Answered step by step

Verified Expert Solution

Question

1 Approved Answer

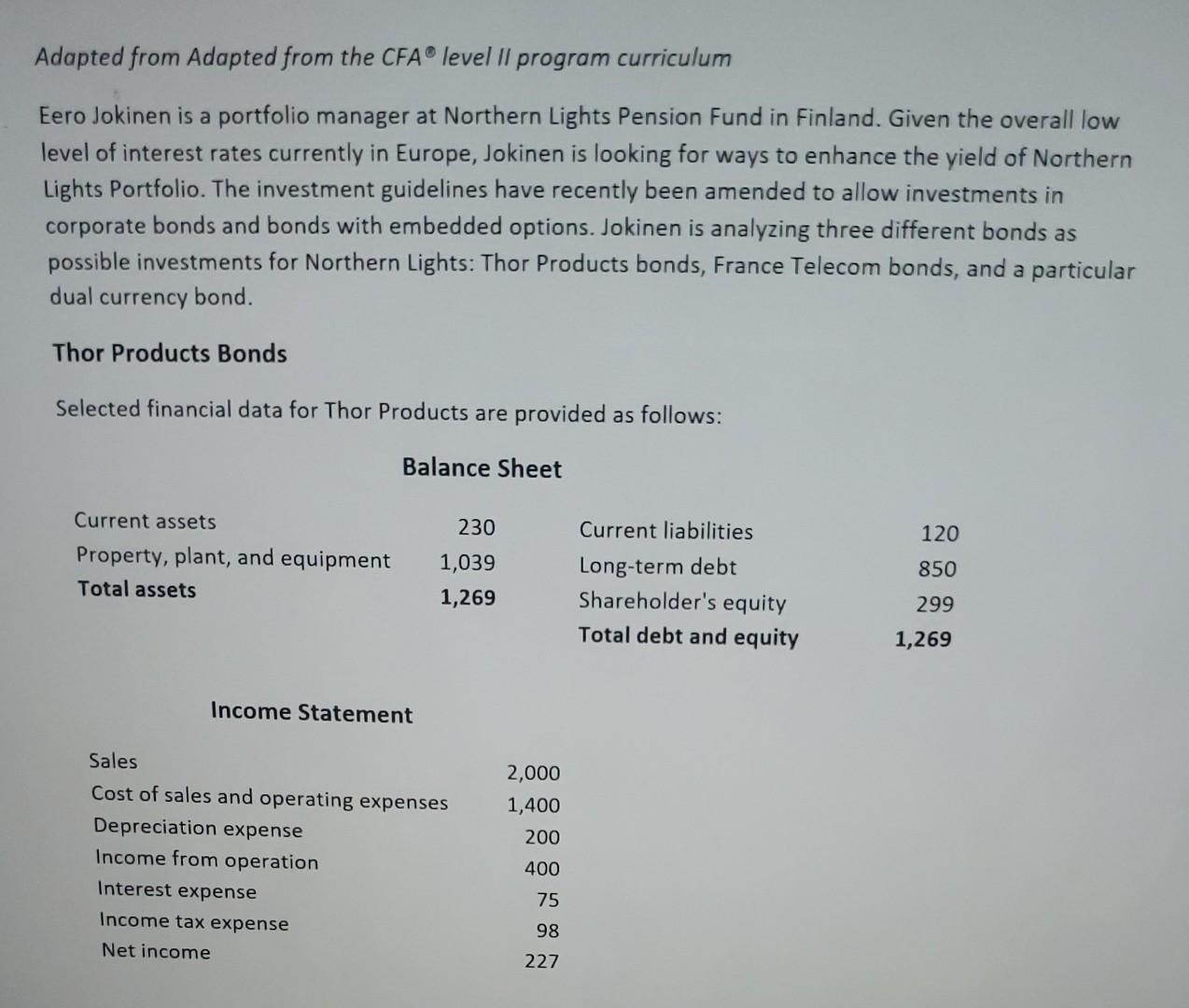

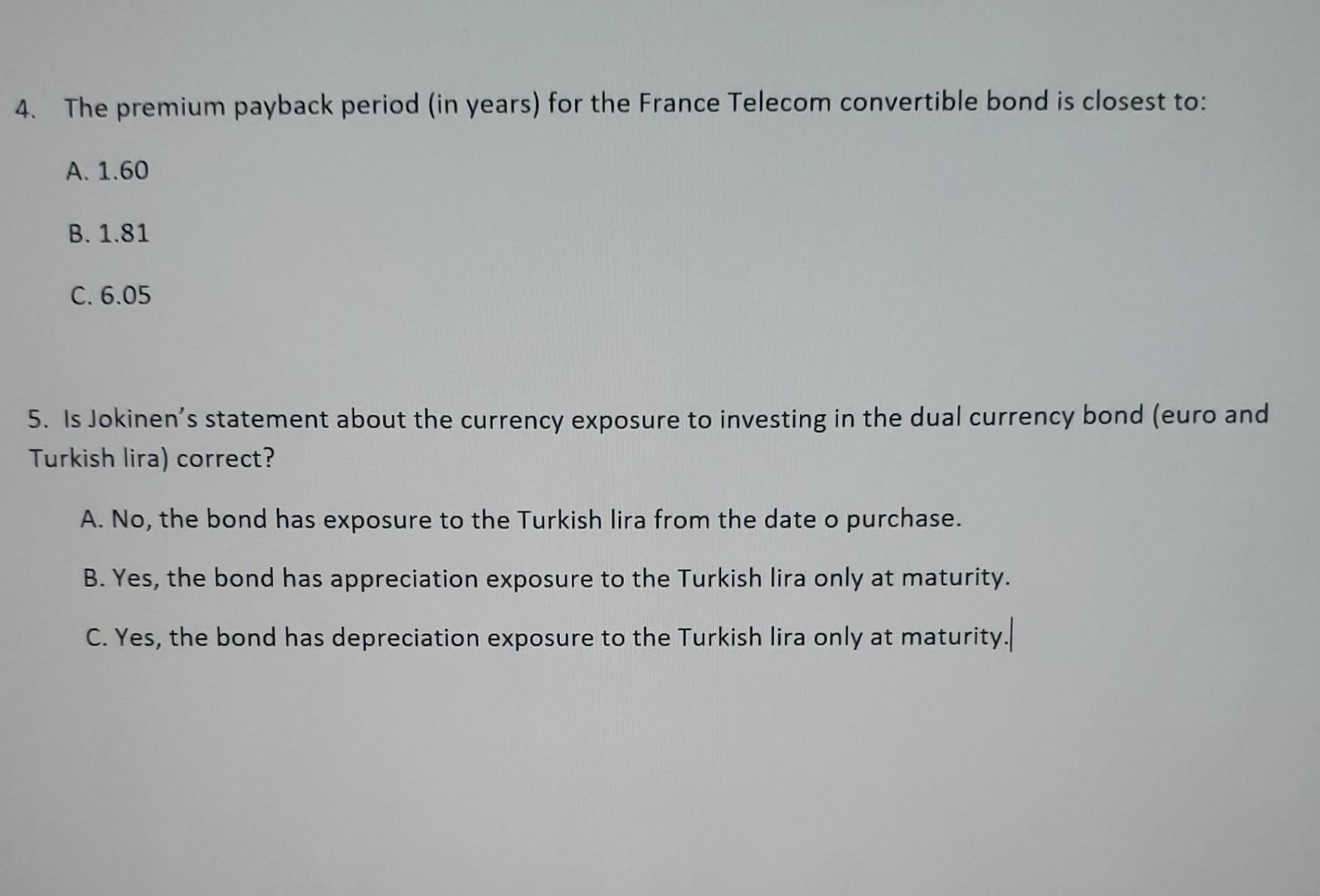

Adapted from Adapted from the CFA level Il program curriculum Eero Jokinen is a portfolio manager at Northern Lights Pension Fund in Finland. Given the

