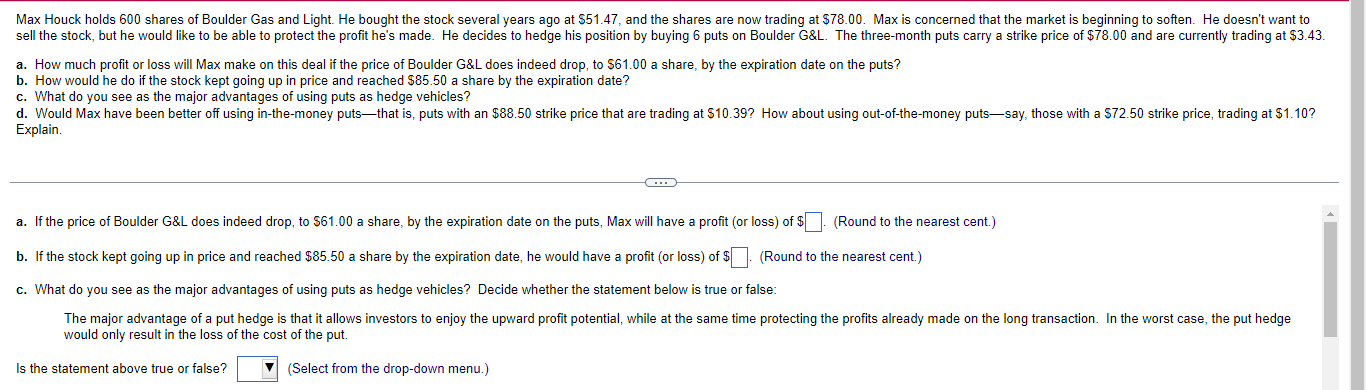

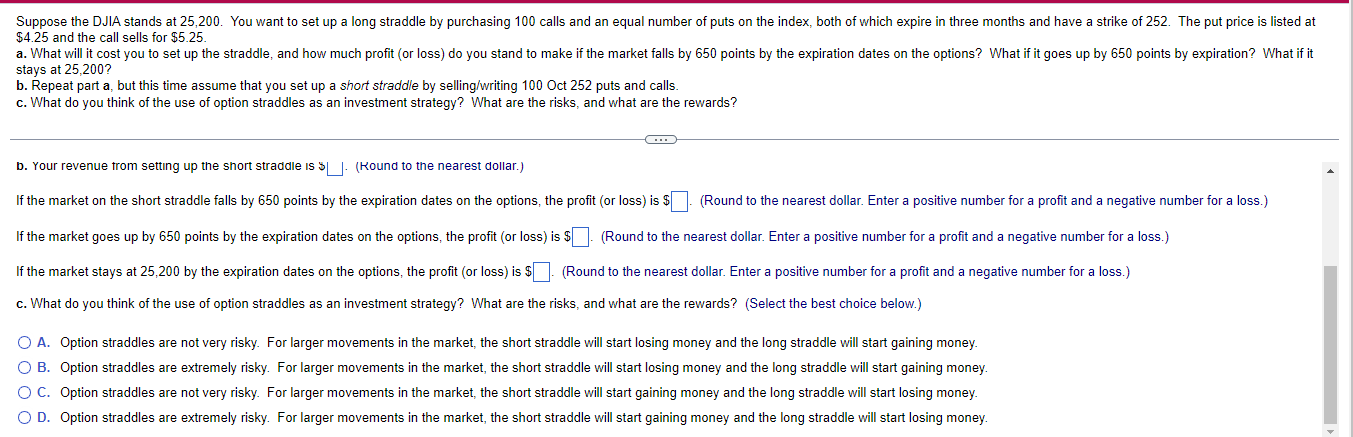

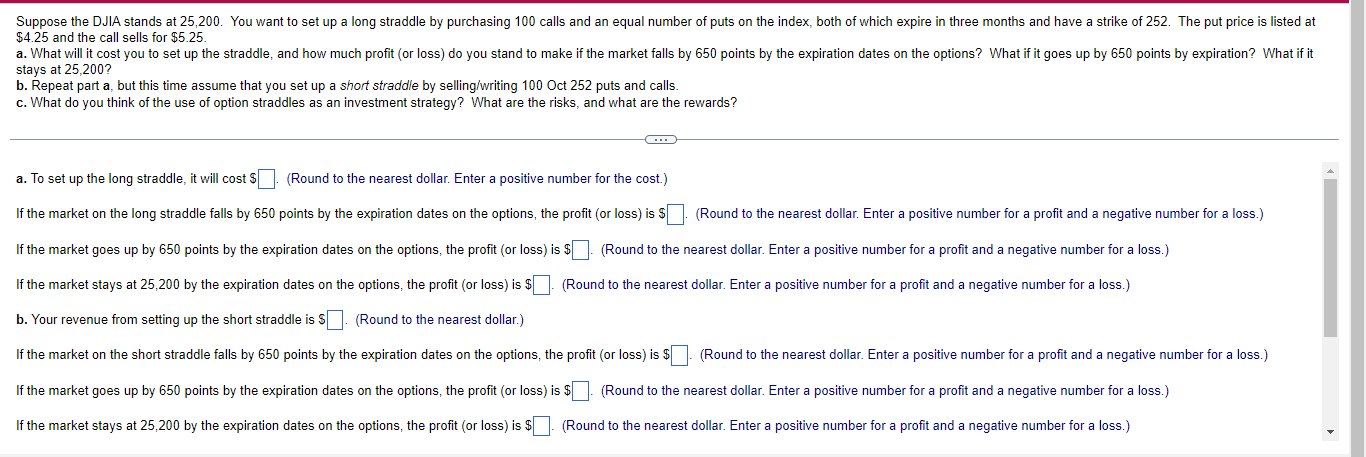

Adam Smith just purchased 600 shares of AT&E at $53.71, and he has decided to write covered calls against these stocks. Accordingly, he sells 6 AT&E calls at their current market price of $4.94. The calls have 3 months to expiration and carry a strike price of $56.50. The stock pays a quarterly dividend of $0.53 a share (the next dividend to be paid in about a month). a. Determine the total profit and holding period return Adam will generate if the stock rises to $56.50 a share by the expiration date on the calls. b. What happens to Adam's profit (and return) if the price of the stock rises to more than $56.50 a share? c. Does this covered call position offer any protection (or cushion) against a drop in the price of the stock? Explain. C a. If the stock rises to $56.50 a share by the expiration date on the calls, the total profit is $. (Round to the nearest cent.) The total holding period return is %. (Round to two decimal places.) b. What happens to Adam's profit (and return) if the price of the stock rises to more than $56.50 a share? (Select the best answer below.) O A. For any price above $56.50, the loss on the call option will suppress the additional capital gains made on the long position in the stock, leaving zero profit. The HPR will also be zero. O B. For any price above $56.50, the loss on the call option will exceed the additional capital gains made on the long position in the stock, leaving the profit unchanged. The HPR also remains the same. O C. For any price above $56.50, the gain on the call option will be offset exactly by the capital loss made on the long position in the stock, leaving the profit unchanged. The HPR also remains the same. O D. For any price above $56.50, the loss on the call option will be offset exactly by the additional capital gains made on the long position in the stock, leaving the profit unchanged. The HPR also remains the same. c. Does this covered call position offer any protection (or cushion) against a drop in the price of the stock? Explain. (Select the best answer below.) O A. The covered call position offers no protection against a drop in stock price. The capital loss on the stock can not be protected by the option premium received. Adam Smith just purchased 600 shares of AT&E at $53.71, and he has decided to write covered calls against these stocks. Accordingly, he sells 6 AT&E calls at their current market price of $4.94. The calls have 3 months to expiration and carry a strike price of $56.50. The stock pays a quarterly dividend of $0.53 a share (the next dividend to be paid in about a month). a. Determine the total profit and holding period return Adam will generate if the stock rises to $56.50 a share by the expiration date on the calls. b. What happens to Adam's profit (and return) if the price of the stock rises to more than $56.50 a share? c. Does this covered call position offer any protection (or cushion) against a drop in the price of the stock? Explain. C O A. For any price above $56.50, the loss on the call option will suppress the additional capital gains made on the long position in the stock, leaving zero profit. The HPR will also be zero. O B. For any price above $56.50, the loss on the call option will exceed the additional