Answered step by step

Verified Expert Solution

Question

1 Approved Answer

All paid time off may not be the same. A city has adopted the following plan for compensated time off: - City employees are entitled

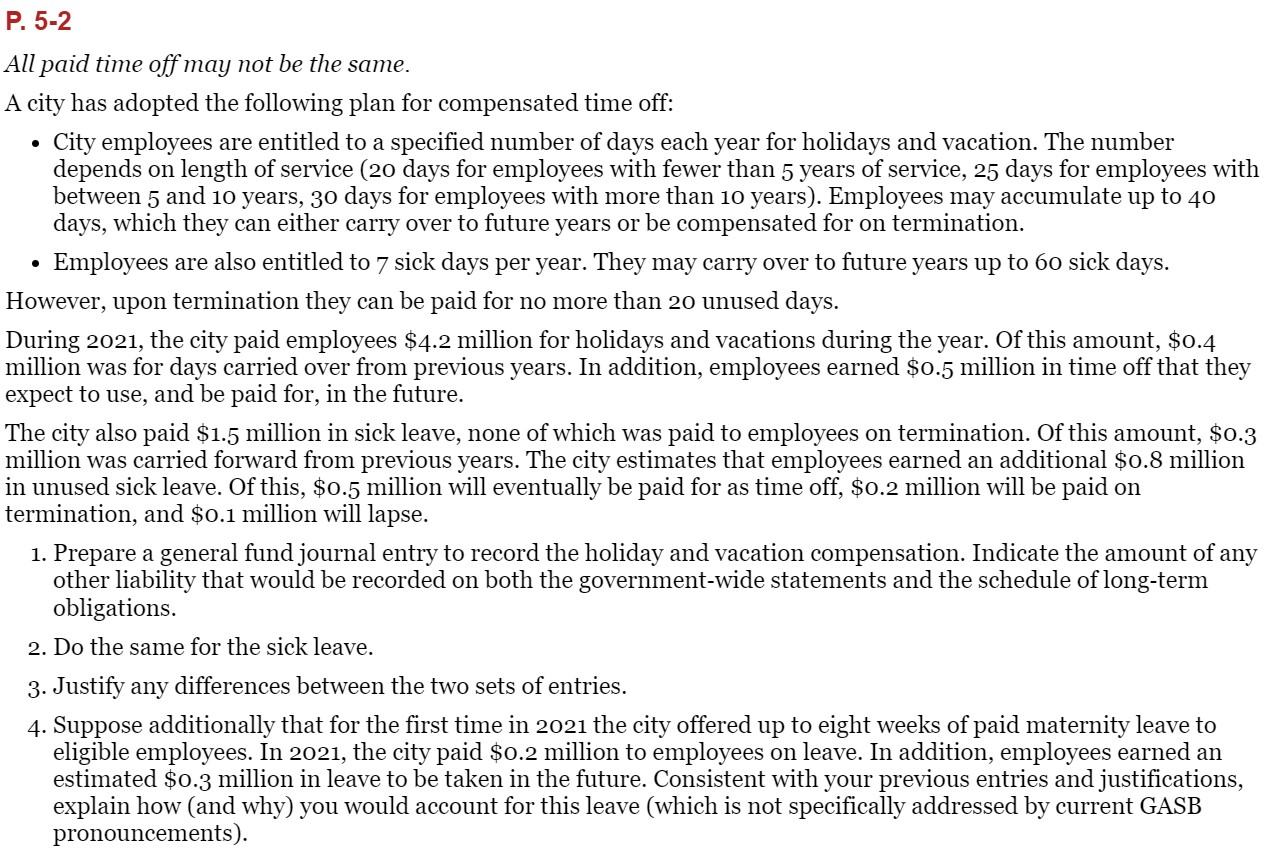

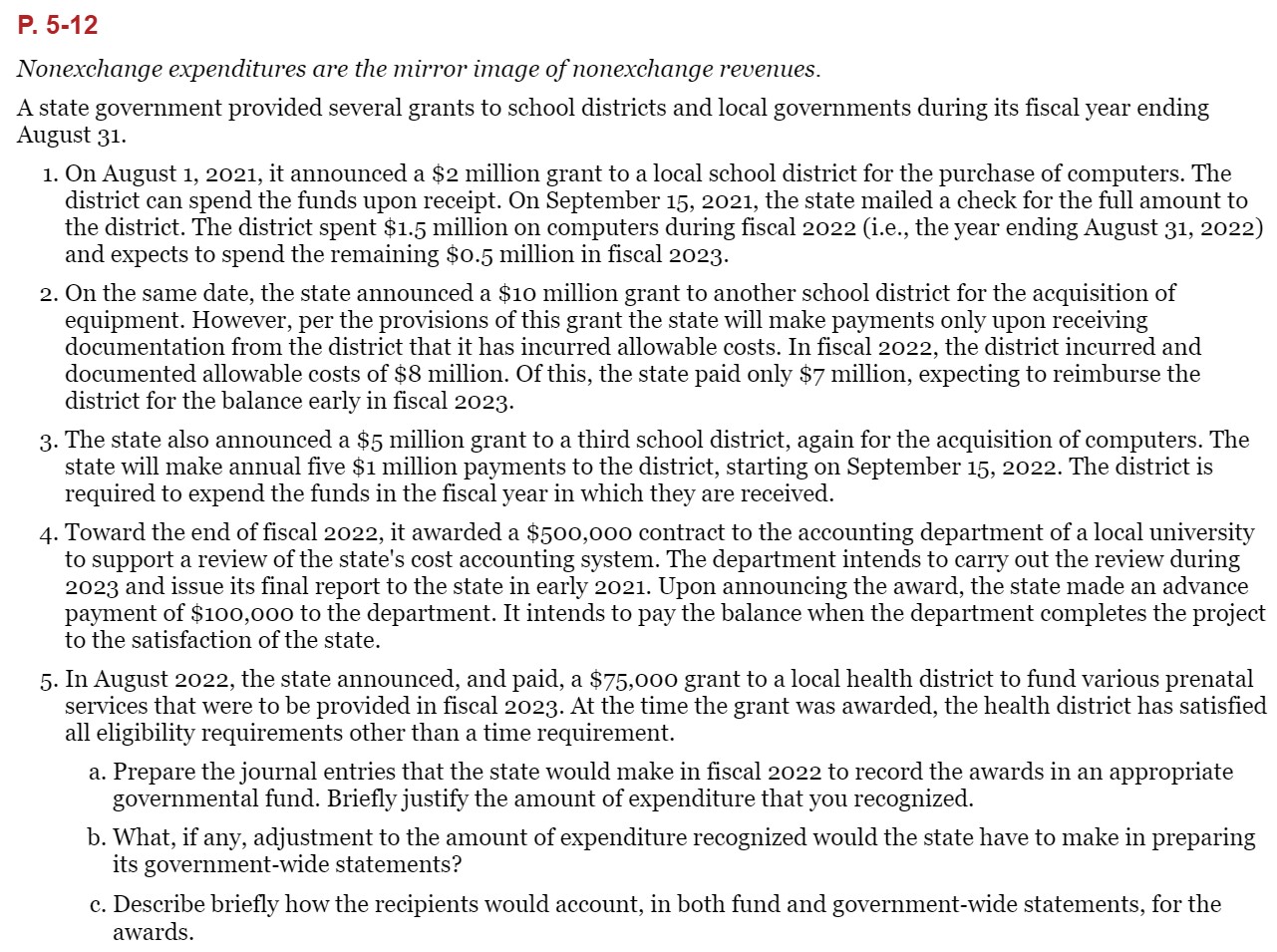

All paid time off may not be the same. A city has adopted the following plan for compensated time off: - City employees are entitled to a specified number of days each year for holidays and vacation. The number depends on length of service (20 days for employees with fewer than 5 years of service, 25 days for employees with between 5 and 10 years, 30 days for employees with more than 10 years). Employees may accumulate up to 40 days, which they can either carry over to future years or be compensated for on termination. - Employees are also entitled to 7 sick days per year. They may carry over to future years up to 60 sick days. However, upon termination they can be paid for no more than 20 unused days. During 2021, the city paid employees $4.2 million for holidays and vacations during the year. Of this amount, \$0.4 million was for days carried over from previous years. In addition, employees earned $0.5 million in time off that they expect to use, and be paid for, in the future. The city also paid $1.5 million in sick leave, none of which was paid to employees on termination. Of this amount, \$0.3 million was carried forward from previous years. The city estimates that employees earned an additional $0.8 million in unused sick leave. Of this, \$0.5 million will eventually be paid for as time off, $0.2 million will be paid on termination, and \$0.1 million will lapse. 1. Prepare a general fund journal entry to record the holiday and vacation compensation. Indicate the amount of any other liability that would be recorded on both the government-wide statements and the schedule of long-term obligations. 2. Do the same for the sick leave. 3. Justify any differences between the two sets of entries. 4. Suppose additionally that for the first time in 2021 the city offered up to eight weeks of paid maternity leave to eligible employees. In 2021, the city paid \$0.2 million to employees on leave. In addition, employees earned an estimated \$0.3 million in leave to be taken in the future. Consistent with your previous entries and justifications, explain how (and why) you would account for this leave (which is not specifically addressed by current GASB pronouncements). Nonexchange expenditures are the mirror image of nonexchange revenues. A state government provided several grants to school districts and local governments during its fiscal year ending August 31. 1. On August 1, 2021, it announced a \$2 million grant to a local school district for the purchase of computers. The district can spend the funds upon receipt. On September 15, 2021, the state mailed a check for the full amount to the district. The district spent \$1.5 million on computers during fiscal 2022 (i.e., the year ending August 31, 2022) and expects to spend the remaining \$0.5 million in fiscal 2023. 