All information needed is listed below. This course is called Financial Account 2

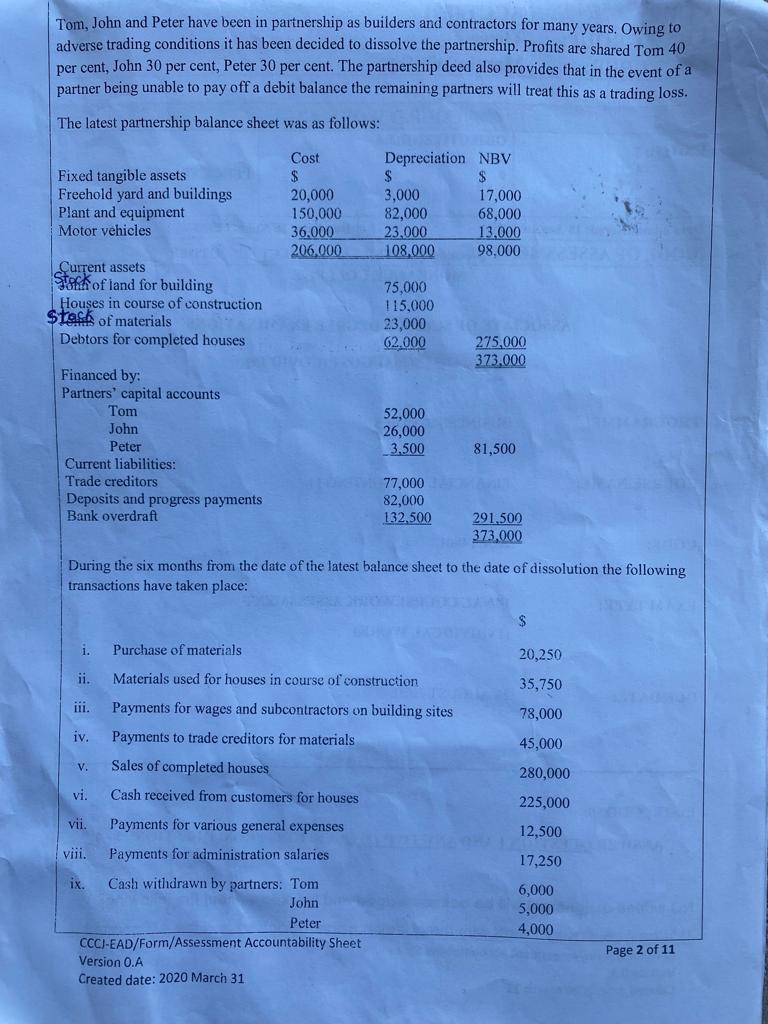

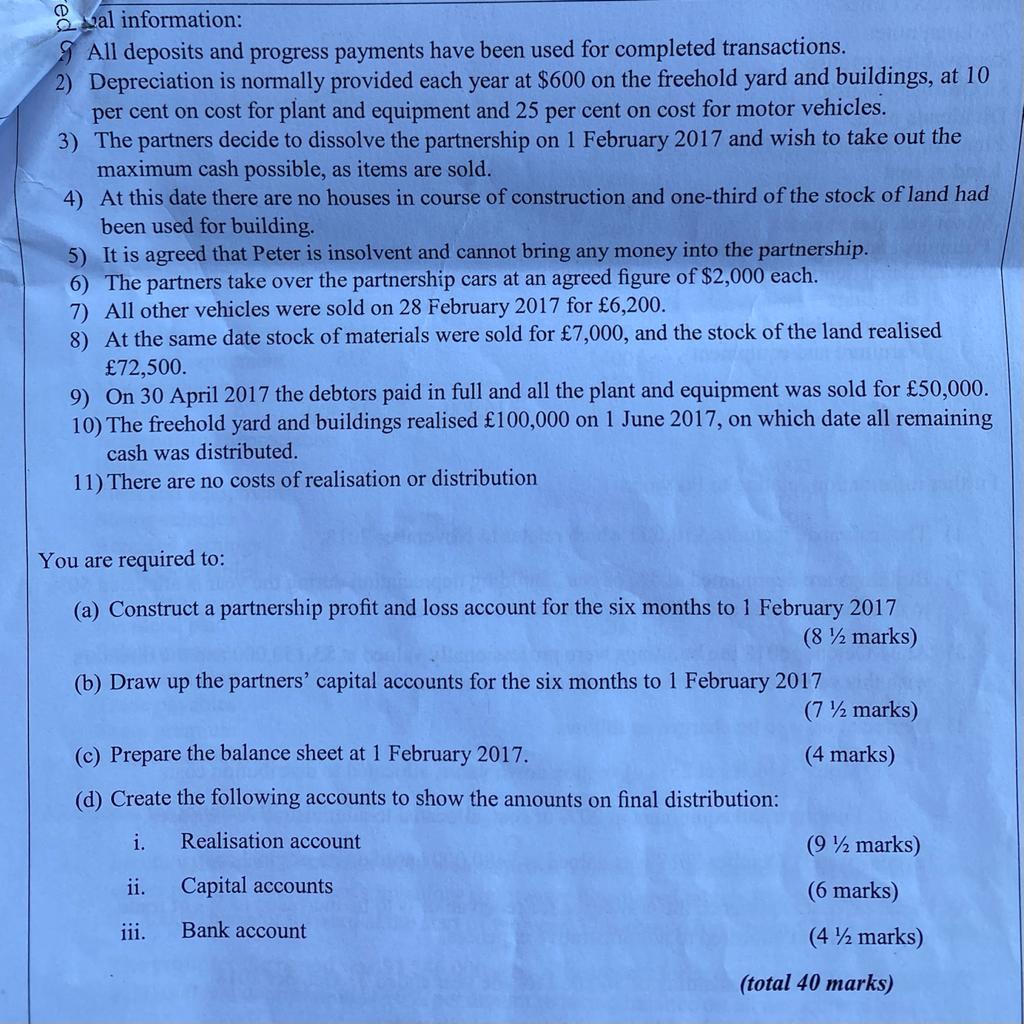

Tom, John and Peter have been in partnership as builders and contractors for many years. Owing to adverse trading conditions it has been decided to dissolve the partnership. Profits are shared Tom 40 per cent, John 30 per cent, Peter 30 per cent. The partnership deed also provides that in the event of a partner being unable to pay off a debit balance the remaining partners will treat this as a trading loss. The latest partnership balance sheet was as follows: Fixed tangible assets Freehold yard and buildings Plant and equipment Motor vehicles Cost $ 20,000 150,000 36.000 206,000 Depreciation NBV $ $ 3,000 17,000 82,000 68,000 23.000 13,000 108,000 98.000 Current assets Stork of land for building Houses in course of construction $task of materials Debtors for completed houses 75,000 115,000 23,000 62.000 275,000 373.000 Financed by: Partners' capital accounts Tom John Peter Current liabilities: Trade creditors Deposits and progress payments Bank overdraft 52,000 26,000 3.500 81,500 77,000 82,000 132.500 291,500 373,000 During the six months from the date of the latest balance sheet to the date of dissolution the following transactions have taken place: $ 1. Purchase of materials 20,250 ii. Materials used for houses in course of construction 35,750 iii. 78,000 iv. 45,000 V. Payments for wages and subcontractors on building sites Payments to trade creditors for materials Sales of completed houses Cash received from customers for houses Payments for various general expenses 280,000 vi. 225,000 vii 12,500 17,250 viii. Payments for administration salaries ix. Cash withdrawn by partners: Tom John Peter CCCI-EAD/Form/Assessment Accountability Sheet Version 0.A Created date: 2020 March 31 6,000 5,000 4,000 Page 2 of 11 D wal information: All deposits and progress payments have been used for completed transactions. 2) Depreciation is normally provided each year at $600 on the freehold yard and buildings, at 10 per cent on cost for plant and equipment and 25 per cent on cost for motor vehicles. 