capital gains made on the long position in the stock, leaving the profit unchanged. The HPR also remains the same. O C. For any price above $56.50, the gain on the call option will be offset exactly by the capital loss made on the long position in the stock, leaving the profit unchanged. The HPR also remains the same. O D. For any price above $56.50, the loss on the call option will be offset exactly by the additional capital gains made on the long position in the stock, leaving the profit unchanged. The HPR also remains the same. c. Does this covered call position offer any protection (or cushion) against a drop in the price of the stock? Explain. (Select the best answer below.) O A. The covered call position offers no protection against a drop in stock price. The capital loss on the stock can not be protected by the option premium received. O B. The covered call position offers limited protection against a drop in stock price. The capital loss on the stock can be protected to the extent of the option premium received. O C. The covered call position offers total protection against a drop in stock price. The capital loss on the stock will be fully protected. O D. The covered call position offers limited protection against an increase in stock price. The capital loss on the stock can be protected to the extent of the option premium received. Max Houck holds 600 shares of Boulder Gas and Light. He bought the stock several years ago at $51.47, and the shares are now trading at $78.00. Max is concerned that the market is beginning to soften. He doesn't want to sell the stock, but he would like to be able to protect the profit he's made. He decides to hedge his position by buying 6 puts on Boulder G&L. The three-month puts carry a strike price of $78.00 and are currently trading at $3.43. a. How much profit or loss will Max make on this deal if the price of Boulder G&L does indeed drop, to $61.00 a share, by the expiration date on the puts? b. How would he do if the stock kept going up in price and reached $85.50 a share by the expiration date? c. What do you see as the major advantages of using puts as hedge vehicles? d. Would Max have been better off using in-the-money puts-that is, puts with an $88.50 strike price that are trading at $10.39? How about using out-of-the-money puts-say, those with a $72.50 strike price, trading at $1.10? Explain. C d. Would Max have been better off using in-the-money puts-that is, puts with an $88.50 strike price that are trading at $10.39? (Select from the drop-down menus.) options are more expensive, and as a hedging device, they are riskier than In the worst case, the investor would lose $ case, the cost of 600 puts would be $ How about using out-of-the-money puts-say, those with a $72.50 strike price, trading at $1.10? Explain. (Select from the drop-down menus.) Even though options (those with strike prices exactly equal to the current market price of the underlying stock). In this compared to only $ with an at-the-money option. options are inexpensive, using those options to create a put hedge will leave part of the profits unprotected. For example, using the put with a strike price of $72.50 would cost only But if the stock price drops to $72.50, Max would lose $5.50 per share in unprotected capital gains. His profit on the out-of-the-money put hedge would be $. (Round to