2. On the same date, the state announced a $10 million grant to another school district for the acquisition of equipment. However, per the provisions of this grant the state will make payments only upon receiving documentation from the district that it has incurred allowable costs. In fiscal 2022, the district incurred and documented allowable costs of $8 million. Of this, the state paid only $7 million, expecting to reimburse the district for the balance early in fiscal 2023. 3. The state also announced a $5 million grant to a third school district, again for the acquisition of computers. The state will make annual five $1 million payments to the district, starting on September 15, 2022. The district is required to expend the funds in the fiscal year in which they are received. 4. Toward the end of fiscal 2022, it awarded a $500,000 contract to the accounting department of a local university to support a review of the state's cost accounting system. The department intends to carry out the review during 2023 and issue its final report to the state in early 2021. Upon announcing the award, the state made an advance payment of $100,000 to the department. It intends to pay the balance when the department completes the project to the satisfaction of the state. 5. In August 2022, the state announced, and paid, a $75,000 grant to a local health district to fund various prenatal services that were to be provided in fiscal 2023. At the time the grant was awarded, the health district has satisfied all eligibility requirements other than a time requirement. a. Prepare the journal entries that the state would make in fiscal 2022 to record the awards in an appropriate governmental fund. Briefly justify the amount of expenditure that you recognized. b. What, if any, adjustment to the amount of expenditure recognized would the state have to make in preparing its government-wide statements? c. Describe briefly how the recipients would account, in both fund and government-wide statements, for the All paid time off may not be the same. A city has adopted the following plan for compensated time off: - City employees are entitled to a specified number of days each year for holidays and vacation. The number depends on length of service (20 days for employees with fewer than 5 years of service, 25 days for employees with between 5 and 10 years, 30 days for employees with more than 10 years). Employees may accumulate up to 40 days, which they can either carry over to future years or be compensated for on termination. - Employees are also entitled to 7 sick days per year. They may carry over to future years up to 60 sick days. However, upon termination they can be paid for no more than 20 unused days. During 2021, the city paid employees $4.2 million for holidays and vacations during the year. Of this amount, \$0.4 million was for days carried over from previous years. In addition, employees earned $0.5 million in time off that they expect to use, and be paid for, in the future. The city also paid $1.5 million in sick leave, none of which was paid to employees on termination. Of this amount, \$0.3 million was carried forward from previous years. The city estimates that employees earned an additional $0.8 million in unused sick leave. Of this, \$0.5 million will eventually be paid for as time off, $0.2 million will be paid on termination, and \$0.1 million will lapse. 1. Prepare a general fund journal entry to record the holiday and vacation compensation. Indicate the amount of any other liability that would be recorded on both the government-wide statements and the schedule of long-term obligations. 