3) The partners decide to dissolve the partnership on 1 February 2017 and wish to take out the maximum cash possible, as items are sold. 4) At this date there are no houses in course of construction and one-third of the stock of land had been used for building. 5) It is agreed that Peter is insolvent and cannot bring any money into the partnership. 6) The partners take over the partnership cars at an agreed figure of $2,000 each. 7) All other vehicles were sold on 28 February 2017 for 6,200. 8) At the same date stock of materials were sold for 7,000, and the stock of the land realised 72,500. 9) On 30 April 2017 the debtors paid in full and all the plant and equipment was sold for 50,000. 10) The freehold yard and buildings realised 100,000 on 1 June 2017, on which date all remaining cash was distributed. 11) There are no costs of realisation or distribution You are required to: (a) Construct a partnership profit and loss account for the six months to 1 February 2017 (8 % marks) (b) Draw up the partners' capital accounts for the six months to 1 February 2017 (7/2 marks) (4 marks) (c) Prepare the balance sheet at 1 February 2017. (d) Create the following accounts to show the amounts on final distribution: i. Realisation account (972 marks) ii. Capital accounts (6 marks) iii. Bank account (4/2 marks) (total 40 marks) Tom, John and Peter have been in partnership as builders and contractors for many years. Owing to adverse trading conditions it has been decided to dissolve the partnership. Profits are shared Tom 40 per cent, John 30 per cent, Peter 30 per cent. The partnership deed also provides that in the event of a partner being unable to pay off a debit balance the remaining partners will treat this as a trading loss. The latest partnership balance sheet was as follows: Fixed tangible assets Freehold yard and buildings Plant and equipment Motor vehicles Cost $ 20,000 150,000 36.000 206,000 Depreciation NBV $ $ 3,000 17,000 82,000 68,000 23.000 13,000 108,000 98.000 Current assets Stork of land for building Houses in course of construction $task of materials Debtors for completed houses 75,000 115,000 23,000 62.000 275,000 373.000 Financed by: Partners' capital accounts Tom John Peter Current liabilities: Trade creditors Deposits and progress payments Bank overdraft 52,000 26,000 3.500 81,500 77,000 82,000 132.500 291,500 373,000 During the six months from the date of the latest balance sheet to the date of dissolution the following transactions have taken place: $ 1. Purchase of materials 20,250 ii. Materials used for houses in course of construction 35,750 iii. 78,000 iv. 45,000 V. Payments for wages and subcontractors on building sites Payments to trade creditors for materials Sales of completed houses Cash received from customers for houses Payments for various general expenses 280,000 vi. 225,000 vii 12,500 17,250 viii. Payments for administration salaries ix. Cash withdrawn by partners: Tom John Peter CCCI-EAD/Form/Assessment Accountability Sheet Version 0.A Created date: 2020 March 31 6,000 5,000 4,000 Page 2 of 11 D wal information: All deposits and progress payments have been used for completed transactions. 2) Depreciation is normally provided each year at $600 on the freehold yard and buildings, at 10 per cent on cost for plant and equipment and 25 per cent on cost for motor vehicles. 3) The partners decide to dissolve the partnership on 1 February 2017 and wish to take out the maximum cash possible, as items are sold. 4) At this date there are no houses in course of construction and one-third of the stock of land had been used for building. 5) It is agreed that Peter is insolvent and cannot bring any money into the partnership. 6) The partners take over the partnership cars at an agreed figure of $2,000 each. 7) All other vehicles were sold on 28 February 2017 for 6,200. 8) At the same date stock of materials were sold for 7,000, and the stock of the land realised 72,500. 9) On 30 April 2017 the debtors paid in full and all the plant and equipment was sold for 50,000. 10) The freehold yard and buildings realised 100,000 on 1 June 2017, on which date all remaining cash was distributed. 11) There are no costs of realisation or distribution You are required to: (a) Construct a partnership profit and loss account for the six months to 1 February 2017 (8 % marks) (b) Draw up the partners' capital accounts for the six months to 1 February 2017 (7/2 marks) (4 marks) (c) Prepare the balance sheet at 1 February 2017. (d) Create the following accounts to show the amounts on final distribution: i. Realisation account (972 marks) ii. Capital accounts (6 marks) iii. Bank account (4/2 marks) (total 40 marks)