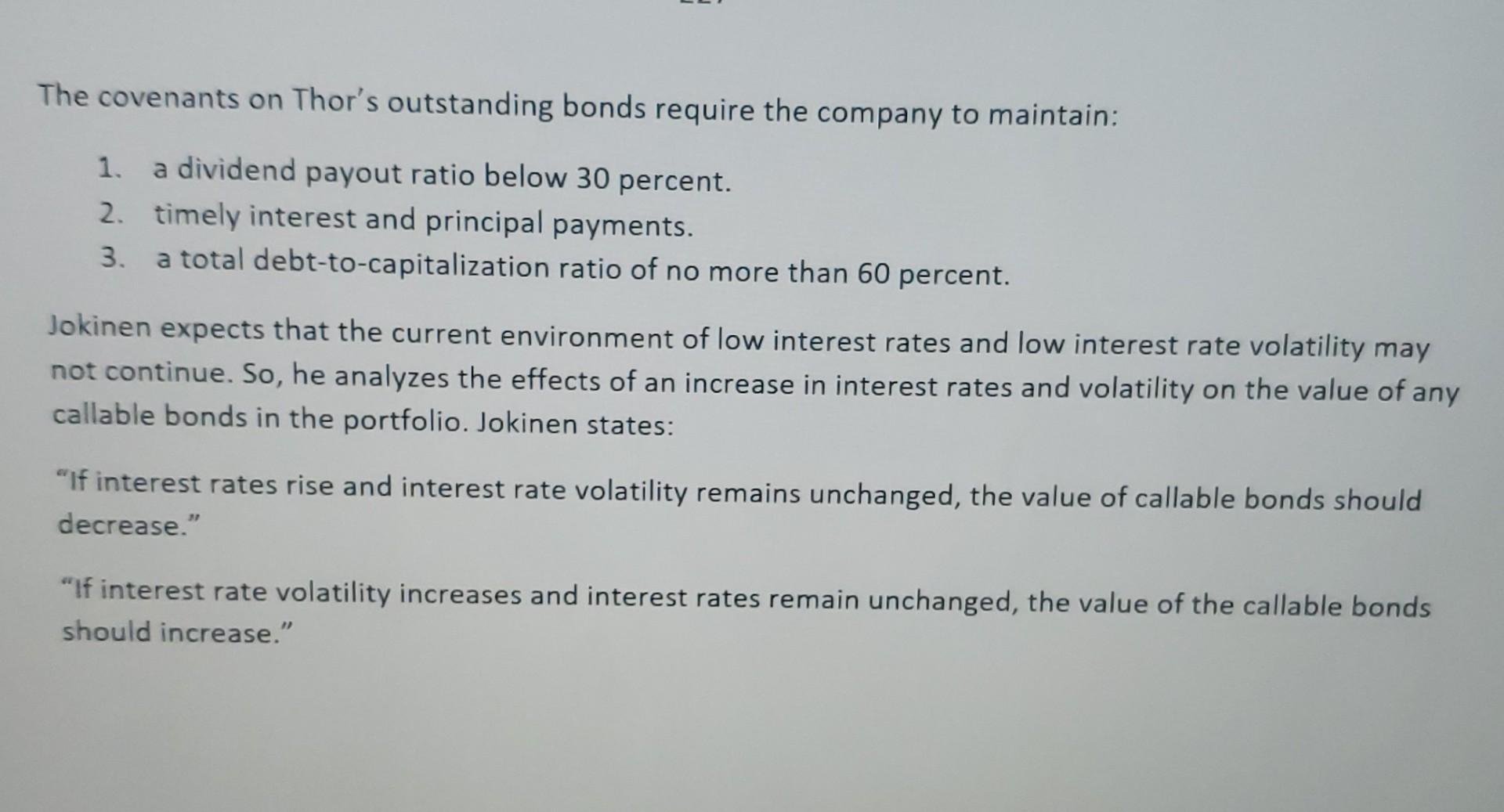

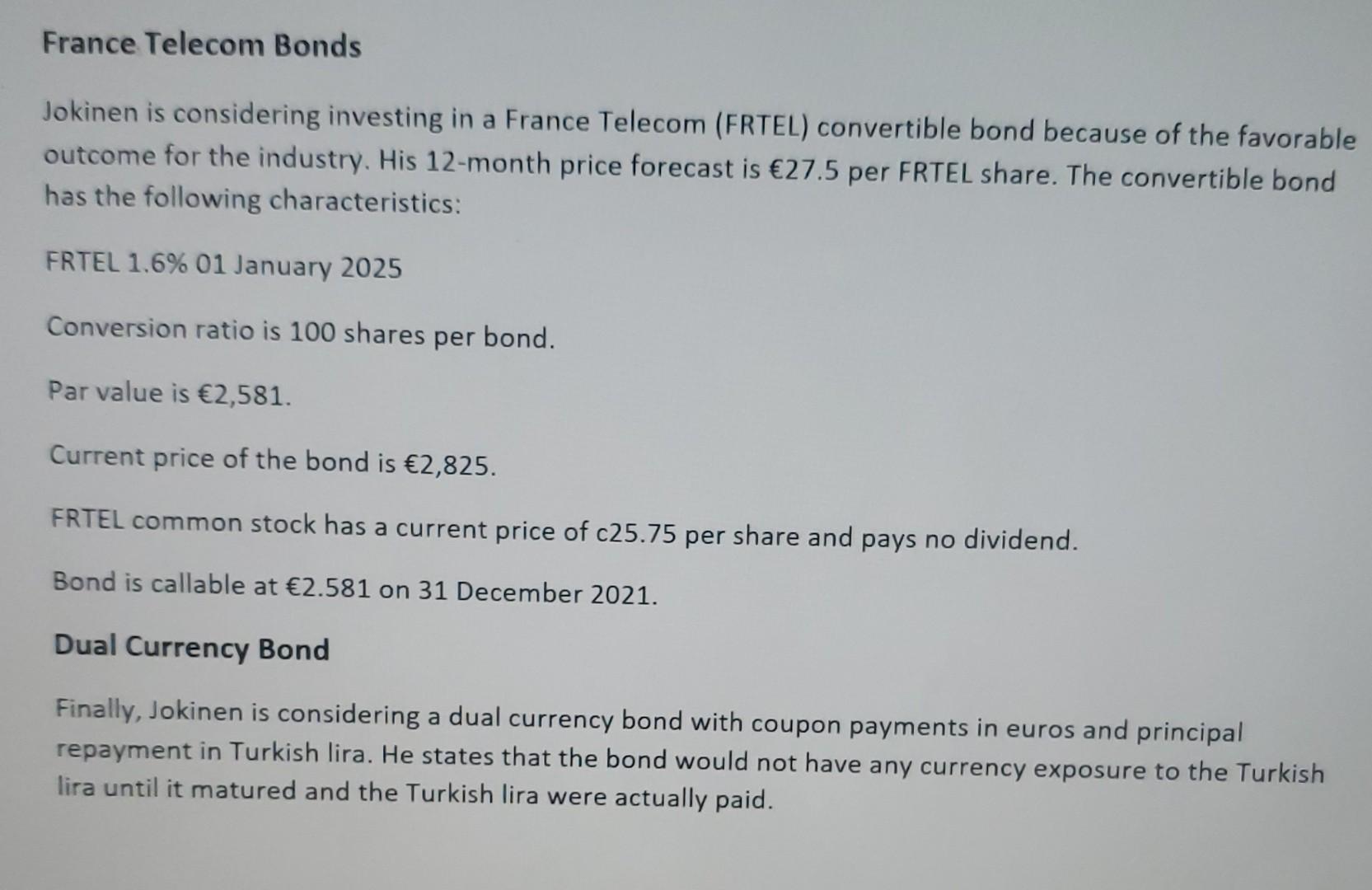

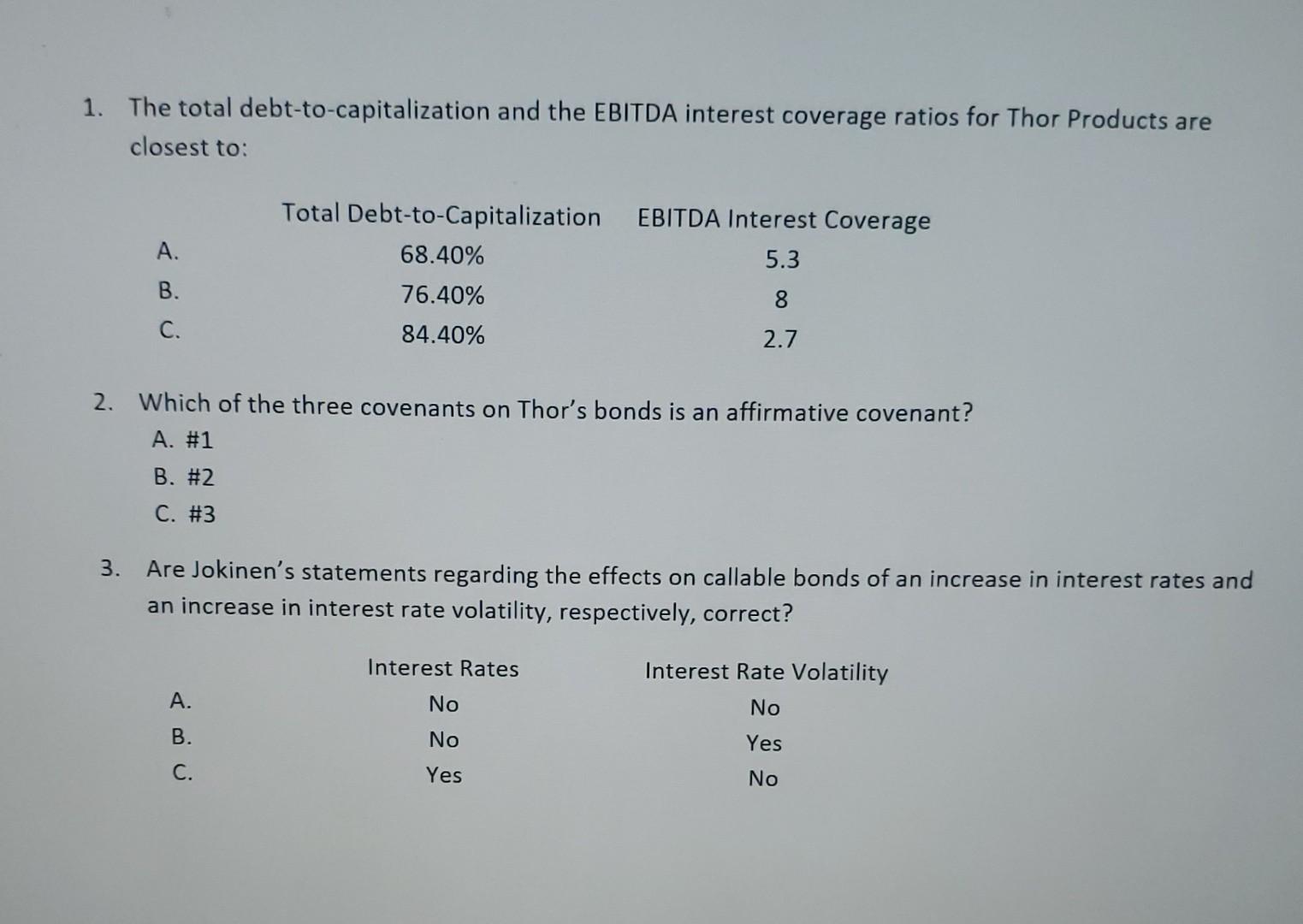

Adapted from Adapted from the CFA level Il program curriculum Eero Jokinen is a portfolio manager at Northern Lights Pension Fund in Finland. Given the overall low level of interest rates currently in Europe, Jokinen is looking for ways to enhance the yield of Northern Lights Portfolio. The investment guidelines have recently been amended to allow investments in corporate bonds and bonds with embedded options. Jokinen is analyzing three different bonds as possible investments for Northern Lights: Thor Products bonds, France Telecom bonds, and a particular dual currency bond. Thor Products Bonds Selected financial data for Thor Products are provided as follows: Balance Sheet 120 Current assets Property, plant, and equipment Total assets 230 1,039 1,269 850 Current liabilities Long-term debt Shareholder's equity Total debt and equity 299 1,269 Income Statement 2,000 1,400 200 Sales Cost of sales and operating expenses Depreciation expense Income from operation Interest expense Income tax expense Net income 400 75 98 227 The covenants on Thor's outstanding bonds require the company to maintain: 1. a dividend payout ratio below 30 percent. 2. timely interest and principal payments. 3. a total debt-to-capitalization ratio of no more than 60 percent. Jokinen expects that the current environment of low interest rates and low interest rate volatility may not continue. So, he analyzes the effects of an increase in interest rates and volatility on the value of any callable bonds in the portfolio. Jokinen states: "If interest rates rise and interest rate volatility remains unchanged, the value of callable bonds should decrease." "If interest rate volatility increases and interest rates remain unchanged, the value