2. Do the same for the sick leave. 3. Justify any differences between the two sets of entries. 4. Suppose additionally that for the first time in 2021 the city offered up to eight weeks of paid maternity leave to eligible employees. In 2021, the city paid \$0.2 million to employees on leave. In addition, employees earned an estimated \$0.3 million in leave to be taken in the future. Consistent with your previous entries and justifications, explain how (and why) you would account for this leave (which is not specifically addressed by current GASB pronouncements). Nonexchange expenditures are the mirror image of nonexchange revenues. A state government provided several grants to school districts and local governments during its fiscal year ending August 31. 1. On August 1, 2021, it announced a \$2 million grant to a local school district for the purchase of computers. The district can spend the funds upon receipt. On September 15, 2021, the state mailed a check for the full amount to the district. The district spent \$1.5 million on computers during fiscal 2022 (i.e., the year ending August 31, 2022) and expects to spend the remaining \$0.5 million in fiscal 2023. 2. On the same date, the state announced a $10 million grant to another school district for the acquisition of equipment. However, per the provisions of this grant the state will make payments only upon receiving documentation from the district that it has incurred allowable costs. In fiscal 2022, the district incurred and documented allowable costs of $8 million. Of this, the state paid only $7 million, expecting to reimburse the district for the balance early in fiscal 2023. 3. The state also announced a $5 million grant to a third school district, again for the acquisition of computers. The state will make annual five $1 million payments to the district, starting on September 15, 2022. The district is required to expend the funds in the fiscal year in which they are received. 4. Toward the end of fiscal 2022, it awarded a $500,000 contract to the accounting department of a local university to support a review of the state's cost accounting system. The department intends to carry out the review during 2023 and issue its final report to the state in early 2021. Upon announcing the award, the state made an advance payment of $100,000 to the department. It intends to pay the balance when the department completes the project to the satisfaction of the state. 5. In August 2022, the state announced, and paid, a $75,000 grant to a local health district to fund various prenatal services that were to be provided in fiscal 2023. At the time the grant was awarded, the health district has satisfied all eligibility requirements other than a time requirement. a. Prepare the journal entries that the state would make in fiscal 2022 to record the awards in an appropriate governmental fund. Briefly justify the amount of expenditure that you recognized. b. What, if any, adjustment to the amount of expenditure recognized would the state have to make in preparing its government-wide statements? c. Describe briefly how the recipients would account, in both fund and government-wide statements, for the

