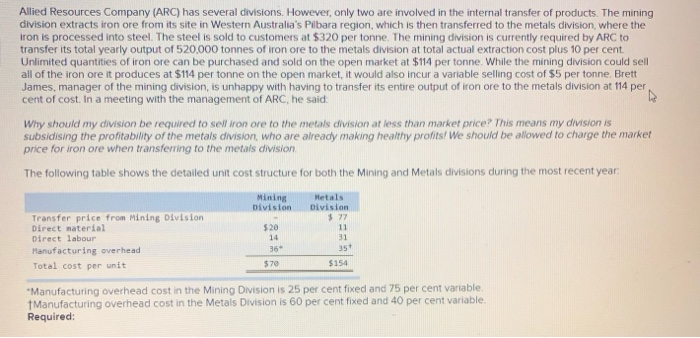

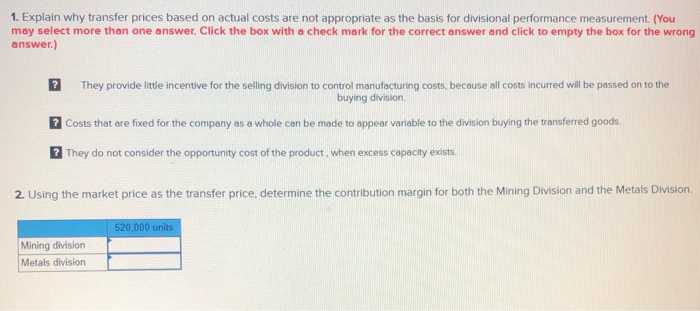

Allied Resources Company (ARC) has several divisions. However, only two are involved in the internal transfer of products. The mining division extracts iron ore from its site in Western Australia's Pilbara region, which is then transferred to the metals division, where the Iron is processed into steel. The steel is sold to customers at $320 per tonne. The mining division is currently required by ARC to transfer its total yearly output of 520.000 tonnes of iron ore to the metals division at total actual extraction cost plus 10 per cent. Unlimited quantities of iron ore can be purchased and sold on the open market at $114 per tonne. While the mining division could sell all of the iron ore it produces at $114 per tonne on the open market, it would also incur a variable selling cost of $5 per tonne Brett James, manager of the mining division, is unhappy with having to transfer its entire output of iron ore to the metals division at 114 per cent of cost. In a meeting with the management of ARC, he said. Why should my division be required to sell iron ore to the metals division ar less than market price? This means my division is subsidising the profitability of the metals division, who are already making healthy profits! We should be allowed to charge the market price for iron ore when transferring to the metals division The following table shows the detailed unit cost structure for both the Mining and Metals divisions during the most recent year. Mining Division Metals Division $77 11 31 Transfer price from Mining Division Direct material Direct labour Manufacturing overhead Total cost per unit $20 14 36 $70 $154 Manufacturing overhead cost in the Mining Division is 25 per cent fixed and 75 per cent variable. Manufacturing overhead cost in the Metals Division is 60 per cent fixed and 40 per cent variable. Required: 1. Explain why transfer prices based on actual costs are not appropriate as the basis for divisional performance measurement. (You may select more than one answer. Click the box with a check mark for the correct answer and click to empty the box for the wrong answer.) They provide little incentive for the selling division to control manufacturing costs, because all costs incurred will be passed on to the buying division Costs that are fixed for the company as a whole can be made to appear variable to the division buying the transferred goods. They do not consider the opportunity cost of the product, when excess capacity exists. 2. Using the market price as the transfer price, determine the contribution margin for both the Mining Division and the Metals Division 520,000 units Mining division Metals division 3. If ARC were to introduce the use of negotiated transfer prices and allow divisions to buy and sell on the open market, determine the price range for toldine that would be acceptable to both the Mining Division and the Metals Division. (You may select more than one answer. Click the box with a check mark for the correct answer and click to empty the box for the wrong answer.) to Price range from 4-b is your answer consistent with your conclusion in requirement 3? ? Yes No 5 Identity which one of the three types of transfer prices (cost-based, market based or negotiated) is most likely to elicit desirable management behaviour at SIRC. Market based 2 Cost-based 2 Negotiated