of the callable bonds should increase." France Telecom Bonds Jokinen is considering investing in a France Telecom (FRTEL) convertible bond because of the favorable outcome for the industry. His 12-month price forecast is 27.5 per FRTEL share. The convertible bond has the following characteristics: FRTEL 1.6% 01 January 2025 Conversion ratio is 100 shares per bond. Par value is 2,581. Current price of the bond is 2,825. FRTEL common stock has current price of c25.75 per share and pays no dividend. Bond is callable at 2.581 on 31 December 2021. Dual Currency Bond Finally, Jokinen is considering a dual currency bond with coupon payments in euros and principal repayment in Turkish lira. He states that the bond would not have any currency exposure to the Turkish lira until it matured and the Turkish lira were actually paid. 1. The total debt-to-capitalization and the EBITDA interest coverage ratios for Thor Products are closest to: EBITDA Interest Coverage 5.3 4 Total Debt-to-Capitalization 68.40% 76.40% 84.40% B. 8 C. 2.7 2. Which of the three covenants on Thor's bonds is an affirmative covenant? A. #1 B. #2 C. #3 3. Are Jokinen's statements regarding the effects on callable bonds of an increase in interest rates and an increase in interest rate volatility, respectively, correct? Interest Rates No A. Interest Rate Volatility No Yes B. No Yes C. No 4. The premium payback period (in years) for the France Telecom convertible bond is closest to: A. 1.60 B. 1.81 C. 6.05 5. Is Jokinen's statement about the currency exposure to investing in the dual currency bond (euro and Turkish lira) correct? A. No, the bond has exposure to the Turkish lira from the date o purchase. B. Yes, the bond has appreciation exposure to the Turkish lira only at maturity. C. Yes, the bond has depreciation exposure to the Turkish lira only at maturity. Adapted