All paid time off may not be the same. A city has adopted the following plan for compensated time off: - City employees are entitled to a specified number of days each year for holidays and vacation. The number depends on length of service (20 days for employees with fewer than 5 years of service, 25 days for employees with between 5 and 10 years, 30 days for employees with more than 10 years). Employees may accumulate up to 40 days, which they can either carry over to future years or be compensated for on termination. - Employees are also entitled to 7 sick days per year. They may carry over to future years up to 60 sick days. However, upon termination they can be paid for no more than 20 unused days. During 2021, the city paid employees $4.2 million for holidays and vacations during the year. Of this amount, \$0.4 million was for days carried over from previous years. In addition, employees earned $0.5 million in time off that they expect to use, and be paid for, in the future. The city also paid $1.5 million in sick leave, none of which was paid to employees on termination. Of this amount, \$0.3 million was carried forward from previous years. The city estimates that employees earned an additional $0.8 million in unused sick leave. Of this, \$0.5 million will eventually be paid for as time off, $0.2 million will be paid on termination, and \$0.1 million will lapse. 1. Prepare a general fund journal entry to record the holiday and vacation compensation. Indicate the amount of any other liability that would be recorded on both the government-wide statements and the schedule of long-term obligations. 2. Do the same for the sick leave. 3. Justify any differences between the two sets of entries. 4. Suppose additionally that for the first time in 2021 the city offered up to eight weeks of paid maternity leave to eligible employees. In 2021, the city paid \$0.2 million to employees on leave. In addition, employees earned an estimated \$0.3 million in leave to be taken in the future. Consistent with your previous entries and justifications, explain how (and why) you would account for this leave (which is not specifically addressed by current GASB pronouncements). Nonexchange expenditures are the mirror image of nonexchange revenues. A state government provided several grants to school districts and local governments during its fiscal year ending August 31. 1. On August 1, 2021, it announced a \$2 million grant to a local school district for the purchase of computers. The district can spend the funds upon receipt. On September 15, 2021, the state mailed a check for the full amount to the district. The district spent \$1.5 million on computers during fiscal 2022 (i.e., the year ending August 31, 2022) and expects to spend the remaining \$0.5 million in fiscal 2023. 2. On the same date, the state announced a $10 million grant to another school district for the acquisition of equipment. However, per the provisions of this grant the state will make payments only upon receiving documentation from the district that it has incurred allowable costs. In fiscal 2022, the district incurred and documented allowable costs of $8 million. Of this, the state paid only $7 million, expecting to reimburse the district for the balance early in fiscal 2023. 3. The state also announced a $5 million grant to a third school district, again for the acquisition of computers. The state will make annual five $1 million payments to the district, starting on September 15, 2022. The district is required to expend the funds in the fiscal year in which they are received. 4. Toward the end of fiscal 2022, it awarded a $500,000 contract to the accounting department of a local university to support a review of the state's cost accounting system. The department intends to carry out the review during 2023 and issue its final report to the state in early 2021. Upon announcing the award, the state made an advance payment of $100,000 to the department. It intends to pay the balance when the department completes the project to the satisfaction of the state. 5. In August 2022, the state announced, and paid, a $75,000 grant to a local health district to fund various prenatal services that were to be provided in fiscal 2023. At the time the grant was awarded, the health district has satisfied all eligibility requirements other than a time requirement. a. Prepare the journal entries that the state would make in fiscal 2022 to record the awards in an appropriate governmental fund. Briefly justify the amount of expenditure that you recognized. b. What, if any, adjustment to the amount of expenditure recognized would the state have to make in preparing its government-wide statements? c. Describe briefly how the recipients would account, in both fund and government-wide statements, for the All paid time off may not be the same. A city has adopted the following plan for compensated