Advanced Accounting

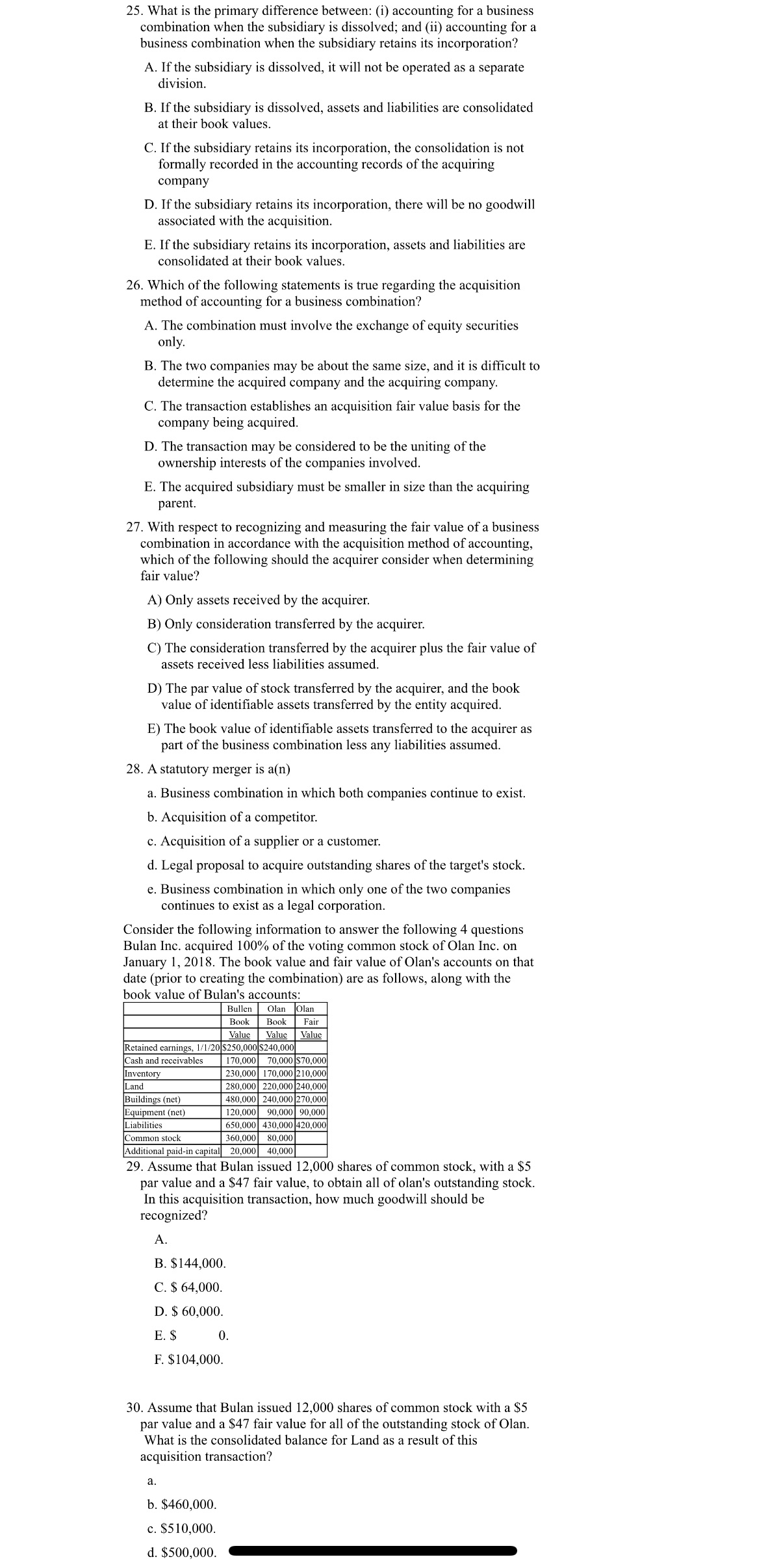

25. What is the primary difference between: (i) accounting for a business combination when the subsidiary is dissolved; and (ii) accounting for a business combination when the subsidiary retains its incorporation? A. If the subsidiary is dissolved, it will not be operated as a separate division. B. If the subsidiary is dissolved, assets and liabilities are consolidated at their book values. C. If the subsidiary retains its incorporation, the consolidation is not formally recorded in the accounting records of the acquiring company D. If the subsidiary retains its incorporation, there will be no goodwill associated with the acquisition. E. If the subsidiary retains its incorporation, assets and liabilities are consolidated at their book values. 26. Which of the following statements is true regarding the acquisition method of accounting for a business combination? A. The combination must involve the exchange of equity securities only. B. The two companies may be about the same size, and it is difficult to determine the acquired company and the acquiring company. C. The transaction establishes an acquisition fair value basis for the company being acquired. D. The transaction may be considered to be the uniting of the ownership interests of the companies involved. E. The acquired subsidiary must be smaller in size than the acquiring parent. 27. With respect to recognizing and measuring the fair value of a business combination in accordance with the acquisition method of accounting, which of the following should the acquirer consider when determining fair value? A) Only assets received by the acquirer. B) Only consideration transferred by the acquirer. C) The consideration transferred by the acquirer plus the fair value of assets received less liabilities assumed. D) The par value of stock transferred by the acquirer, and the book value of identiable assets transferred by the entity acquired. E) The book value of identiable assets transferred to the acquirer as part of the business combination less any liabilities assumed. 28. A statutory merger is a(n) a. Business combination in which both companies continue to exist. b. Acquisition of a competitor. c. Acquisition of a supplier or a customer. d. Legal proposal to acquire outstanding shares of the target's stock. e. Business combination in which only one of the two companies continues to exist as a legal corporation. Consider the following information to answer the following 4 questions Bulan Inc. acquired 100% of the voting common stock of Olan Inc. on January 1, 2018. The book value and fair value chlan's accounts on that date (prior to creating the combination) are as follows, along with the book value of Bulan's accounts: Bullert Olan Olan Fair M Retained earnings, 1:112_ 170,000 70,000 $70,000 230,000 170,000 210,000 2:50.000 220,000 240,000 4:10.000 240,000 270,000 120.000 90.000 90.000 Liabilities 650,000 410,000 420,000 Commonsrock 360,000 80,000 Adduionalpaid-incapual 20,000 40000 29. Assume that Bulan issued 12,000 shares of common stock, with a $5 par value and a $47 fair value, to obtain all of olan's outstanding stock. In this acquisition transaction, how much goodwill should be recognized? A. B. $144,000. C. $ 64,000. D. $ 60,000. E. $ 0. F. $104,000. 30. Assume that Bulan issued 12,000 shares of common stock with a $5 par value and a $47 fair value for all of the outstanding stock of Olan. What is the consolidated balance for Land as a result of this acquisition transaction? a. h. $460,000. c. $510,000. (1. $500,000