from Adapted from the CFA level Il program curriculum Eero Jokinen is a portfolio manager at Northern Lights Pension Fund in Finland. Given the overall low level of interest rates currently in Europe, Jokinen is looking for ways to enhance the yield of Northern Lights Portfolio. The investment guidelines have recently been amended to allow investments in corporate bonds and bonds with embedded options. Jokinen is analyzing three different bonds as possible investments for Northern Lights: Thor Products bonds, France Telecom bonds, and a particular dual currency bond. Thor Products Bonds Selected financial data for Thor Products are provided as follows: Balance Sheet 120 Current assets Property, plant, and equipment Total assets 230 1,039 1,269 850 Current liabilities Long-term debt Shareholder's equity Total debt and equity 299 1,269 Income Statement 2,000 1,400 200 Sales Cost of sales and operating expenses Depreciation expense Income from operation Interest expense Income tax expense Net income 400 75 98 227 The covenants on Thor's outstanding bonds require the company to maintain: 1. a dividend payout ratio below 30 percent. 2. timely interest and principal payments. 3. a total debt-to-capitalization ratio of no more than 60 percent. Jokinen expects that the current environment of low interest rates and low interest rate volatility may not continue. So, he analyzes the effects of an increase in interest rates and volatility on the value of any callable bonds in the portfolio. Jokinen states: "If interest rates rise and interest rate volatility remains unchanged, the value of callable bonds should decrease." "If interest rate volatility increases and interest rates remain unchanged, the value of the callable bonds should increase." France Telecom Bonds Jokinen is considering investing in a France Telecom (FRTEL) convertible