Answered step by step

Verified Expert Solution

Question

1 Approved Answer

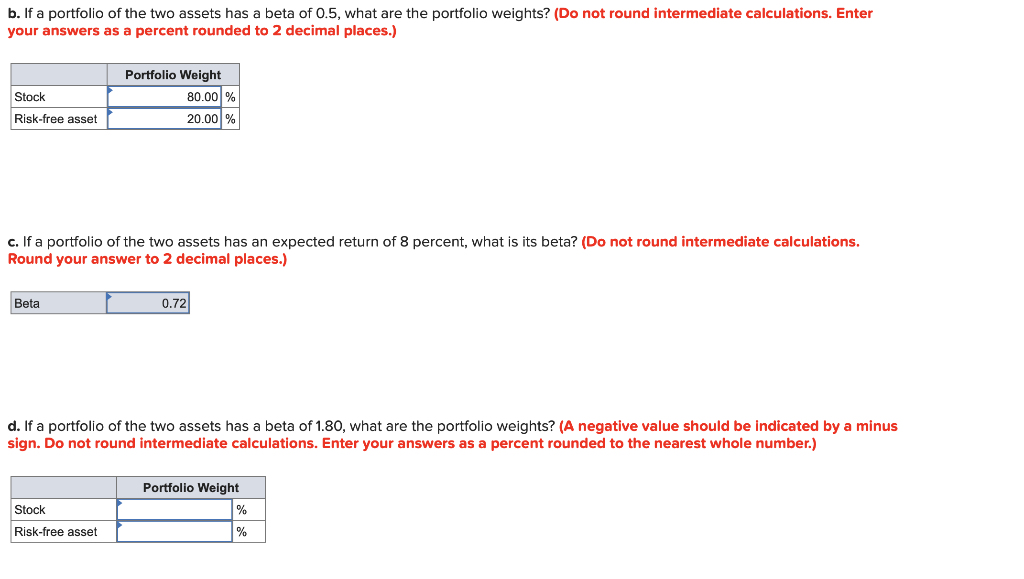

Also check b and c b. If a portfolio of the two assets has a beta of 0.5, what are the portfolio weights? (Do not

Also check b and c

b. If a portfolio of the two assets has a beta of 0.5, what are the portfolio weights? (Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) Stock Risk-free asset Portfolio Weight 80.00% 20.00% c. If a portfolio of the two assets has an expected return of 8 percent, what is its beta? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Beta 0.72 d. If a portfolio of the two assets has a beta of 1.80, what are the portfolio weights? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to the nearest whole number.) Portfolio Weight Stock Risk-free asset b. If a portfolio of the two assets has a beta of 0.5, what are the portfolio weights? (Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) Stock Risk-free asset Portfolio Weight 80.00% 20.00% c. If a portfolio of the two assets has an expected return of 8 percent, what is its beta? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Beta 0.72 d. If a portfolio of the two assets has a beta of 1.80, what are the portfolio weights? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to the nearest whole number.) Portfolio Weight Stock Risk-free assetStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Theory And Practice

Authors: Anne Marie Ward

3rd Edition

1908199482, 978-1908199485