All interest rates are annual interest rates with semi-annual compounding. All coupon rates are annual rates paid semi-annually. All bonds have $100 face values. Keep at least 6 decimal digits.

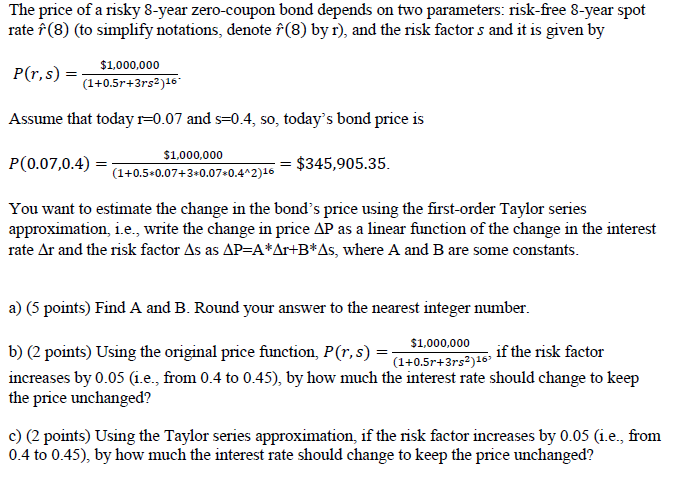

The price of a risky 8-year zero-coupon bond depends on two parameters: risk-free 8-year spot rate f (8) (to simplify notations, denote f(8) by r), and the risk factor s and it is given by $1,000,000 P(r,s) = (1+0.5r+3rs2)16 Assume that today r=0.07 and s=0.4, so, today's bond price is P(0.07,0.4) $1,000,000 (1+0.5*0.07+3+0.07.0.4^2)16 = $345,905.35. You want to estimate the change in the bond's price using the first-order Taylor series approximation, i.e., write the change in price AP as a linear function of the change in the interest rate Ar and the risk factor As as AP=A*Ar+B*As, where A and B are some constants. a) (5 points) Find A and B. Round your answer to the nearest integer number. b) (2 points) Using the original price function, P(r,s) = $1,000,000 if the risk factor (1+0.5r+3rs2)163 increases by 0.05 (i.e., from 0.4 to 0.45), by how much the interest rate should change to keep the price unchanged? c) (2 points) Using the Taylor series approximation, if the risk factor increases by 0.05 (i.e., from 0.4 to 0.45), by how much the interest rate should change to keep the price unchanged? The price of a risky 8-year zero-coupon bond depends on two parameters: risk-free 8-year spot rate f (8) (to simplify notations, denote f(8) by r), and the risk factor s and it is given by $1,000,000 P(r,s) = (1+0.5r+3rs2)16 Assume that today r=0.07 and s=0.4, so, today's bond price is P(0.07,0.4) $1,000,000 (1+0.5*0.07+3+0.07.0.4^2)16 = $345,905.35. You want to estimate the change in the bond's price using the first-order Taylor series approximation, i.e., write the change in price AP as a linear function of the change in the interest rate Ar and the risk factor As as AP=A*Ar+B*As, where A and B are some constants. a) (5 points) Find A and B. Round your answer to the nearest integer number. b) (2 points) Using the original price function, P(r,s) = $1,000,000 if the risk factor (1+0.5r+3rs2)163 increases by 0.05 (i.e., from 0.4 to 0.45), by how much the interest rate should change to keep the price unchanged? c) (2 points) Using the Taylor series approximation, if the risk factor increases by 0.05 (i.e., from 0.4 to 0.45), by how much the interest rate should change to keep the price unchanged