the nearest cent.) Max Houck holds 600 shares of Boulder Gas and Light. He bought the stock several years ago at $51.47, and the shares are now trading at $78.00. Max is concerned that the market is beginning to soften. He doesn't want to sell the stock, but he would like to be able to protect the profit he's made. He decides to hedge his position by buying 6 puts on Boulder G&L. The three-month puts carry a strike price of $78.00 and are currently trading at $3.43. a. How much profit or loss will Max make on this deal if the price of Boulder G&L does indeed drop, to $61.00 a share, by the expiration date on the puts? b. How would he do if the stock kept going up in price and reached $85.50 a share by the expiration date? c. What do you see as the major advantages of using puts as hedge vehicles? d. Would Max have been better off using in-the-money puts-that is, puts with an $88.50 strike price that are trading at $10.39? How about using out-of-the-money puts-say, those with a $72.50 strike price, trading at $1.10? Explain. G a. If the price of Boulder G&L does indeed drop, to $61.00 a share, by the expiration date on the puts, Max will have a profit (or loss) of $. (Round to the nearest cent.) b. If the stock kept going up in price and reached $85.50 a share by the expiration date, he would have a profit (or loss) of $ (Round to the nearest cent.) c. What do you see as the major advantages of using puts as hedge vehicles? Decide whether the statement below is true or false: The major advantage of a put hedge is that it allows investors to enjoy the upward profit potential, while at the same time protecting the profits already made on the long transaction. In the worst case, the put hedge would only result in the loss of the cost of the put. Is the statement above true or false? (Select from the drop-down menu.) Suppose the DJIA stands at 25,200. You want to set up a long straddle by purchasing 100 calls and an equal number of puts on the index, both of which expire in three months and have a strike of 252. The put price is listed at $4.25 and the call sells for $5.25. a. What will it cost you to set up the straddle, and how much profit (or loss) do you stand to make if the market falls by 650 points by the expiration dates on the options? What if it goes up by 650 points by expiration? What if it stays at 25,200? b. Repeat part a, but this time assume that you set up a short straddle by selling/writing 100 Oct 252 puts and calls. c. What do you think of the use of option straddles as an investment strategy? What are the risks, and what are the rewards? C b. Your revenue from setting up the short straddle is $. (Kound to the nearest dollar.) If the market on the short straddle falls by 650 points by the expiration dates on the options, the profit (or loss) is $ If the market goes up by 650 points by the expiration dates on the options, the profit (or loss) is $ (Round to the nearest dollar. Enter a positive number for a profit and a negative number for a loss.) If the market stays at 25,200 by the expiration dates on the options, the profit (or loss) is $. (Round to the nearest dollar. Enter a positive number for a profit and a negative number for a loss.) c. What do you think of the use of option straddles as an investment strategy? What are the risks, and what are the rewards? (Select the best choice below.) (Round