time off: - City employees are entitled to a specified number of days each year for holidays and vacation. The number depends on length of service (20 days for employees with fewer than 5 years of service, 25 days for employees with between 5 and 10 years, 30 days for employees with more than 10 years). Employees may accumulate up to 40 days, which they can either carry over to future years or be compensated for on termination. - Employees are also entitled to 7 sick days per year. They may carry over to future years up to 60 sick days. However, upon termination they can be paid for no more than 20 unused days. During 2021, the city paid employees $4.2 million for holidays and vacations during the year. Of this amount, \$0.4 million was for days carried over from previous years. In addition, employees earned $0.5 million in time off that they expect to use, and be paid for, in the future. The city also paid $1.5 million in sick leave, none of which was paid to employees on termination. Of this amount, \$0.3 million was carried forward from previous years. The city estimates that employees earned an additional $0.8 million in unused sick leave. Of this, \$0.5 million will eventually be paid for as time off, $0.2 million will be paid on termination, and \$0.1 million will lapse. 1. Prepare a general fund journal entry to record the holiday and vacation compensation. Indicate the amount of any other liability that would be recorded on both the government-wide statements and the schedule of long-term obligations. 2. Do the same for the sick leave. 3. Justify any differences between the two sets of entries. 4. Suppose additionally that for the first time in 2021 the city offered up to eight weeks of paid maternity leave to eligible employees. In 2021, the city paid \$0.2 million to employees on leave. In addition, employees earned an estimated \$0.3 million in leave to be taken in the future. Consistent with your previous entries and justifications, explain how (and why) you would account for this leave (which is not specifically addressed by current GASB pronouncements). Nonexchange expenditures are the mirror image of nonexchange revenues. A state government provided several grants to school districts and local governments during its fiscal year ending August 31. 1. On August 1, 2021, it announced a \$2 million grant to a local school district for the purchase of computers. The district can spend the funds upon receipt. On September 15, 2021, the state mailed a check for the full amount to the district. The district spent \$1.5 million on computers during fiscal 2022 (i.e., the year ending August 31, 2022) and expects to spend the remaining \$0.5 million in fiscal 2023. 2. On the same date, the state announced a $10 million grant to another school district for the acquisition of equipment. However, per the provisions of this grant the state will make payments only upon receiving documentation from the district that it has incurred allowable costs. In fiscal 2022, the district incurred and documented allowable costs of $8 million. Of this, the state paid only $7 million, expecting to reimburse the district for the balance early in fiscal 2023. 3. The state also announced a $5 million grant to a third school district, again for the acquisition of computers. The state will make annual five $1 million payments to the district, starting on September 15, 2022. The district is required to expend the funds in the fiscal year in which they are received. 4. Toward the end of fiscal 2022, it awarded a $500,000 contract to the accounting department of a local university to support a review of the state's cost accounting system. The department intends to carry out the review during 2023 and issue its final report to the state in early 2021. Upon announcing the award, the state made an advance payment of $100,000 to the department. It intends to pay the balance when the department completes the project to the satisfaction of the state. 5. In August 2022, the state announced, and paid, a $75,000 grant to a local health district to fund various prenatal services that were to be provided in fiscal 2023. At the time the grant was awarded, the health district has satisfied all eligibility requirements other than a time requirement. a. Prepare the journal entries that the state would make in fiscal 2022 to record the awards in an appropriate governmental fund. Briefly justify the amount of expenditure that you recognized. b. What, if any, adjustment to the amount of expenditure recognized would the state have to make in preparing its government-wide statements? c. Describe briefly how the recipients would account, in both fund and government-wide statements, for the Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Survey of Accounting

Authors: Thomas Edmonds, Christopher, Philip Olds, Frances McNair, Bor

4th edition

77862376, 978-0077862374