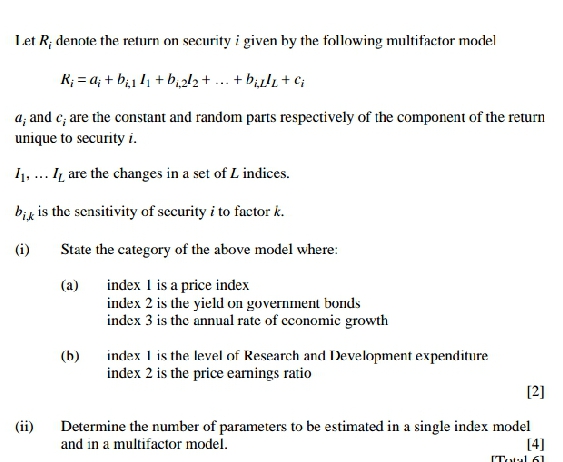

Question: Adress all the questions effectively Let R; denote the return on security i given by the following multifactor model K; =di + bill + bal2

Adress all the questions effectively

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock