Answered step by step

Verified Expert Solution

Question

1 Approved Answer

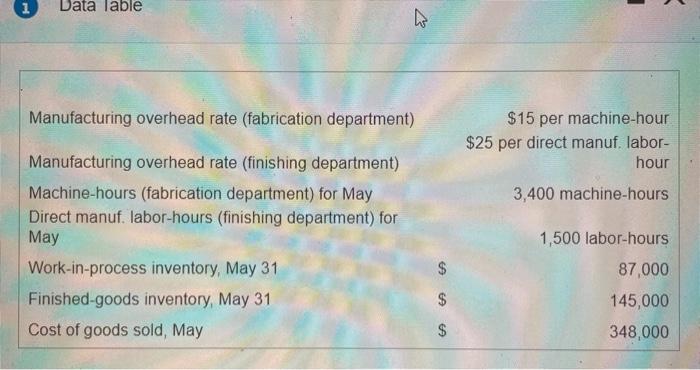

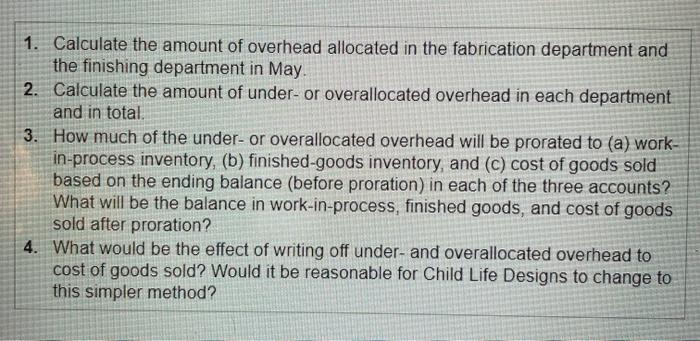

Additi Child Life Designs makes custom backyard play structures that it sells to dealers across the Midwest The play structures are produced in two departments,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Accounting Uk Gaap Volume 2

Authors: Alan Sangster, Frank Wood

1st Edition

0273718800, 9780273718802