to the nearest dollar. Enter a positive number for a profit and a negative number for a loss.) O A. Option straddles are not very risky. For larger movements in the market, the short straddle will start losing money and the long straddle will start gaining money. O B. Option straddles are extremely risky. For larger movements in the market, the short straddle will start losing money and the long straddle will start gaining money. C. Option straddles are not very risky. For larger movements in the market, the short straddle will start gaining money and the long straddle will start losing money. O D. Option straddles are extremely risky. For larger movements in the market, the short straddle will start gaining money and the long straddle will start losing money. Suppose the DJIA stands at 25,200. You want to set up a long straddle by purchasing 100 calls and an equal number of puts on the index, both of which expire in three months and have a strike of 252. The put price is listed at $4.25 and the call sells for $5.25. a. What will it cost you to set up the straddle, and how much profit (or loss) do you stand to make if the market falls by 650 points by the expiration dates on the options? What if it goes up by 650 points by expiration? What if it stays at 25,200? b. Repeat part a, but this time assume that you set up a short straddle by selling/writing 100 Oct 252 puts and calls. c. What do you think of the use of option straddles as an investment strategy? What are the risks, and what are the rewards? a. To set up the long straddle, it will cost $. (Round to the nearest dollar. Enter a positive number for the cost.) If the market on the long straddle falls by 650 points by the expiration dates on the options, the profit (or loss) is $ (Round to the nearest dollar. Enter a positive number for a profit and a negative number for a loss.) If the market goes up by 650 points by the expiration dates on the options, the profit (or loss) is $. (Round to the nearest dollar. Enter a positive number for a profit and a negative number for a loss.) If the market stays at 25,200 by the expiration dates on the options, the profit (or loss) is $. (Round to the nearest dollar. Enter a positive number for a profit and a negative number for a loss.) b. Your revenue from setting up the short straddle is $. (Round to the nearest dollar.) If the market on the short straddle falls by 650 points by the expiration dates on the options, the profit (or loss) is $. (Round to the nearest dollar. Enter a positive number for a profit and a negative number for a loss.) If the market goes up by 650 points by the expiration dates on the options, the profit (or loss) is $. (Round to the nearest dollar. Enter a positive number for a profit and a negative number for a loss.) If the market stays at 25,200 by the expiration dates on the options, the profit (or loss) is $. (Round to the nearest dollar. Enter a positive number for a profit and a negative number for a loss.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

The detailed answer for the above question is provided below a To calculate the total profit and hol...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Investing

Authors: Scott B. Smart, Lawrence J. Gitman, Michael D. Joehnk

12th edition

978-0133075403, 133075354, 9780133423938, 133075400, 013342393X, 978-0133075359