bond because of the favorable outcome for the industry. His 12-month price forecast is 27.5 per FRTEL share. The convertible bond has the following characteristics: FRTEL 1.6% 01 January 2025 Conversion ratio is 100 shares per bond. Par value is 2,581. Current price of the bond is 2,825. FRTEL common stock has current price of c25.75 per share and pays no dividend. Bond is callable at 2.581 on 31 December 2021. Dual Currency Bond Finally, Jokinen is considering a dual currency bond with coupon payments in euros and principal repayment in Turkish lira. He states that the bond would not have any currency exposure to the Turkish lira until it matured and the Turkish lira were actually paid. 1. The total debt-to-capitalization and the EBITDA interest coverage ratios for Thor Products are closest to: EBITDA Interest Coverage 5.3 4 Total Debt-to-Capitalization 68.40% 76.40% 84.40% B. 8 C. 2.7 2. Which of the three covenants on Thor's bonds is an affirmative covenant? A. #1 B. #2 C. #3 3. Are Jokinen's statements regarding the effects on callable bonds of an increase in interest rates and an increase in interest rate volatility, respectively, correct? Interest Rates No A. Interest Rate Volatility No Yes B. No Yes C. No 4. The premium payback period (in years) for the France Telecom convertible bond is closest to: A. 1.60 B. 1.81 C. 6.05 5. Is Jokinen's statement about the currency exposure to investing in the dual currency bond (euro and Turkish lira) correct? A. No, the bond has exposure to the Turkish lira from the date o purchase. B. Yes, the bond has appreciation exposure to the Turkish lira only at maturity. C. Yes, the bond has depreciation exposure to the Turkish lira only at maturity

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For IT Decision Makers

Authors: Michael Blackstaff

3rd Edition

1780171226, 978-1780171227