Answered step by step

Verified Expert Solution

Question

1 Approved Answer

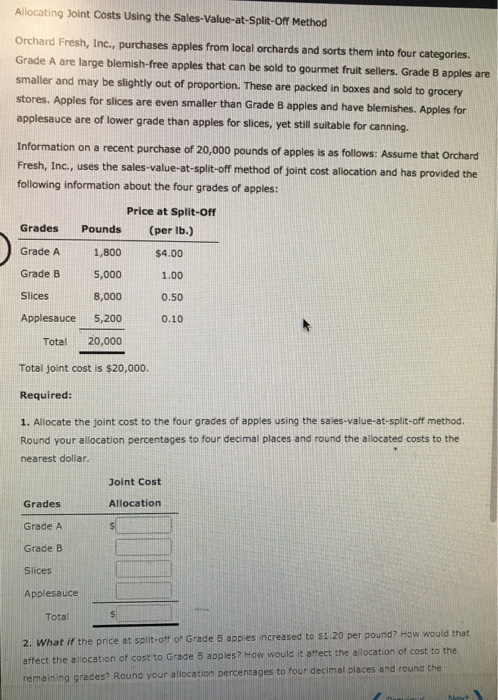

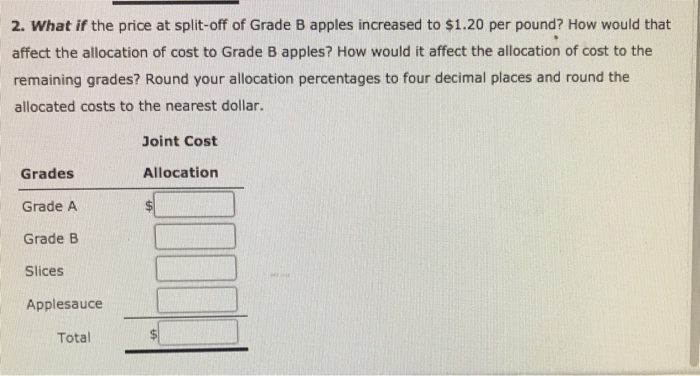

Allocating Joint Costs Using the Sales-Value-at-Split-Off Method Orchard Fresh, Inc., purchases apples from local orchards and sorts them into four categories. Grade A are large

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Energy Audits

Authors: Albert Thumann, Terry Niehus, William J. Younger

8th Edition

1439821453, 978-1439821459