Answered step by step

Verified Expert Solution

Question

1 Approved Answer

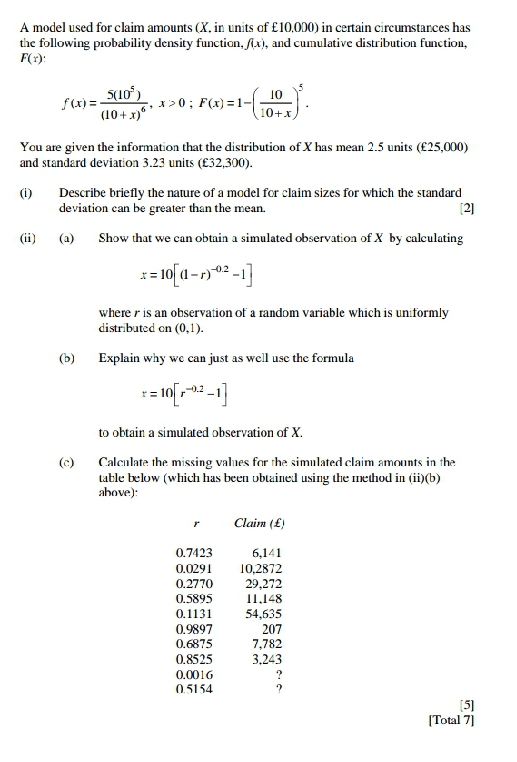

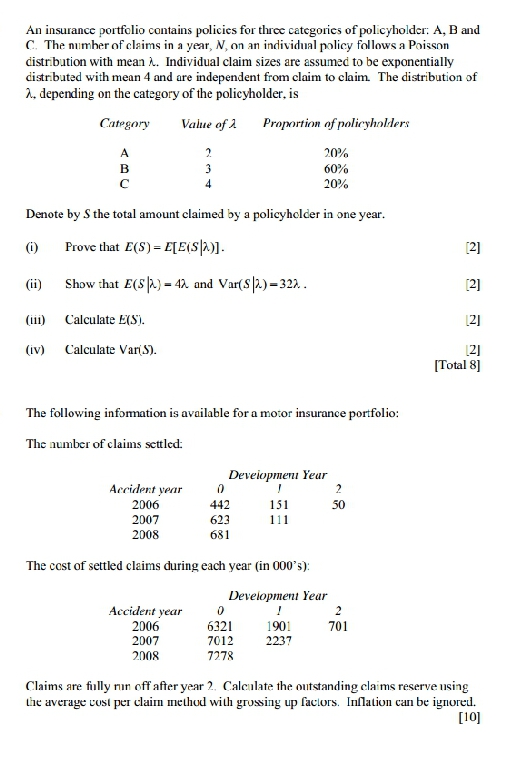

Address the following questions effectively. All the parts please A model used for claim amounts (X. in units of (10,000) in certain circumstances has the

Address the following questions effectively. All the parts please

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Theory And Applications Of Partial Functional Differential Equations

Authors: Abrar A Khan

1st Edition

9353141915, 9789353141912